Author: Nancy, PANews

Huma is a legendary bird that appears in Middle Eastern and Persian mythology, symbolizing hope, holiness and luck. According to legend, Huma never lands on the ground, and anyone who is lucky enough to be passed by its shadow will be given the fate of a king, which is the inspiration behind the name of Huma Finance.

As one of the most popular PayFi protocols, discussions surrounding Huma Finance’s product mechanism and development path have continued to heat up recently. There are both affirmations of its innovative model and doubts about its transparency and profit mechanism.

Recently, PANews interviewed Richard Liu, co-founder of Huma Finance, to help everyone have a more comprehensive understanding of Huma's operating logic, development status, and views and judgments on the future of the entire PayFi track.

Using on-chain technology to break financial barriers and gain support from the Solana Foundation

Richard is a compound entrepreneur who has experience in entrepreneurship, venture capital and top technology companies, with a deep technical background and insights into the financial industry.

During his nearly eight years at Google, Richard led several innovative projects from "0 to 1", including Google Fi, which is used by many cross-border users. In 2016, he left Google and joined the entrepreneurial wave, co-founding the intelligent career development platform Leap.ai and serving as CEO. He used AI technology to accurately match jobs for tens of thousands of job seekers. The project was later acquired by Facebook (Meta).

Later, Richard joined the financial technology company EarnIn as CTO, a platform that helps users "advance wages". It was this experience that planted the key seeds for him to establish Huma Finance in the future.

"Chinese people like to save, but many Americans live paycheck to paycheck. If their child has a birthday or an emergency happens, they really may not be able to come up with the money. When they can withdraw their salary in advance through an app, the gratitude and happiness they feel is the motivation we feel every day," Richard recalled in the interview.

EarnIn's annual lending volume is as high as $10 billion, but even such a large-scale, healthy and profitable company faces the traditional financial system's rejection of financing for emerging Fintech companies. "You can't get money from banks, so you can only look for PE (private equity), but when they find out that you only have one or two lending channels, they will 'strangle you'. The terms are harsh and there is little room for growth."

This experience made Richard realize a serious imbalance: high-quality financial assets are often only in the hands of a few people such as PE, funds, and Family Office, while ordinary users cannot participate in them. At the same time, these assets could have provided more liquidity to the market and created income for the public.

Richard also began to think, can we use blockchain to put these assets on the chain? On the one hand, it provides enterprises with a wider range of financing channels, and on the other hand, it allows ordinary people to access high-quality investment opportunities that were originally excluded. But he also realized that not all assets are suitable for blockchain. "Many crypto users can accept the risk of cryptocurrency fluctuations, but have almost zero tolerance for credit risk." Therefore, he chose to focus on the payment financing field with extremely low credit risk and extremely short cycle.

In April 2022, Richard officially co-founded Huma Finance. The project initially started with DeFi lending protocols, attempting to bring the huge financial needs of the real world onto the chain, and using fintech companies as the main service group. In the continuous exploration, the team gradually focused on payment financing, with the core consideration being that its credit risk is extremely low and the cycle is clear.

In 2024, when the Solana Foundation listed PayFi as a strategic priority, Richard met with Lily Liu, the chairman of the foundation. Lily made it clear that "you understand the underlying logic of payment financing, which is a perfect fit with Solana's strategy. You should come to Solana to build, and we fully support you."

"We are a multi-chain platform, but Solana is currently the main battlefield." Richard also emphasized in the interview that Solana provides an ideal environment for Huma Finance's high-frequency PayFi clearing business. What really surprised the team was the Solana Foundation's active response and substantial support during the cooperation process. For example, when Huma Finance just connected to the Solana ecosystem and was not familiar with the technology, Solana arranged an excellent team of engineers to assist in development. At the same time, in the early stage of on-chain financing, Solana introduced many early LPs (liquidity providers), and the introduction of large institutions established trust for on-chain financing. In addition, Huma Finance and the Solana Foundation plan to jointly organize five PayFi ecosystem conferences to promote the progress of the industry.

“Solana has done everything, whether it’s technical issues or institutional resource docking, and many things have even exceeded our expectations.” Richard said frankly. Today, Huma Finance has become a banner of PayFi in the Solana ecosystem.

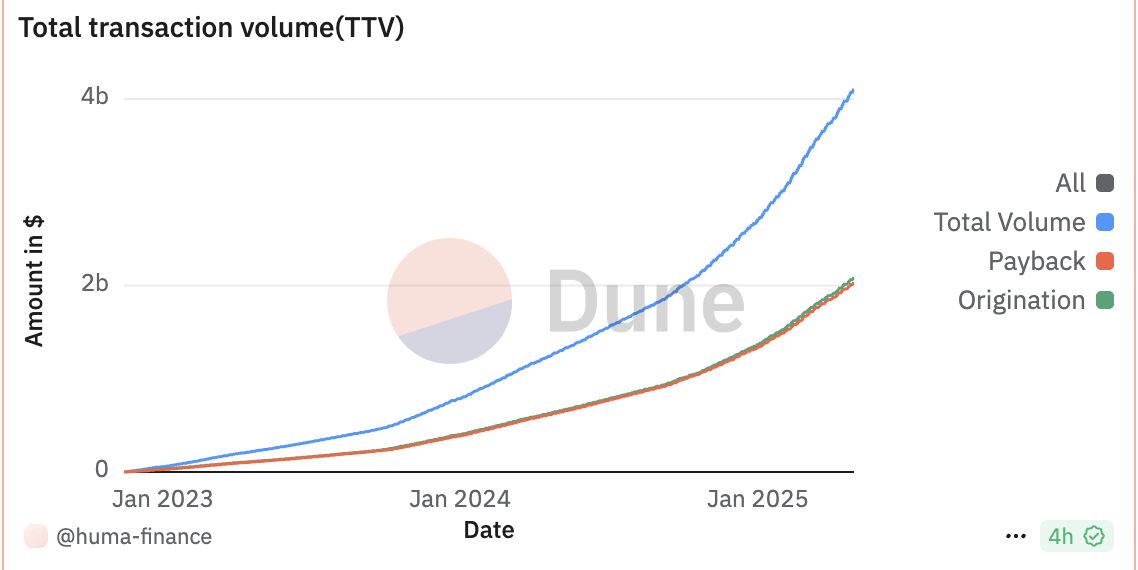

For Richard, Huma Finance is not only a continuation of the mission from the EarnIn era, but also a natural extension of his many years of cross-border experience in technology and finance. So far, Huma Finance has publicly obtained more than US$46 million in financing, and the transaction volume on the chain has exceeded US$4 billion.

Focus on cross-border payment advances and credit card business, and create a strategic closed loop of platform + application

In the interview, Richard introduced that Huma is the first PayFi network, mainly because it has a strong PayFi infrastructure, especially in the financing layer, and a series of self-operated and third-party applications. The core application scenarios of the PayFi ecosystem can be divided into three major sectors: cross-border payment advances, credit cards, and trade financing. At present, Huma Finance mainly focuses on cross-border payment advances and credit cards.

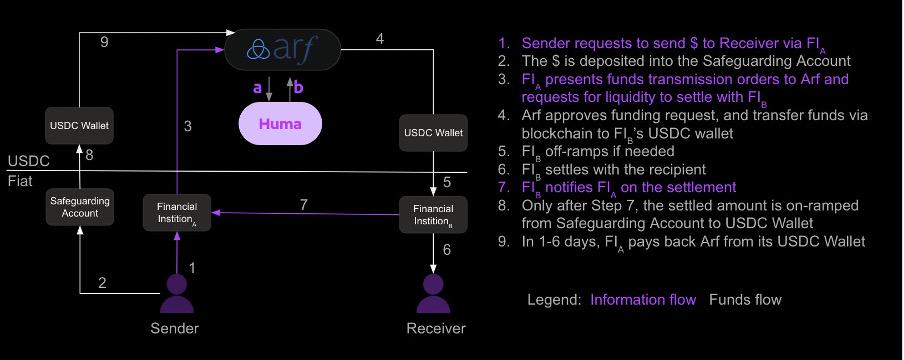

In response to questions about Huma's profit mechanism, Richard pointed out that in terms of cross-border payment advances, Huma Finance, through its subsidiary Arf, focuses on providing short-term advances for payment companies. The account period for such business is usually only a few days, with higher capital efficiency and more controllable risk characteristics. Richard pointed out in the interview that the industry itself has formed a stable price structure: remittances through SWIFT usually cost RMB 20 to 60 per transaction; while remittances through payment company channels cost between 2% and 5%. The daily lending rate between payment institutions is about 10 basis points per day.

"At Huma, users usually pay 6 to 10 basis points of funding costs per day, which is a very common price in the current industry. In addition to the reasonable price advantage, we also use stablecoins as the underlying clearing, combining the natural advantages of blockchain and stablecoins into the system to build an efficient and secure clearing system, which is also a technical innovation of the existing order." Richard said frankly that cross-border payment advances are a supermarket with a volume of up to 4 trillion US dollars. Precisely because the market base is extremely large, and the scale of advance business currently handled by Huma Finance is still small, it will not have a significant impact on the overall price level of the industry for the time being. Only in the future, as the platform transaction volume grows to tens of billions or even hundreds of billions, it may promote changes in the industry's cost curve. Of course, in addition to Huma Finance, other competitors will gradually leverage more low-cost sources of funds by improving brand trust and optimizing the capital cost structure, triggering changes in the market structure.

In addition to cross-border payment advances, Richard believes that another greater opportunity exists in the field of credit card advances, a huge market of up to 16 trillion US dollars. Taking the United States as an example, after consumers swipe their cards, the issuing bank must settle the funds to the merchant account through the payment network within 2-3 days. Some emerging markets such as Brazil even delay up to 30 days. Before the user actually repays the loan, the bank actually bears the responsibility of advance payment during this period. At the same time, there is also a waiting period for funds on the merchant side. But many merchants are actually willing to pay a sum of money to realize the immediate arrival of funds.

Richard said that he and his co-founder Erbil have experience in issuing cards, and have been deeply involved in the design and implementation of the credit card payment chain, whether in cooperation in the Google Pay system or in leading the card issuance business in EarnIn. In other words, the team not only has the ability to understand the complexity of this industry, but also has the experience of polishing products and models from the bottom up.

Regarding trade finance, Richard pointed out in the interview that although Huma Finance's system is technically capable of supporting trade finance, this type of business generally has long account terms and slow capital turnover, which does not conform to Huma Finance's current "high frequency, short cycle" strategy, so it will not be directly involved for the time being.

In terms of access to funds, Huma Finance was mainly aimed at professional investors or institutions before Huma 2.0. With the recent launch of Huma 2.0, it is open to retail investors under the premise of compliance, and users can choose Classic mode or Maxi mode. Richard believes that this is not only an expansion at the product level, but also a deep fit with the core concept of community ownership.

At the same time, considering that users generally do not want their funds to be forcibly locked, Huma has also made a design balance: although B-side assets usually have a fixed account period (such as three months) and cannot be withdrawn at any time, in addition to using about 80% of the funds to pay for transaction financing, the platform will allocate about 20% of the assets as high-liquidity assets to meet users' redemption needs at any time.

“We will not force users to lock their positions. This is their clear feedback to us. In order to ensure smooth redemption, we will reserve a certain proportion of liquid assets, and the redemption process can usually be completed within 1 to 2 days.” Richard emphasized.

In addition, regarding Huma Finance's choice to actively embrace the DeFi mechanism in the early financing stage instead of dealing only with traditional financial institutions, Richard explained that unlike traditional financial institutions with low communication efficiency and long response cycles, DeFi provides a highly transparent and high-speed financing path. "Anyone who does financial asset allocation knows that it is not easy to scale up assets, especially in the early stages. Traditional financial institutions have slow processes and complex docking, and the snowball rolls slowly. There is a large amount of funds in the market willing to support high-quality assets, but under the traditional system, there is a lack of transparent and convenient channels for participation. We are willing to display asset data completely transparently on the chain, so as to gain the trust and financial support of the DeFi community, which will greatly help our development speed."

In addition to efficiency and transparency, Richard also emphasized the value of community co-building. He said that Huma Finance highly recognizes the power of the community, especially in enabling retail investors to participate in high-quality asset opportunities under the premise of compliance. "What attracts me most about Web3 is that it can achieve true community co-building and sharing. In the traditional financial system, such a mechanism is almost impossible to exist." Richard added.

"Google currently uses the Android platform and core applications such as Gmail, YouTube, and Search as ecological anchors to support the platform's growth and user stickiness. Similarly, we hope that the PayFi platform will not only provide underlying capabilities and scalability, but also have core products that can be used to drive real demand and capital flow." Richard also emphasized in the interview that Huma Finance is not just trying to build a single product, but a PayFi infrastructure platform that can run a variety of products and applications, and its value is far greater than any independent application.

For this reason, Huma acquired its largest customer Arf, thus forming a closed-loop ecosystem of "platform + App". Richard believes that the value of the platform itself is far greater than a specific application. It can connect the capital side and the asset side and support financial innovation in more scenarios.

It is worth mentioning that Richard also mentioned Huma Finace's interim goals and implementation paths. Not long ago, Richard said that the platform's interim goal in 2025 is to achieve a cumulative transaction volume of more than 10 billion US dollars. He further stated, "At present, our main transaction increment comes from Arf's core customers. Although the platform has established a strong potential customer cooperation line, the landing and online launch of each customer requires a certain period of time, including the chain process, which often takes several months, involving the opening of bank accounts and local regulatory approvals. The process varies from place to place. Our focus now is how to accelerate this process. The team is also exploring a more efficient support system to speed up the customer access process."

On the funding side, Huma is also constantly optimizing the user experience and attractiveness. "After we launched Huma 2.0, the market feedback was very positive." Richard said that under the premise of controlled deposit quotas, the platform pool was full in a short period of time. The number of participating users and the participation in the Maxi mode exceeded expectations. The current activity and user interest on the funding side are very high. Once the quota is released and more large users are introduced to participate, there is ample room for growth. Next, the team's main focus will be on accelerating Arf customers' transactions on the chain, while promoting the on-chain deployment of credit card financing scenarios.

Introducing traditional financial risk control logic to create multiple lines of defense for asset security

Huma Finance has sparked heated discussions in the market due to its PayFi model, and some investors are worried that it may face the risk of default or bankruptcy.

In response to the market's doubts about asset security, Richard introduced that Huma Finance has drawn on the classic risk control logic of traditional structured finance, introduced the First-Loss Cover (first loss mechanism) and priority/inferior structure, and supplemented it with multiple protection mechanisms. The goal is to create a DeFi product system with institutional-level risk control capabilities, especially in the cross-border payment advance business of its core asset Arf.

Specifically, in terms of service object screening, Huma Finance's Arf business only serves licensed financial institutions in developed countries (such as the United States, the United Kingdom, France, and Singapore), avoiding areas with complex foreign exchange controls. These institutions must meet strict compliance requirements and have low credit risks, providing Arf with a basic level of risk barriers and reducing counterparty risks. At the same time, Huma Finance has developed a strict internal risk control rating system for all partner institutions, and classifies them (including level 1, level 2, and level 3) based on their financial status, remittance path stability, counterparty risk and other factors. Currently, it only serves customers with level 1 and level 2 ratings; in the operational process, the advance payment object must receive the customer's remittance in advance, and the funds will be deposited into a special account, which is regulated by the bank and is limited to this cross-border transaction. Huma Finance will only release funds for payment after verifying that the funds have indeed arrived and meet the previous risk model assessment; in terms of legal structure isolation, the assets involved in Arf are managed by an independent SPV (special purpose vehicle), which is completely isolated from the assets of Huma Fiance or Arf's main company. Even if Arf goes bankrupt, user assets are still protected by law; in terms of the payment period response mechanism, Huma Finance's payment period is designed to be extremely short, and advance payment and recovery are usually completed within a few days. Once an institution shows signs of delayed payment, credit changes, etc., the system can quickly adjust its credit limit or even suspend its credit limit to ensure that risks are identified and controlled at an early stage. Historical data shows that the bad debt rate of the financial system has been only 0.25% in the past 20 years, and Huma Finace chooses to provide short-term payment period services to developed countries, which means a lower bad debt rate.

Even in the face of possible large-scale redemptions or systemic risk events, Richard pointed out in the interview that Huma Finance has also designed several emergency mechanisms: for example, a 2% margin has been clearly set up in Arf to cover several times the regular bad debt rate, which is gradually established by the platform's profit accumulation and is used first to cover possible bad debt risks; regardless of whether the user's funds are locked or not, in extreme scenarios, they are all "fairly liquidated" to avoid structural unfairness caused by "first runners profiting"; if the cooperative institution defaults or goes bankrupt, since the customer funds are always in isolated accounts and circulated in the regulatory system, Huma Finance has the ability to recover most or even all of the funds through legal means. This mechanism has not been actually triggered in history, but from the perspective of legal structure and process, it is realistic and feasible.

In addition, in terms of transparency, Richard revealed that all funds of Huma Finance are held in Fireblocks wallets, flowing to pre-defined compliance paths, and requiring multi-signature approval to ensure that funds are not misappropriated. Not only that, the flow of funds can be traced in real time through the blockchain. Currently, Huma Finance has disclosed some information in the Dune Dashboard, and will gradually improve the dashboard in the future to show more detailed fund dynamics. In addition, Huma Finance publishes a monthly fund flow report to disclose the allocation and use of funds in the pool. In the future, it is also planned to write it into the smart contract to further improve transparency and auditability through decentralization.

It can be seen that the core logic of Huma Finance does not rely on market sentiment or Ponzi cycles to support its liquidity, but through multiple risk control layers, legal structures and own capital buffers, it establishes a DeFi financial ecosystem with high resilience and accountability. Although extreme risks can never be completely avoided, its systematic buffer mechanism and liquidation principles are designed to build multiple lines of defense for the safety of user assets.

Strengthening community building and user education is the biggest challenge at present

"Disrespect for the community and users is an absolute red line for Huma Finance, and sincerity is a sharp weapon that penetrates all noise." After the recent community controversy caused by the communication method of team members, Richard immediately issued an open letter in response, and in the interview further elaborated on the team's reflections on community building and future improvement directions.

On the one hand, Richard frankly admitted that communication problems arose due to the mismatch between people and positions. "Our colleague is very hard-working and creative, but I put her in an inappropriate position - responsible for external community communication. This is not her strong point, and I should have realized it earlier." For this reason, Richard readjusted the external communication responsibilities. Richard will be responsible for the communication of the Chinese community, while the English community will be handed over to another co-founder, Erbil Karaman.

"We believe that community communication is one of the most critical tasks of a Crypto company. Lianchuang best represents the company's mission and values, and they must be at the forefront of community communication." This adjustment is also Huma Finance's direct response and structural repair to past problems.

Not only that, Richard also emphasized that the team has reached a consensus internally: every feedback from the community, no matter how it is worded, deserves to be listened to and reflected upon. "We should maintain a healthy attitude towards community accusations and try to understand their real concerns. We should either explain it clearly or admit that we are not doing well enough and actively improve it. For example, on the issue of transparency, we did not give transparency a high enough priority in the past. In the future, we will improve this aspect and ensure that information disclosure is clearer and more systematic."

At the end of the interview, Richard also shared his overall views on the PayFi track, especially the key to bridging the gap between traditional finance and DeFi, as well as the challenges and solutions faced in the process of user education and adoption.

"The core of PayFi is to use blockchain technology to serve the payment and financing needs of the real world." Richard pointed out that although many financial institutions and payment companies are very interested in this model, the actual implementation is often stuck in the most traditional links - compliance and bank account system.

He further pointed out that compliance and the path of funds in and out of the chain are the most critical middleware in the entire ecosystem. If Hong Kong can introduce clearer relevant legislation to allow local payment companies to legally and conveniently access on-chain services, this will not only be a breakthrough for Hong Kong, but will also greatly promote the development of the entire PayFi ecosystem.

In addition to opening up interfaces with traditional finance, Richard also said, "We not only hope that users will invest their money in the Huma Finance platform, but more importantly, whether these PayFi assets can 'go out' in the DeFi ecosystem and become the core assets of the entire DeFi world."

But between ideal and reality, there is still a most difficult threshold to cross - user education. "This is actually the biggest challenge we are facing now." Richard said frankly that for DeFi users, they are accustomed to the "coin issuance logic" of high APY, and are unfamiliar with PayFi's income structure based on real lending and no coin issuance subsidy. "Even if I tell them that it can actually generate 12.5% of income here, which is higher than many on-chain protocols, their first reaction is often: Are you doing a Ponzi scheme? Is it fake?" For traditional financial practitioners, they have doubts about the entire DeFi technical path. "Many people will ask me directly, why can't I use a fiat currency account to complete the operation directly? Why do I have to use stablecoins?" Once it comes to stablecoins or on-chain liquidation, they hesitate because of unclear supervision.

Richard pointed out that this "cognitive misalignment" stems from the unfamiliarity of the two circles with each other's language and logic. "This also means that our team needs to speak two 'languages' at the same time, using both DeFi's professional terms and the language of traditional finance. PayFi has a long way to go, and we need to work with the community to produce more content so that more people can better understand PayFi, build this track together, and develop PayFi into the most successful application of Crypto in real life as soon as possible."