Original title: What’s wrong with CDP stablecoins on HyperEVM?

Original author: @stablealt

Original translation: zhouzhou, BlockBeats

Editor's note: CDP "stablecoins" on HyperEVM such as feUSD and USDXL cannot maintain a $1 anchor price due to the lack of a strong arbitrage mechanism, weak demand in Hyperliquid, and low borrowing costs, causing their prices to fall below $1. Hyperliquid natively provides leveraged trading, and users do not need CDP stablecoins. As airdrops and point rewards are exhausted, CDP tokens will lose value and eventually fail to exist.

The following is the original content (for easier reading and understanding, the original content has been reorganized):

Disclaimer: This article is not intended to FUD or attack HyperEVM's CDP protocol.

In short: CDP stablecoins, such as feUSD and USDXL, are not actually stable or capital efficient. They lack strong arbitrage mechanisms, have limited use cases, and are mainly used for leveraged trading, while Hyperliquid already natively provides better user experience and liquidity. As a result, these tokens are trading below their $1 pegs, and without incentives like airdrops, they will likely fade away.

Collateralized debt position (CDP) stablecoins promise to provide a decentralized alternative to dollar-backed stablecoins like USD and USDT or centralized synthetic dollars like USDDe, but the reality is often not as expected. feUSD, USDXL, and KEI are some of the latest examples that have tried to emulate Liquity, but they all face serious issues such as peg stability, scalability, or incentive design flaws.

This article will analyze what these problems are, what paid influencers don’t tell you, and why these problems are more than just growing pains—they are structural problems.

CDP Design Overview

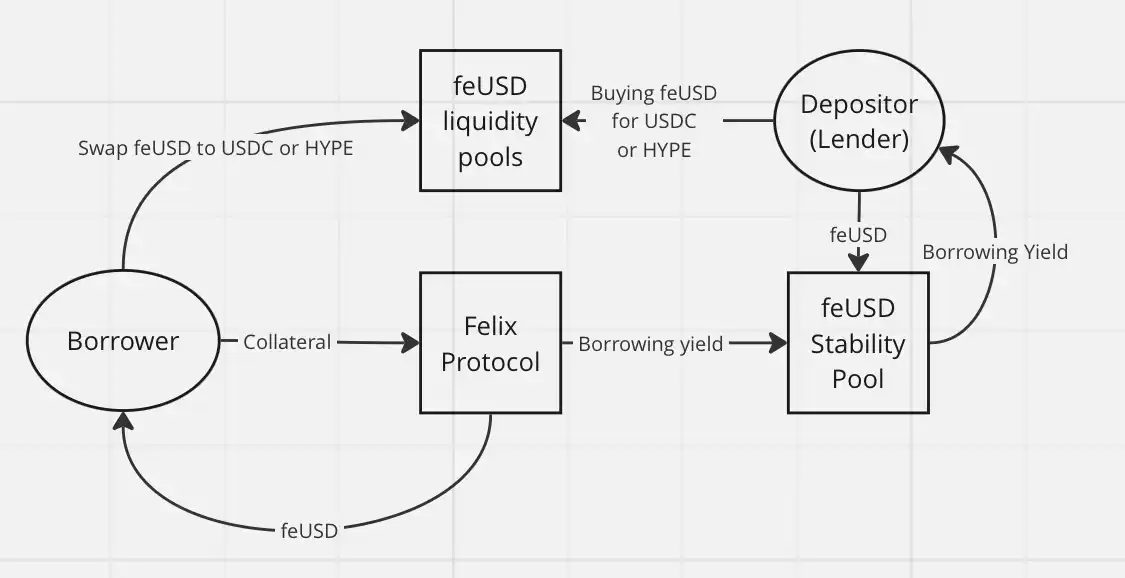

First, let’s understand the basic concept: CDP “stablecoins” are not actually true stablecoins or “USD” tokens. This is why DAI is called “DAI” instead of USDD or other names. It is wrong to name CDP stablecoins with the “USD” prefix, which may mislead DeFi newcomers. They have no arbitrage mechanism and no direct guarantee. Each CDP token is minted out of thin air and may be worth far less than $1.

To mint one CDP token, users must lock up more than 100% of the value of collateral in order to borrow tokens. This reduces capital efficiency and limits growth. In order to mint 1 token, you need to lock up more than $1 in value. Depending on the loan-to-value ratio, this ratio can be higher.

Without adding heavy-handed mechanisms like Felix’s redemptions (when arbitrageurs can steal someone’s collateral if the borrowing rate is too low) or Dai’s PSM module, CDP tokens simply cannot maintain a 1:1 peg to the USD, especially when their main use case is leveraged trading.

In DeFi, CDP is just another form of lending. Borrowers mint CDP stablecoins and exchange them for other assets or yield strategies that they believe can exceed the protocol's lending rate.

what happened?

Everyone swaps their CDP stablecoins for other assets, usually more stable centralized assets like USDC or USDT, or for more volatile assets like HYPE for leveraged trading. It doesn’t make sense to hold these tokens, especially if you have to pay borrowing rates: 7% annualized yield (APY) on feUSD on Felix and 10.5% APY on USDXL on HypurrFi.

Take USDXL as an example: it has no local use case, and users have no reason to hold it. That's why it can fluctuate at prices like $0.80, $1.20, etc. - the price is not anchored by any real arbitrage mechanism. Its price simply reflects the demand of users to borrow HYPE. When USDXL is trading above $1, borrowers can borrow more USD; when it is below $1, borrowers can borrow less - it's that simple.

feUSD is slightly better. Felix provides users with a stable pool where users can earn 75% of the returns from borrowing fees and liquidation bonuses, which is currently around 8% annualized. This helps reduce price volatility, but like USDXL, there is still no strong arbitrage mechanism to keep feUSD firmly at $1. Its price still fluctuates based on borrowing demand.

The core problem is this: users who buy feUSD and put it into the stability pool are essentially lending their USDC or HYPE (via Felix) to the people who minted feUSD. These CDP tokens have no intrinsic value. They only have value when paired with valuable tokens like HYPE or USDC in a liquidity pool.

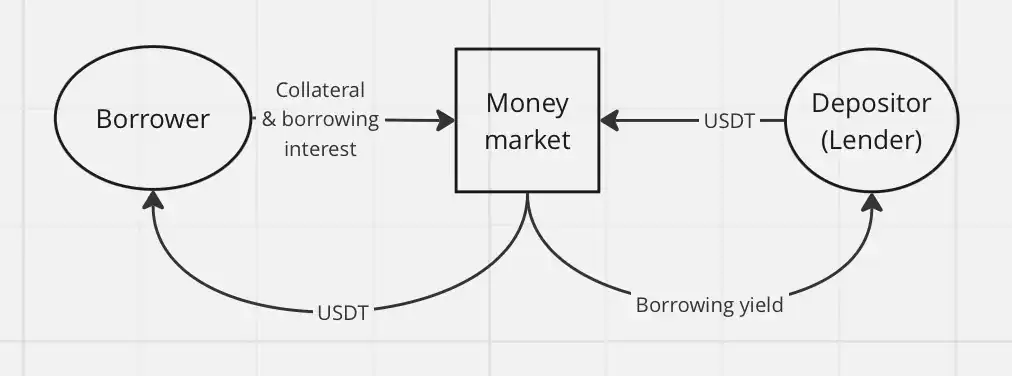

This introduces third-party risk, and without airdrops or other incentives, there is really little reason for DeFi users to borrow illiquid, unpegged tokens like feUSD or USDXL, or to buy them as exit liquidity for borrowers. Why would you do this when you can just borrow stablecoins like USDT or USDDe directly? The stablecoins you borrow will eventually be converted into other tokens anyway, so you don’t need to care about the decentralization of the borrowed assets.

Classic lending through the flywheel mechanism of money markets, such as Hyperlend, is much simpler and has the same economic effect for the end user.

Another reason why CDP did not succeed in HyperEVM is that leveraged trading is already a native feature of the Hyperliquid ecosystem. On other chains, CDP provides decentralized leveraged trading. On Hyperliquid, users only need to use the platform itself, take advantage of leveraged perpetual contracts (perps) and excellent user experience, and do not need to rely on CDP stablecoins.

With Hyperliquid, there is no need to use a third-party protocol for leveraged trading. The only use case I see for CDP is for leverage farming and HLP recycle operations.

To summarize, here are the reasons why CDP “stablecoins” on HyperEVM perform poorly:

Lack of strong arbitrage mechanism

Weak demand for CDP products in Hyperliquid

Low borrowing costs and no reason to hold CDP tokens

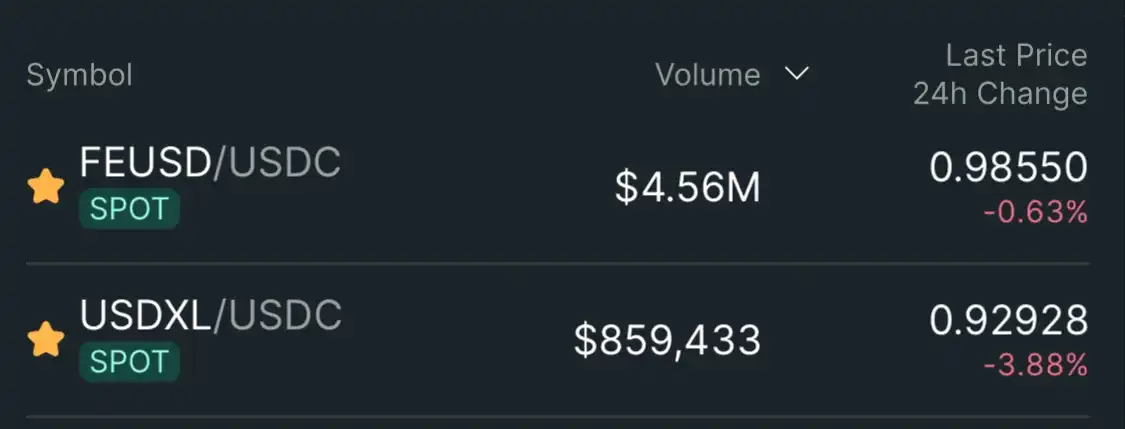

As a result, CDP “stablecoins” like feUSD and USDXL are trading below their soft pegs of $1: feUSD at $0.985 (-1.5%) and USDXL at $0.93 (-7%).

Conclusion: I don’t think CDP stablecoins have any potential in the Hyperliquid ecosystem. Users don’t need them — Hyperliquid already provides a better user experience and deeper liquidity, with native support for leveraged trading. Once the airdrop and points reward program are exhausted, CDP tokens will lose their remaining use value.

Hypurrliquid, don’t do exit liquidity.