Compiled by: Aiying

Galaxy Research released the "Cryptocurrency Lending Status" report on April 14, 2025, which summarizes 24 years of annual data. The following is the full text of the report: Lending is an application scenario of cryptocurrency, which has found strong market fit both on-chain and off-chain. At the peak of the entire market, the size of the lending market exceeded US$64 billion. The lending market plays an important role in building a financial ecosystem based on digital assets, allowing users to obtain liquidity for their holdings through lending, so as to deploy them in decentralized finance (DeFi), or trade on on-chain and off-chain platforms.

This report explores the on-chain and off-chain cryptocurrency lending markets in two parts: Part I reviews the history of the crypto lending market, market participants, historical size (both on-chain and off-chain), and some key moments in the space. Part II provides an in-depth analysis of how some lending products and other sources of leverage work in both on-chain and off-chain environments, who uses these products, and the risks of each product. This report presents a comprehensive picture of the crypto lending market, shedding light on this most widely used but opaque area of the crypto economy. Most importantly, the report provides a rare perspective on the size of the off-chain lending market, a historically relatively opaque part of the crypto industry.

I. Key conclusions

The overall size of the crypto lending market remains significantly below the peak at the end of the 2020-2021 crypto bull market. As of the fourth quarter of 2024, the size of the crypto lending market, including crypto collateralized debt positions (CDP) stablecoins, was $36.5 billion, down 43% from the all-time high of $64.4 billion in the fourth quarter of 2021. This decline can be attributed to the collapse of lenders on the supply side and the shrinking of funds, individuals and businesses on the demand side.

As of the fourth quarter of 2024, the total size of the crypto lending market is 36.5 billion US dollars. The top three centralized financial (CeFi) lending institutions include Tether, Galaxy and Ledn. The loan book size of these three companies reached 9.9 billion US dollars at the end of the fourth quarter of 2024, accounting for 88.6% of the CeFi lending market (Tether accounts for about 73% of it, reaching 8.2 billion), and the main proportions of the market size are:

- Centralized Finance (CeFi) lending: $11.2 billion,

- Decentralized Finance (DeFi) lending: $19.1 billion

- Crypto-backed Collateralized Debt Position (CDP) Stablecoins: $6.2 billion

Since the crypto bear market trough in Q4 2022, when on-chain lending was $1.8 billion, on-chain lending applications have experienced strong growth. As of Q4 2024, total open borrowings across 20 lending applications and 12 blockchains totaled $19.1 billion. This means that in eight quarters, DeFi borrowing has grown by 959%.

II. Market Overview

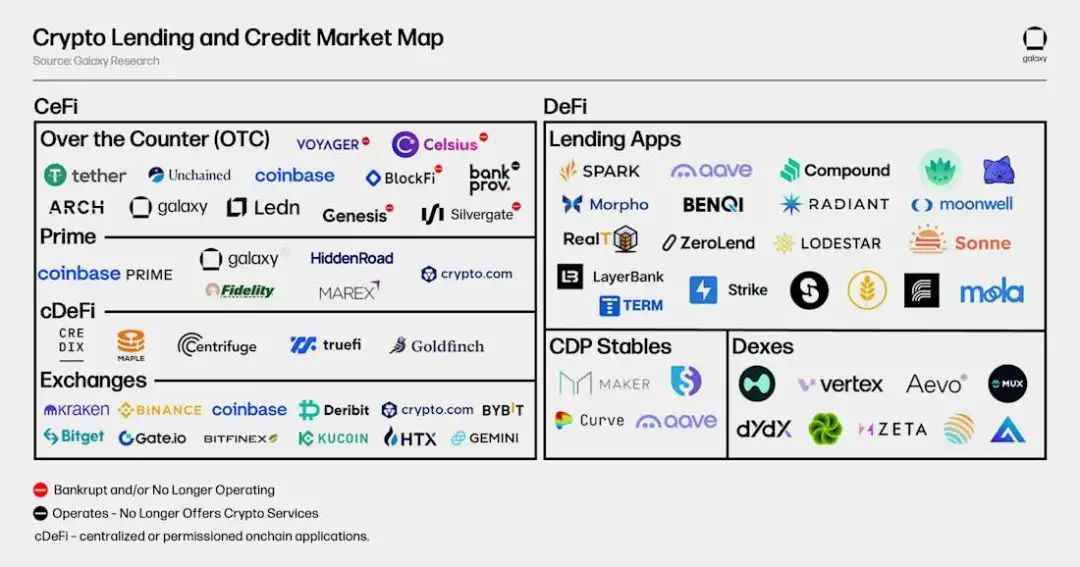

Crypto lending services are provided mainly through two channels: decentralized finance (DeFi) and centralized finance (CeFi). Each of them has unique characteristics and products provided. Here is a brief overview of CeFi and DeFi lending services:

1. Centralized Finance (CeFi)

CeFi is a lending service for cryptocurrencies and related assets provided by centralized off-chain financial companies. Some CeFi entities use on-chain infrastructure, or their entire business is built on-chain. CeFi lending can be roughly divided into three categories:

a. Over-the-Counter (OTC)

OTC transactions are provided by centralized institutions, offering a range of customized lending solutions and products. OTC transactions are bilateral transactions that allow borrowers and lenders to reach a personalized agreement on borrowing conditions, including interest rates, terms, and loan-to-value ratios (LTV). These products are usually only available to qualified investors and institutions.

b. Prime Brokerage

Prime brokerage platforms provide margin financing, trade execution, and custody services. Users can withdraw margin financing from prime brokers and use it elsewhere or on the platform for trading activities. Prime brokers typically only provide financing for limited crypto assets and crypto ETFs.

c. On-chain private credit

Allows users to pool funds on-chain and deploy them through off-chain protocols and accounts. In this model, the underlying blockchain actually becomes a crowdfunding and accounting platform to meet off-chain credit needs. Debt is usually tokenized as a collateralized debt position (CDP) stablecoin or directly through tokens representing shares of the debt pool. The use of funds is usually narrow.

2. Decentralized Finance (DeFi)

DeFi is a smart contract-driven application that runs on the blockchain and allows users to borrow, lend, or use leverage when trading against cryptocurrencies. DeFi lending and borrowing have the following notable features: 24/7 operation, a wide range of borrowable and collateral assets, and full transparency that can be audited by anyone. Lending applications, collateralized debt position stablecoins, and decentralized exchanges all allow users to gain leverage on the chain.

a. Lending Application

These on-chain applications allow users to deposit collateral assets (such as Bitcoin and Ethereum) in order to borrow other cryptocurrencies. The loan conditions are pre-set by the application through risk assessment and adjusted based on the collateral assets and borrowing assets provided by the user. On-chain lending and borrowing are similar to traditional over-collateralized lending.

b. Collateralized Debt Position Stablecoin

These stablecoins are over-collateralized, backed by individual cryptocurrencies or baskets of cryptocurrencies. The principle is similar to over-collateralized lending and borrowing, but synthetic assets are issued for the collateral deposited by users.

c. Decentralized Exchange

Some decentralized exchanges allow users to obtain leverage to magnify trading positions. Although decentralized exchanges function differently, the role of providing leverage is similar to that of CeFi prime brokers. Leveraged funds are generally not transferable from decentralized exchanges, but their role is similar to CeFi's financing services.

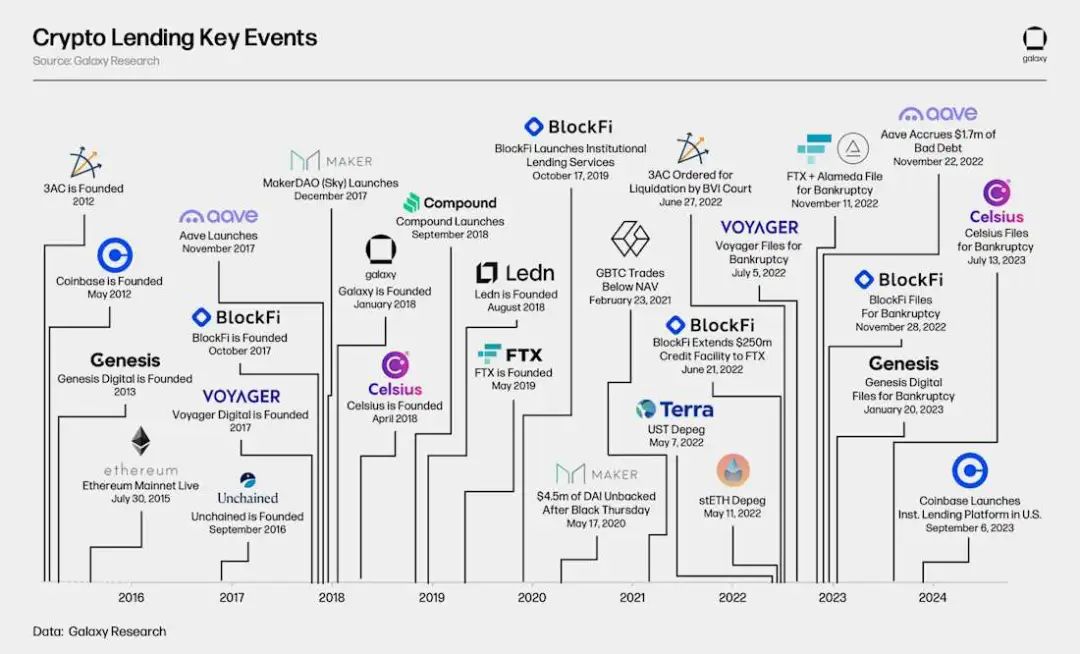

3. Market Development and History

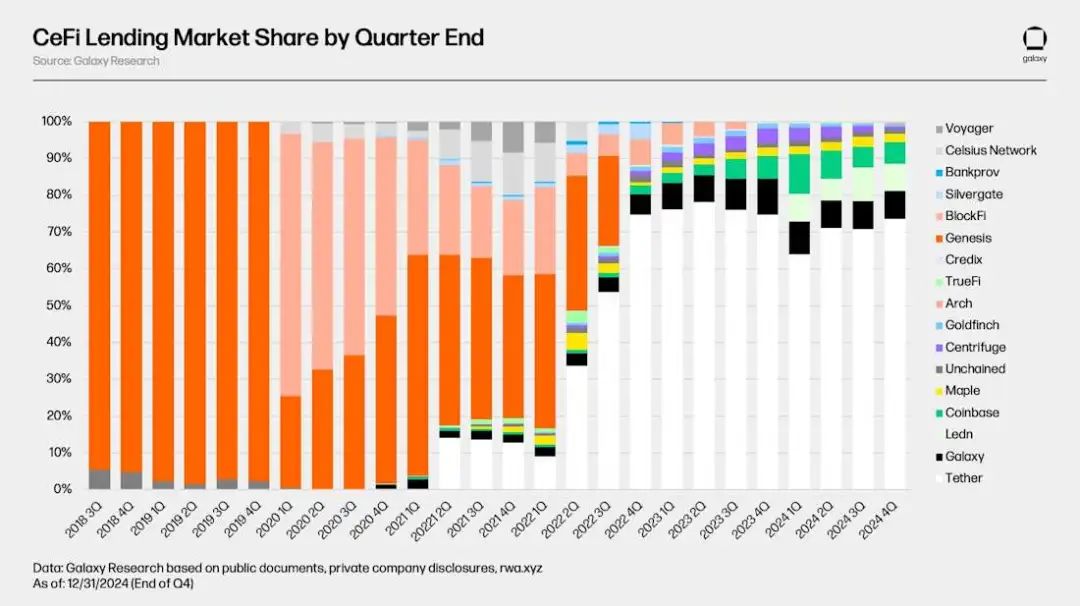

The following figure shows the main historical players in the CeFi and DeFi crypto lending markets. In 2022 and 2023, as crypto asset prices fell and market liquidity dried up, many of the largest CeFi lending platforms collapsed, notably Genesis, Celsius Network, BlockFi, and Voyager filed for bankruptcy in those two years. This resulted in an estimated 78% contraction in the CeFi and DeFi lending markets from the peak in 2022 to the trough of the bear market, with CeFi lending open borrowings falling by 82%. The following sections will delve into the historical evolution and size of the crypto lending market.

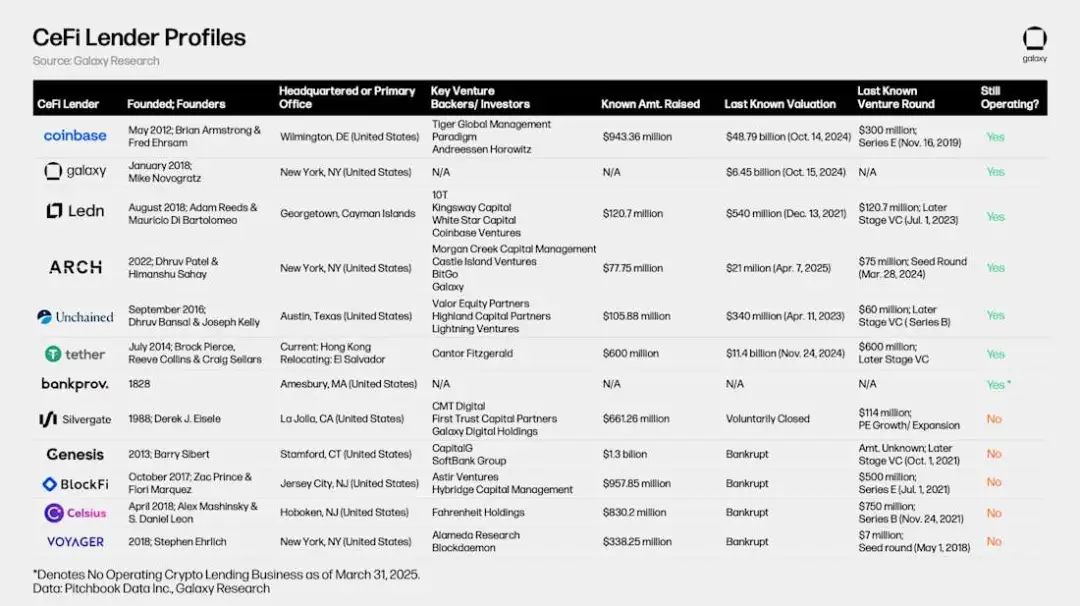

The table below compares some of the largest CeFi crypto lending institutions in history. Some of the listed companies provide multiple services to investors, such as Coinbase, which, although its main operation is a cryptocurrency exchange, provides credit services to investors through over-the-counter (OTC) cryptocurrency loans and margin financing.

4. History of Crypto Lending

Although on-chain and off-chain crypto lending did not become widely available until late 2019/early 2020, some of the current and historically important players were founded as early as 2012. Notably, Genesis was founded in 2013 and had a loan book of $14.6 billion at one point. On-chain lending and CDP stablecoin giants like Aave, Sky (formerly MakerDAO), and Compound Finance were launched on the Ethereum platform between 2017 and 2018. The emergence of these on-chain lending/borrowing solutions was made possible by the advent of Ethereum and its smart contracts, which were officially launched in July 2015.

The end of the 2020-2021 crypto bull run marked the beginning of a turbulent 18 months for the crypto lending market, which was plagued by bankruptcies. Several major events at this time included: Terra's stablecoin UST depegging, eventually becoming worthless along with LUNA; Ethereum's largest liquid staking token (LST) stETH depegging; and Grayscale Bitcoin Trust Fund (GBTC) began trading at a discount to net asset value (NAV) after years of trading at a premium.

5. Market size

The total size of the DeFi and CeFi crypto lending markets is still significantly lower than the peak level in the first quarter of 2022 (based on the end-of-quarter data). This phenomenon is mainly due to the weak recovery of the CeFi lending market after the 2022 bear market and the collapse of the largest lenders and borrowers in the market. The following analysis looks at the size of the crypto lending market from the perspective of CeFi and on-chain platforms.

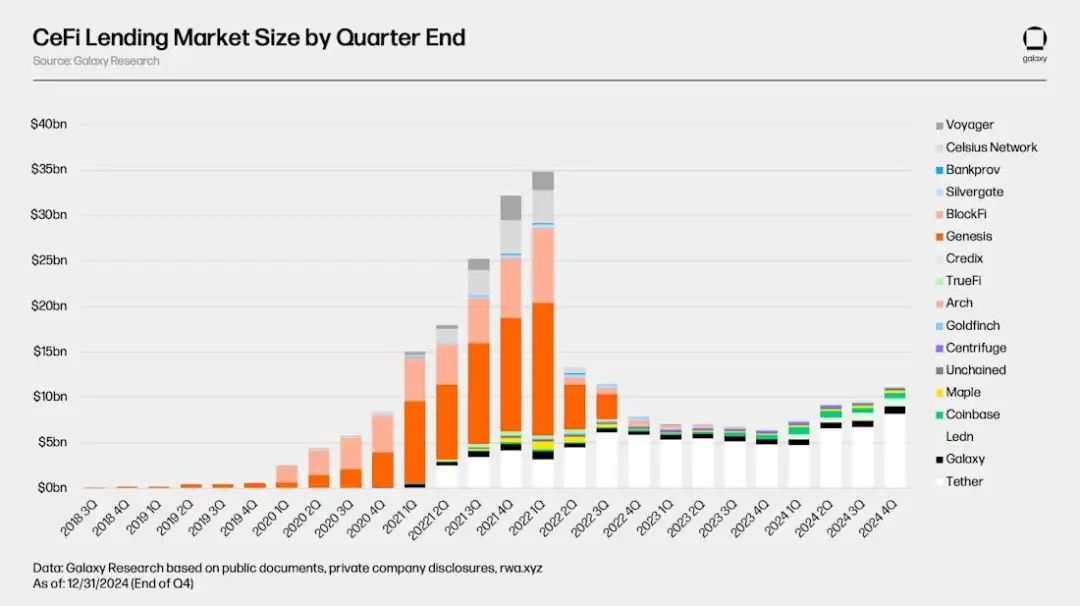

At the peak of the market, Galaxy Research estimated that the total loan book size of CeFi lending platforms with available data was $34.8 billion; at the market bottom, the size of the CeFi lending market fell to $6.4 billion (down 82%). As of the end of the fourth quarter of 2024, the total size of the CeFi lending market is $11.2 billion, down 68% from its historical high, but up 73% from the bear market bottom.

As the CeFi lending market has shrunk over the past three years, the number of outstanding loans has been concentrated on fewer lending platforms. At the peak of the CeFi lending market in the first quarter of 2022, the top three lending platforms (Genesis, BlockFi, and Celsius) accounted for 76% of the market, holding a total of $26.4 billion in loans out of $34.8 billion. Today, the top three lending platforms (Tether, Galaxy, and Ledn) still maintain 89% of the market share. As can be seen from the chart above, Tether accounts for about 73%.

When evaluating the market dominance of one lending platform versus another, it is important to note the differences between each platform, as not all CeFi lending platforms are the same. Some platforms only offer certain types of loans (e.g., Bitcoin-only loans, altcoin-only products, and cash loans that exclude stablecoins), only serve certain types of customers (e.g., institutional clients vs. retail clients), and only operate in specific jurisdictions. It is this combination of factors that allows some lending platforms to scale more massively than others.

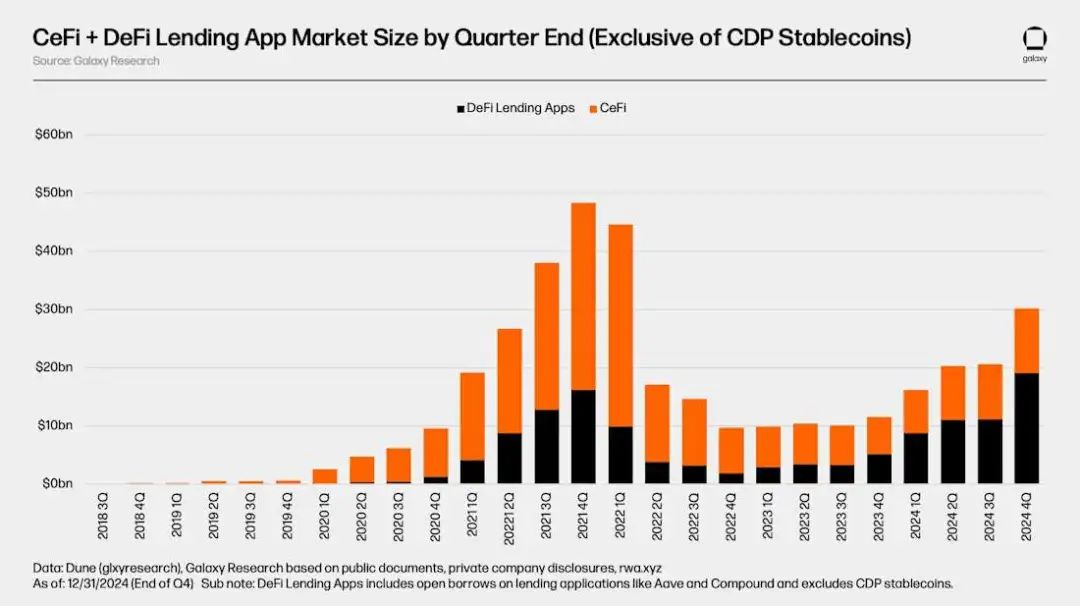

As shown in the chart below, on-chain applications such as Aave and Compound have achieved strong growth through DeFi lending, rebounding from $1.8 billion in outstanding borrowing at the bottom of the bear market to $19.1 billion in outstanding borrowing on 20 lending applications and 12 blockchains at the end of the fourth quarter of 2024. This is a 959% increase in DeFi lending over the past eight quarters since the bottom. As of the end of the fourth quarter of 2024, the total outstanding loans of on-chain lending applications have increased by 18% from the historical high of $1.62 billion set during the 2020-2021 bull market.

DeFi lending has recovered faster than CeFi lending. This can be attributed to the permissionless nature of blockchain-based applications and the fact that DeFi lending applications have survived the bear market turmoil, while many large CeFi lending platforms have declared bankruptcy and ceased operations. Unlike those large CeFi lending platforms that went bankrupt and ceased operations, many DeFi lending applications and markets were not forced to shut down and continue to operate. This fact is a testament to the design and risk management practices of large on-chain lending applications, as well as the advantages of algorithmic, over-collateralized, and supply-demand based lending models.

Excluding the crypto-collateralized CDP stablecoin market capitalization, the crypto lending market reached a peak of $4.84 billion in outstanding borrowings in Q4 2021. The market hit a trough of $960 million four quarters later in Q4 2022, down 80% from the peak. Since then, the total market size has expanded to $3.02 billion, driven primarily by the expansion of DeFi lending applications, an increase of 214% from the historical low in Q4 2024.

It is important to note that there is a potential double counting problem between the size of CeFi loan books and DeFi borrowing. This is because some CeFi platforms rely on DeFi lending applications to provide borrowing services to off-chain customers. For example, suppose a CeFi platform may use idle Bitcoin to borrow USDC on-chain, and then lend the same USDC to off-chain customers. In this case, the on-chain borrowing of the CeFi platform will appear in both the outstanding borrowing of DeFi and the outstanding borrowing of its customers in the platform's financial statements. Due to the lack of disclosure and clear labeling of on-chain attribution, it is very difficult to filter out such double counting.

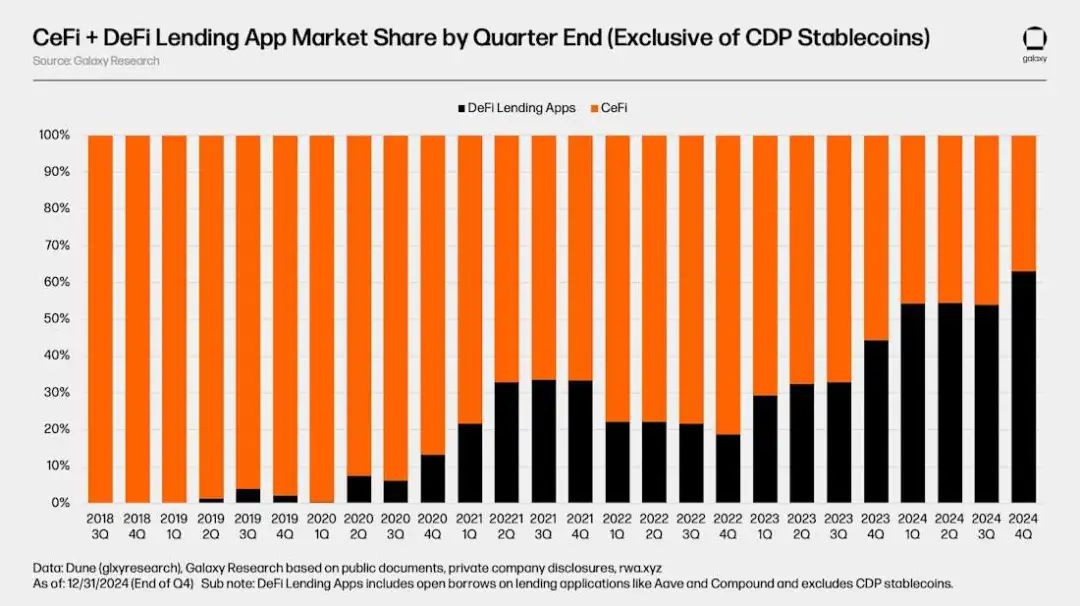

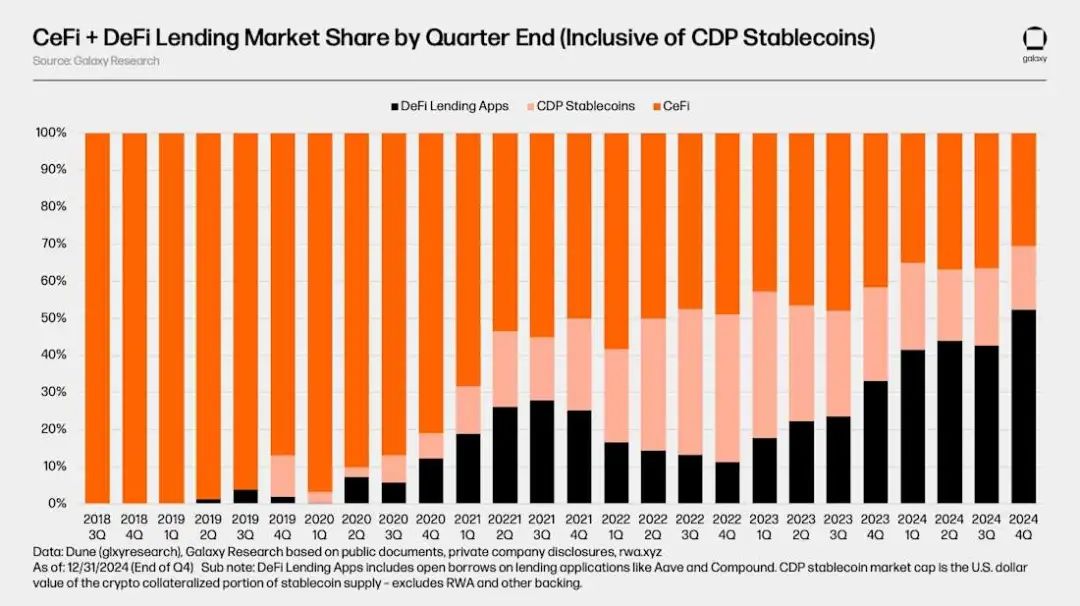

A notable change in the crypto lending market is that DeFi lending applications have shown a stronger dominance than CeFi platforms in the bear market and continue to expand during the market recovery. In the 2020-2021 bull market cycle, when excluding the market capitalization of cryptocurrency-collateralized CDP stablecoins, DeFi lending applications accounted for only 34% of total cryptocurrency borrowing; as of the fourth quarter of 2024, the market share of DeFi lending applications has risen to 63%, almost double its original share.

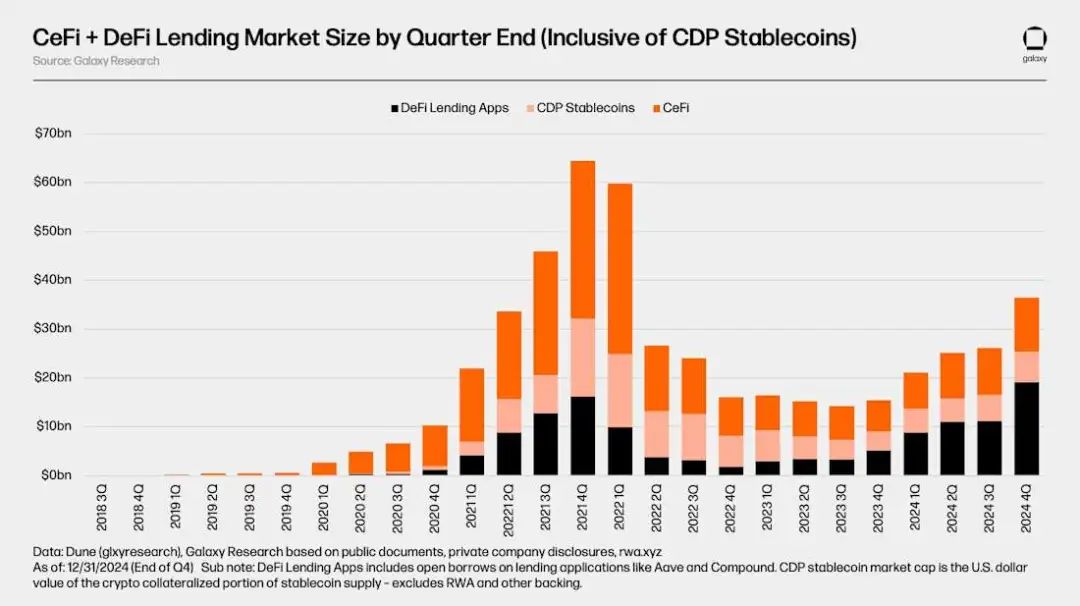

Including crypto-collateralized CDP stablecoin market capitalization, the total size of the entire crypto lending market exceeded $6.44 billion in Q4 2021. At the bottom of the bear market in Q3 2023, the market size was only $1.42 billion, down 78% from the peak of the bull market. As of Q4 2024, the market has rebounded 157% from the low point in Q3 2023, with a total size of $3.65 billion.

It is important to note that, similar to borrowing through DeFi lending applications, there may also be a double counting problem between the size of CeFi loan books and the supply of CDP stablecoins. This is because some CeFi entities rely on minting CDP stablecoins with cryptocurrency collateral to provide lending services to off-chain customers.

When including crypto-collateralized CDP stablecoins, a clear growth in the on-chain lending and borrowing market share can be observed. As of Q4 2024, DeFi lending applications and CDP stablecoins accounted for 69% of the entire market. Since Q4 2022, their share has been showing a steady growth trend. A notable phenomenon is that the dominance of CDP stablecoins as crypto-collateralized leverage is gradually declining. This can be partly attributed to the increase in stablecoin liquidity, the improvement of lending application parameters, and the introduction of neutral stablecoins such as Ethena.

6. Market Data Logic and Sources

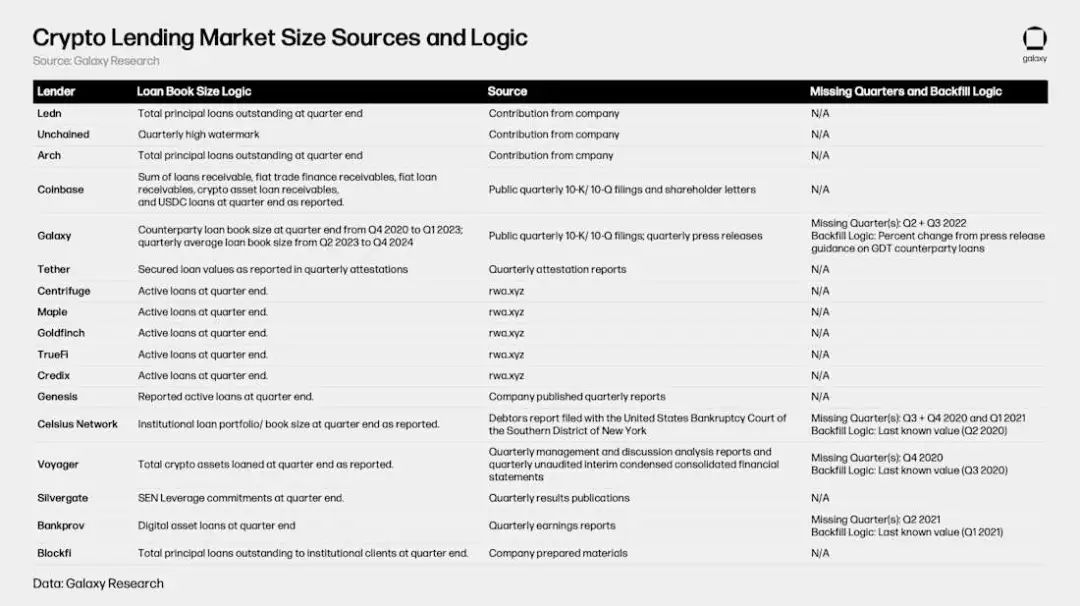

The following table shows the sources and logic used to compile the above DeFi and CeFi lending market data. While DeFi and cDeFi data can be retrieved through on-chain data, which is transparent and easy to obtain, CeFi data is more complicated to obtain and has poor availability. This is due to the inconsistency of CeFi lending platforms in recording outstanding loans, the difference in the frequency of their public information, and the general difficulty of obtaining information.

7. Venture Capital and Crypto Lending

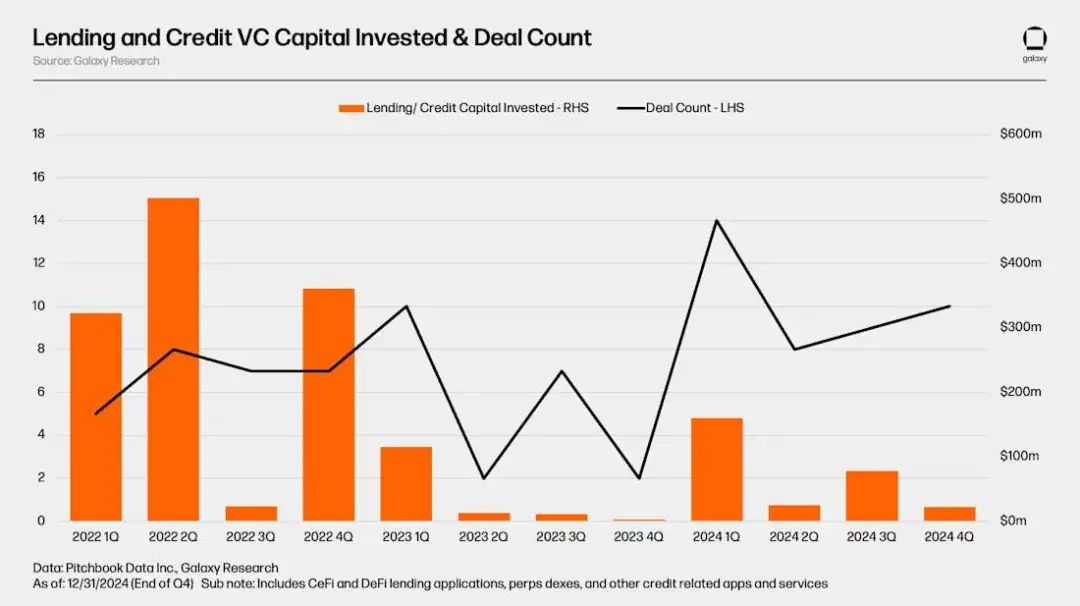

CeFi and DeFi lending/credit application platforms raised a total of $1.63 billion in 89 deals between Q1 2022 and Q4 2024. Among these deals, Q2 2022 saw the most capital raised, with eight deals raising at least $502 million. Q4 2023 was the lowest quarter, with a total of only $2.2 million raised.

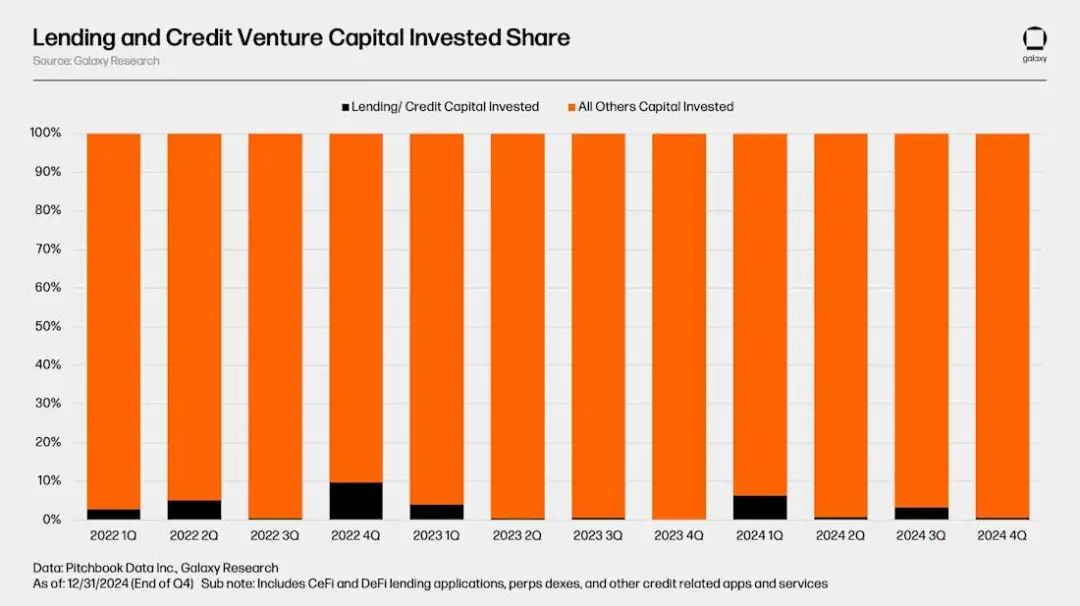

For the crypto economy, venture capital investment in lending and credit applications only accounts for a small part of total investment. From Q1 2022 to Q4 2024, lending and credit applications accounted for only 2.8% of venture capital capital per quarter on average. Lending and credit applications accounted for 9.75% of total quarterly funds in Q4 2022, the largest share; in the most recent Q4 2024, the share was only 0.62%.

8. Historical Review and Future Outlook of Crypto Lending Market

Root of the problem

The core reasons for the crypto lending market crash in 2022-2023 include:

1. Asset prices plummet:

- Excluding Bitcoin and mainstream stablecoins, the total market value of cryptocurrencies has shrunk by 77% (about US$1.3 trillion), and the Terra ecosystem (UST and LUNA) has evaporated US$57.7 billion.

- The value of collateral plummeted and liquidity dried up, leading to debt defaults.

2. Toxic Collateral:

- stETH and GBTC: Because the underlying assets cannot be redeemed, poor liquidity leads to significant discount trading (stETH discount is 6.25%, GBTC discount is 48.9%).

- Mining machine collateral: Due to the decline in Bitcoin prices and the increase in mining difficulty, the income of mining machines has dropped by 86%, and the value has shrunk by 85-91%. Some mining machines cannot be disposed of.

3. Failure of risk management:

- Liquidity mismatch: CeFi platforms lend long-term but rely on short-term funding, and are unable to cope with runs when the market crashes.

- Unsecured loans are rampant: For example, 36.6% of Celsius’ loans are unsecured, and BlockFi provides unsecured loans to FTX.

- Lack of risk control: lack of standardized risk assessment, lax loan review, and no risk limits on some platforms.

IX. Future Trends

1. Institutionalization of CeFi lending:

- Traditional financial institutions (such as Cantor Fitzgerald and banks) will enter the market and expand their services by taking advantage of low-cost funding and regulatory relaxation (such as the SEC's repeal of SAB-121).

- Bitcoin ETFs as collateral drive growth in leveraged trading.

2. The rise of private credit on the chain:

- Tokenized debt instruments increase transparency, reduce administrative costs, and attract venture capital.

- Use case expansion: on-chain collateral, CDP stablecoin minting, etc.

3. Institutionalization and innovation of DeFi:

- Institutions are accelerating their adoption of DeFi due to increased regulatory clarity and on-chain liquidity advantages.

- Centralized companies build on DeFi protocols (such as Ondo Finance forking Compound) to promote on-chain ecological integration.

10. Conclusion

Market differentiation: DeFi showed resilience in the bear market, with its share increasing from 34% to 63%, and its dominant position continued to strengthen; CeFi may recover due to the entry of institutions, but the concentration is still high (the top three platforms account for 89%).

Risks and opportunities coexist: the entry of traditional finance brings compliance and liquidity, but we need to be wary of collateral fluctuations and regulatory uncertainties.

On-chain future: Tokenization, automated risk control and institutional participation will drive crypto lending towards transparency and scale, becoming a core component of digital financial infrastructure.