Looking back at the last round of market, the biggest gameplay can actually be summarized as PVP.

Go to PVP here, go to PVP there, go to PVP on any chain that still has some heat and narrative.

As the time enters 2025, these chains have already entered the stage of stock competition - from the battle of hundreds of chains competing for the title of Ethereum killer a few years ago, to now most chains are labeled as "not even worth a dog", and those that remain are also trying to solve their own food problems.

Not only are the P players in PVP, but these chains are also in PVP.

It’s just that every chain seems to want to copy the excitement of Solana, but no matter how hard they try, they can’t replicate Solana’s meme scene.

The land and water nurture the people, and a public chain may only be able to do one thing.

Every public chain that is still alive has its purpose secretly marked.

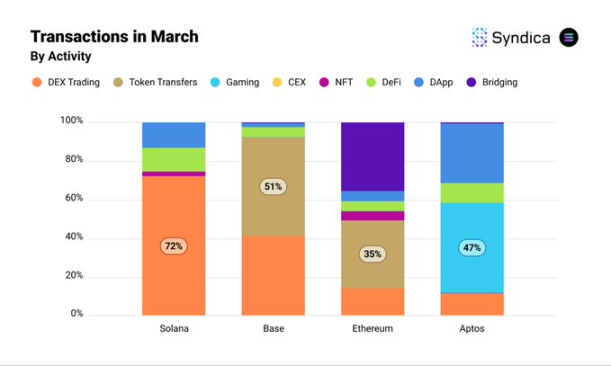

Recently, a March L1/L2 data insight report released by overseas news and research organization Syndica (@Syndica_io) made this sense of fate more concrete through numbers:

- 72% of all Solana transactions are related to decentralized exchanges (DEX), which obviously fits your impression.

- 51% of Base’s transactions are used for token transfers;

- Nearly 40% of ETH transactions are used for cross-chain transactions (purple bars in the above figure)

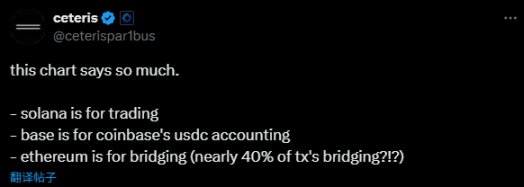

When faced with this set of data, @ceterispar1bus, research director of Delphi Digital, directly pointed out the essence of the topic:

- Solana is for transactions

- Base is used for Coinbase's USDC accounting

- Ethereum is used to transfer assets across chains

The industry has reached this point today, and projects are no longer simply a competition of technology, but about finding an "anchor" of one's own - a use positioning that can be logically positioned.

It is an identity label, but also a destiny

On the surface, the purpose of public chains seems to be selected by users and the market; but if you think about it more deeply, it is more like the result of "secret pricing" by resource endowments and background.

Let’s summarize the identity tags of the three public chains:

Solana is a hot spot for transactions, Base has become the "accountant" of Coinbase, Ethereum has been kidnapped by the bridge, and assets are outflowing at an accelerated rate.

Behind the current status of each chain, there are both technical and non-technical driving forces.

Let’s talk about Solana first.

Solana's on-chain ecosystem will still be the hottest meme trading hotspot in the circle in 2025.

The DEX transaction volume in its ecosystem has been the top for two consecutive months, with a market share far ahead. Since October 2024, Solana has created more than 500,000 MEME coins per month, like a never-ending "dog-beating party".

P young players are brave enough to sit and find angles, traders are busy monitoring the pool and the front of the car, and those who have played Meme mention Solana, and their first reaction is: "Isn't this chain just a big casino?"

Solana's high throughput (TPS is 12 times that of Base) and low cost (a high proportion of transactions below $0.01) are the basis of its trading hotspot. The Syndica report shows that Solana leads in small transactions (below $100) and is suitable for high-frequency trading of MEME coins.

As for whether to decentralize or not, it is probably not that important in terms of practical operation and physical experience.

More importantly, it is the starting advantage in resource endowment.

Between 2019 and 2023, Solana received investment support from a16z, Multicoin Capital, etc., and attracted DeFi and MEME coin developers through grants and incubators;

Solana’s Breakpoint conference is also often a source of inspiration for Meme coins. Remember when Toly wore a green cartoon dragon costume at the conference two years ago, which sparked a wave of attention to the phenomenal Meme SillyDragon?

The founder took the initiative to set up an image, intentionally or unintentionally hinting at some kind of meme association, which has gradually become a common way of playing today.

The community culture has also "reserved" its Meme soil. Through social media (such as X) and Meme coin competitions, Solana has become a paradise for "grassroots players", and PEPE, BONK and POPCAT have also successfully formed positive feedback.

Users’ minds are framed as “Solana = trading”, and all kinds of mixed Devs are flocking in, making the emergence of Pumpfun seem more logical.

Let’s talk about Base.

There are also memes on Base, and there were also many eye-catching tokens in the ecosystem during the last wave of AI Agent craze, but this is more like the result of the previous Solana capital overflow and arbitrage behavior with low PVP difficulty.

Data from March showed that 51% of transactions on Base were token transfers. The deeper reason lies in the interest relationship between Coinbase and Circle.

Coinbase and Circle jointly established Centre Consortium in 2018. This organization is specifically responsible for the issuance and management of USDC. As co-sponsors, Coinbase and Circle not only jointly promoted the popularization of USDC, but also formulated the operating standards of USDC through Centre.

As the "son" of Coinbase, Base has become the preferred channel for USDC transfers.

In addition, Circle's recently filed IPO documents show that Coinbase and Circle's cooperation on USDC has a clear profit sharing - Coinbase takes 50% of the remaining profits from USDC reserves.

This means that every time Coinbase settles a USDC transaction or promotes the use of USDC, it can get a bigger share of the pie.

Base's low cost and high efficiency are just right for this "bookkeeping" requirement - whether it is the transfer of funds within Coinbase or the user's USDC transaction, Base can efficiently record and manage these on-chain activities, such as transfer records, liquidity management and settlement operations. This "bookkeeping" not only reduces Coinbase's operating costs, but also directly generates income through the revenue sharing of USDC.

Looking at the ecological culture, Base is more inclined to serve institutions and compliant users. Most of Coinbase's 100 million+ users are "serious players", and developers will naturally not choose Base to hold a "dog-beating party".

From the very beginning, Base was strategically destined by Coinbase and Circle to be the “accountant” of USDC, and was firmly framed by the interest chain of this pair of partners.

Finally, speaking of Ethereum, it is undoubtedly an old and disappointing topic.

Nearly 40% of transactions are related to cross-chain bridging, making it a "transit station" for other public chains.

The price of ETH is more like being roasted on a fire and gradually losing moisture. Although Ethereum is still the leader of DeFi, with a locked value (TVL) accounting for more than 60% (Syndica data), the negative sentiment in the community is spreading.

Technically, Ethereum’s “bridge fate” is forced by high gas fees.

When the market is good, ordinary users have long been overwhelmed and can only transfer their assets to lower-cost chains through cross-chain bridges; not to mention that when the market is bad, there is nothing to play with.

In addition, ETH's mainnet throughput is also limited, far inferior to Solana's high performance, and low transaction efficiency further increases the demand for cross-chain.

The deeper reason comes from the divergence of historical status.

As the earliest smart contract platform, Ethereum has accumulated the most assets and dApps, and naturally becomes the hub of the cross-chain bridge.

Ecological path dependence has caused DeFi projects and funds to concentrate on Ethereum, but high costs have forced users to leave, and bridging has become an "inevitable choice."

At the same time, the rise of Layer 2 diverted users, the Ethereum Foundation made multiple rounds of adjustments, Vitalik was accused of being unprofessional when he appeared in the same frame with a woman, and the price of the currency fell, and even breathing was wrong...

The dream is to be the "world computer", the current situation is the "cash machine".

Its fate seems to be locked by network effects and market changes, and it has changed from a DeFi overlord to an asset transfer station. Ethereum’s road to breakthrough is probably more difficult than Solana and Base.

Accept your fate and find your anchor

The public chain competition in 2025 is no longer the frenzy of a hundred-chain war, but the calmness of stock game.

The way for public chains to survive, in the final analysis, is to "accept fate and find an anchor."

Transactions can be anchor points, the circulation of stablecoins can be anchor points, and even cross-chain can be anchor points. However, the solidification of "anchor points" also means that the imagination space of public chains is compressed.

Can Solana shake off the label of “Meme Casino”? Can Base break out of the “bookkeeper” box? Can Ethereum break out of the “transfer station”?

There are no answers to these questions.

But what's even more ironic is that most P-boys don't care about these issues.

They will go to the chain that is popular to "beat the dog", and go to the chain that has arbitrage space to "pick the wool". The competition among public chains is actually just the background board behind every passerby who is eager to realize and look forward to a thousand-fold return.

Perhaps, only the arrival of the next cycle can give the real answer - whoever can bring in incremental growth can find a new "anchor point".

The future of the industry and the future of public chains remain undecided.