Don’t Go to Fintech 2.0

Crypto is doing payment, and Fintech is doing stablecoin.

Over the past year, the development of the cryptocurrency industry has been a two-way street with traditional financial companies, Web 2.0 giants and global politicians. Trump's air coin is the end of crypto liquidity, and peace has just begun.

The consultants in Pakistan, the crypto mines in Bhutan and the sky-high financing in the Middle East eventually became the last straw that broke the camel's back for retail investors. So let's all go to the wishing well and be cuckolds, and maybe we can still get some love.

The Age of Crypto Stagnation

Human beings are very strange creatures. In the past, they pursued freedom when they were traditional, but now they pursue tradition when they are free.

The only lesson humanity has ever learned is that it can learn no lesson.

I still remember that when the Bitcoin Spot ETF was passed, everyone thought that Bitcoin would change the world. Of course, now everyone thinks that Bitcoin is just a mapped asset of M2. It itself can neither reduce inflation nor preserve or increase value. After being extracted by the ETF, it can no longer serve as a fuel for the cryptocurrency bull market engine. This one-track mindset has turned into a double-edged sword.

The only lesson humanity has learned is that it can't learn any lessons +1.

When Trump descended upon his loyal cryptocurrency circle with air coins, the silence after the surge was not surprising. PumpFun’s self-rescue, Binance Wallet’s attack, or whether Boop is Binance CXO have all become farces themselves, and none of them can make money.

Image description: Encryption current landscape Image source: @zuoyeweb3

There is nothing new under the sun, only stagnation in cryptocurrencies.

First, Ethereum, an “innovation at the level of human civilization”, could not withstand the decline from 4000 to 1500, and had to rely on Risc-V to return to the L1 battle. If EVM can be completely transformed, it might as well change PoS to PoW in one step. Can Ethereum’s bet on L1 and the newly added Risc-V really save itself?

Being commanded by the enemy is the stupidest behavior. Unfortunately, Solana is the commander this time. Solana bet on L1 before and after FTX.

In essence, SVM L2 or the extension layer is also a bloodsucking behavior for Solana. It is a carp on the whale’s body, not intentional by the whale, but ETH L2 is a barnacle on Ethereum, which was brought upon by Ethereum itself.

The market paradigm we were familiar with is gone forever. ETH is not Money, Stablecoin is Money.

Secondly, invalid information is infecting the entire market. KOL Summer will quickly turn into KOL Agency Summer, and then CEX Summer. If you don’t believe it, just look at the grand occasion of this Dubai Music Festival. Project parties, KOLs and exchanges are ultimately transaction-oriented. The exchange itself is the point of connection for trading behavior. This is an unsolvable situation.

This is not a criticism of KOL, but a recognition of market rules. From the earliest three o'clock community AMA, the community-based Bihu, to the past of the Thousand Media War, the peak of KOL's popularity is also the end point. Guiding transactions is the moment of clearing trust and influence.

However, there are also new differentiation trends in this cycle, although they are all invalid information, generally divided into two categories:

1. Garbage orders, sinking market

2. Old money stands on the platform and promotes its existence

Once again, it is the collapse and persistence of VCs. Relying on US dollar capital, VCs in Silicon Valley, the Middle East and Europe are all planning for the next stage, while the lonely Chinese VCs are constantly tortured by LPs and ROI. They have nothing to do with innovation and are rapidly becoming market makers. Since everything has to lead to transactions anyway, it is better to save steps and do it themselves.

Real innovation used to be in Huaqing Jiayuan, and will be in Shenzhen Science and Technology Park in the future. Chinese founders have to look for money in Silicon Valley and Wall Street, but projects that truly meet the next stage of the market will not be recognized by investors according to the existing framework.

The cryptocurrency world does not need FA, and Meme cannot be shorted.

The reason is simple: the transaction path is too short. The exchanges are eyeing any traffic covetously and would rather waste their time casting a wide net than miss the opportunity. The only beneficiaries have become the former big factory'ers who have escaped from the Internet to CEX. Not only ByteDance is beating, but also the troughs of cattle and horses.

In 2018, the average tenure at Toutiao was only 4 months, but by 2024, it has risen to 7-8 months at ByteDance. However, more people will still be sent out into society, and the big cryptocurrency companies only look at the top CEXs.

Today's outrageous theory: The beneficiaries of VC are students from top schools, and the beneficiaries of CEX are people eliminated by large companies. They bring not only expertise and impressive resumes, but also more hierarchical and in-depth operating standards, as well as a decline in capital efficiency due to the increase in intermediary costs.

The era and people in the cryptocurrency world, which was full of vitality, where everything was competing and people were only interested in making money, are gone forever.

Continuous institutionalization has become a shackle for the cryptocurrency world. The cryptocurrency world is more like the Internet, and the Internet is more like XXX.

Invention is the mother of necessity

I don’t FUD cryptocurrency, a more accurate mindset is “confidence in the crypto industry, but worry about my own future”. This is no longer a niche industry full of opportunities to get rich quickly, and practitioners are being replaced by the Internet and financial industries. Crypto OGs and local promoters will either go to jail, or become younger brothers, or go to jail and become younger brothers of the big guys. Baby is going to fight tigers tonight.

Complaining too much will only make you heartbroken. We should not continue discussing VC and exchanges. We should either start over like Ethereum, or explore a new ecosystem. In every crisis in the crypto industry, new ways of issuing assets are born, such as ERC-20 supporting DeFi, NFT supporting BAYC, and now we have entered the stablecoin stage.

Please note that the core of the last round of on-chain activities was Ethereum and lending, a "Lego-style" amplification of capital efficiency, while this round of Ethereum and staking models did not replicate the miracle. In our timeline, Tencent did not invent WeChat, but Xiaomi MiTalk rose.

Interest-bearing stablecoins (YBS) have become a new invention, and they will create new demands. It is not because the demand for stablecoins cannot be met and USDT is doing well, but because YBS can be done in this way, Ethena was invented, referring to the end of the US dollar seigniorage and the stablecoin super cycle.

YBS will become a new form of asset issuance. This is an expectation. Based on psychological history, I have three predictions for the future, pointing to different futures:

1. YBS becomes a new asset issuance method, and Ethereum successfully changes its “core”. ETH replaces BTC as the new encryption engine, and Restaking ETH becomes real money;

2. YBS becomes a new asset issuance method, and Ethereum goes silent. YBS will be swallowed up by US dollar assets such as government bonds, Fintech 2.0 will become a reality, and Web 3.0 will become a pipe dream;

3. YBS will not become a new asset issuance method, and Ethereum will die silently. Then the blockchain will "de-coin and store chain". Fintech 1.0 is Paypal's replacement for banks, Stripe is an electronic innovation in acquiring, and the coinless blockchain is at most Fintech 1.5.

To summarize, Fintech 2.0 is financial blockchain, and Fintech 1.5 is currency-free blockchain technology.

Stablecoins are becoming a new asset issuance model, which is something that no VC research report has ever predicted. Even Ethena itself has not thought about it this way. If we believe that the market itself is the optimal solution, the biggest problem of VCs and exchanges is not to learn from Vitalik and indulge in technical narratives, but to not respect market laws.

In the current cryptocurrency landscape, exchanges, stablecoins and public chains are actually the three dominant players. Binance, USDT and Ethereum constitute the protagonists, and the others are suppliers and distribution channels surrounding the three. Exchanges and public chains are relatively stable. Now the war is focused on stablecoins. Not only USDC, BlackRock and others are entering the market, but the answer given on the chain is YBS. It is a matter of overall concern and we have an obligation to do so.

PS, exchange stability refers to the dominance of Binance, and public chain stability refers to the revitalization of Ethereum, and Solana’s replacement is still on the way.

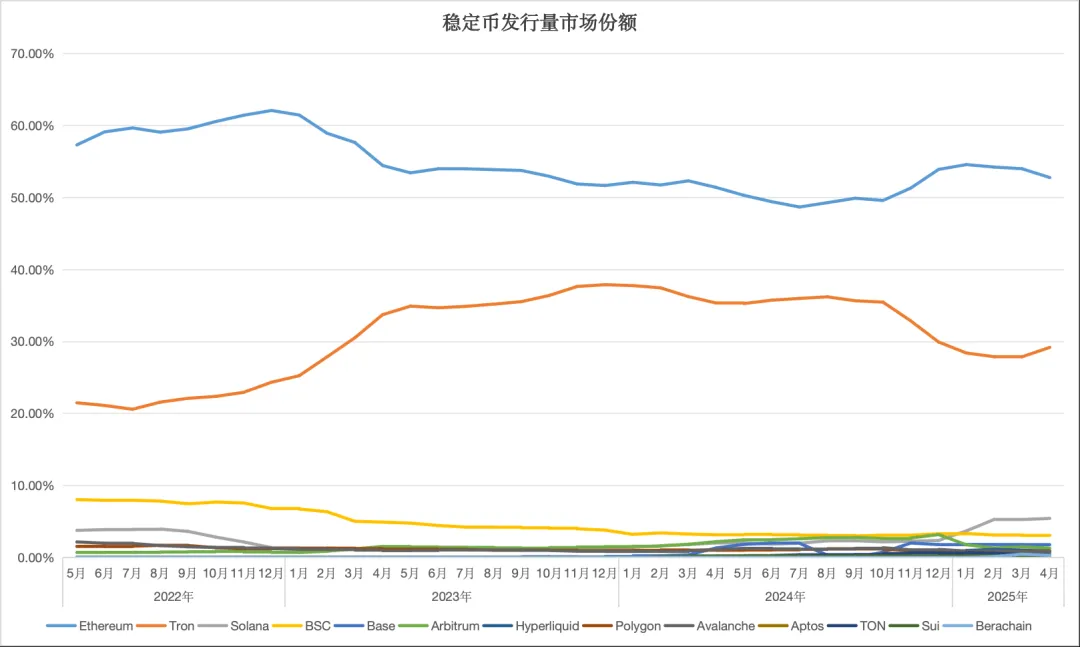

Image caption: Stablecoin market issuance Image source: @zuoyeweb3

In today’s market, Ethereum and Tron dominate the market, but Solana has not given up on catching up. In particular, Ethereum has not been completely defeated. We always hear that Solana DEX transaction volume has surpassed the Ethereum ecosystem. However, in terms of actual asset issuance, ETH+ERC-20 USDT still holds the top spot.

This is also the main reason why I think there is no problem with Ethereum's fundamentals. Everyone expects the price of ETH to be 10,000, and the expectation for SOL is 1,000. The basis points are completely different.

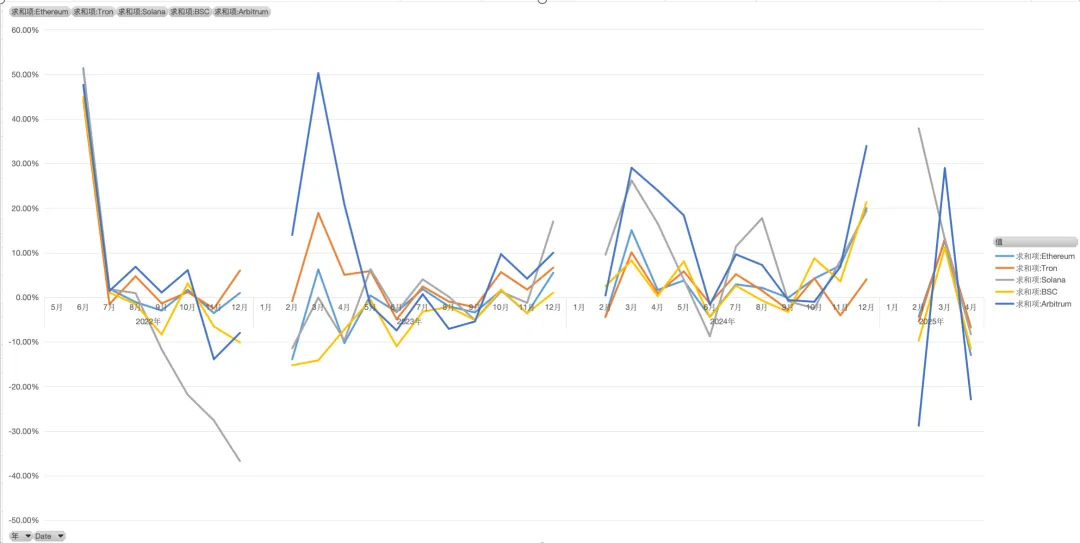

Image caption: Stablecoin growth rate Image source: @zuoyeweb3

Especially by comparing the growth rates of each chain, we can find that they are basically in the same frequency. Except for Solana which is close to death in 2022, everyone is consistent with Ethereum for the rest of the time. We can believe that in terms of correlation, the stablecoins of each chain have not developed independent trends and are still spillovers of Ethereum.

Based on this, the importance of pairing Ethereum and stablecoins is explained, and the importance of YBS lies in anchor exchange. With a stablecoin market value of 230 billion, USDe and YBS are still just others.

Again, YBS must become a new way of issuing assets in order to transfer the asset attributes of ETH to the currency level. Otherwise, the spring of RWA will be the cold winter of the cryptocurrency world.

Conclusion

Ethereum only has a technical narrative, and users only embrace stablecoins.

We hope that users will embrace YBS rather than USDT. This is the current situation and also the disagreement between us and the market.

Pursuing a niche is a very popular thing. Just look at the through-type taillights and LABUBU all over the world. Let me briefly mention blockchain payment. There is nothing wrong with payment, but before YBS supported by crypto-native assets becomes mainstream, pushing blockchain payment is "the result before the cause", that is, payment should be the direction of YBS.

Cryptocurrency should not become Fintech 2.0, the road cannot become narrower and narrower.