Since the DeFi Summer of 2020, AMMs (automated market makers), lending protocols, derivatives trading, and stablecoins have become the core infrastructure in the crypto trading field. Over the past four years, many entrepreneurs have continuously iterated and innovated on these tracks, pushing projects such as Trader Joe and GMX to new heights. However, as these products gradually mature, the growth of the crypto trading track has begun to hit the ceiling, and the birth of a new batch of top projects has become increasingly difficult.

After the 2024 US election, the legalization and compliance process of the crypto industry is expected to bring new development opportunities to the industry. The integration of traditional finance and DeFi is accelerating: private credit, US Treasury bonds, and physical assets (RWA) such as commodities have gradually evolved from simple tokenized certificates in the early days to capital-efficient income-generating stablecoins, providing new options for crypto users seeking stable returns and becoming a new growth engine for DeFi lending and trading. At the same time, the strategic position of stablecoins in international trade is becoming increasingly prominent, and the upstream and downstream infrastructure of the payment track continues to prosper. Traditional financial giants, including the Trump family, Stripe, PayPal, and BlackRock, have accelerated their layout to inject more possibilities into the industry.

After "old DeFi" such as Uniswap, Curve, dYdX and Aave, a new batch of unicorns in the field of crypto trading are brewing. They will adapt to the changes in the regulatory environment, use the integration of traditional finance and technological innovation to open up new markets and push the industry into the "new DeFi" era. For new entrants, this means that they no longer need to stick to micro-innovations in traditional DeFi, but focus on building breakthrough products that meet the new environment and needs.

This article, written by HTX Ventures, will conduct an in-depth analysis of this trend, explore the potential opportunities and development directions in the new round of changes in the crypto trading track, and provide inspiration and reference for industry participants.

Changes in the trading environment during this cycle

Stablecoins have passed compliance and their adoption in cross-border payments continues to increase

Maxine Waters and Chairman Patrick McHenry of the U.S. House Financial Services Committee plan to introduce a stablecoin bill in the short term, marking a rare bipartisan consensus on stablecoin legislation in the United States. Both parties agree that stablecoins not only consolidate the dollar's position as a global reserve currency, but have also become an important buyer of U.S. Treasury bonds and have huge economic potential. For example, Tether generated $6.3 billion in profits last year with only 125 employees, fully demonstrating its profitability.

This bill may become the first comprehensive cryptocurrency legislation passed by Congress in the United States, promoting traditional banks, businesses and individuals to widely access crypto wallets, stablecoins and blockchain-based payment channels. In the next few years, stablecoin payments are expected to become popular, becoming another "step-by-step development" in the crypto market after the Bitcoin ETF.

Although compliant institutional investors cannot directly benefit from the appreciation of stablecoins, they can profit by investing in stablecoin-related infrastructure. For example, mainstream blockchains that support a large supply of stablecoins (such as Ethereum, Solana, etc.) and various DeFi applications that interact with stablecoins will benefit from the growth of stablecoins. Currently, stablecoins account for more than 50% of blockchain transactions, up from 3% in 2020. Its core value lies in seamless cross-border payments, a feature that is growing particularly rapidly in emerging markets. In Turkey, for example, stablecoin transactions account for 3.7% of its GDP; in Argentina, the stablecoin premium is as high as 30.5%. Innovative payment platforms such as Zarpay and MentoLabs use local agents and payment systems to attract users into the blockchain ecosystem with a grassroots market strategy, further promoting the popularity of stablecoins.

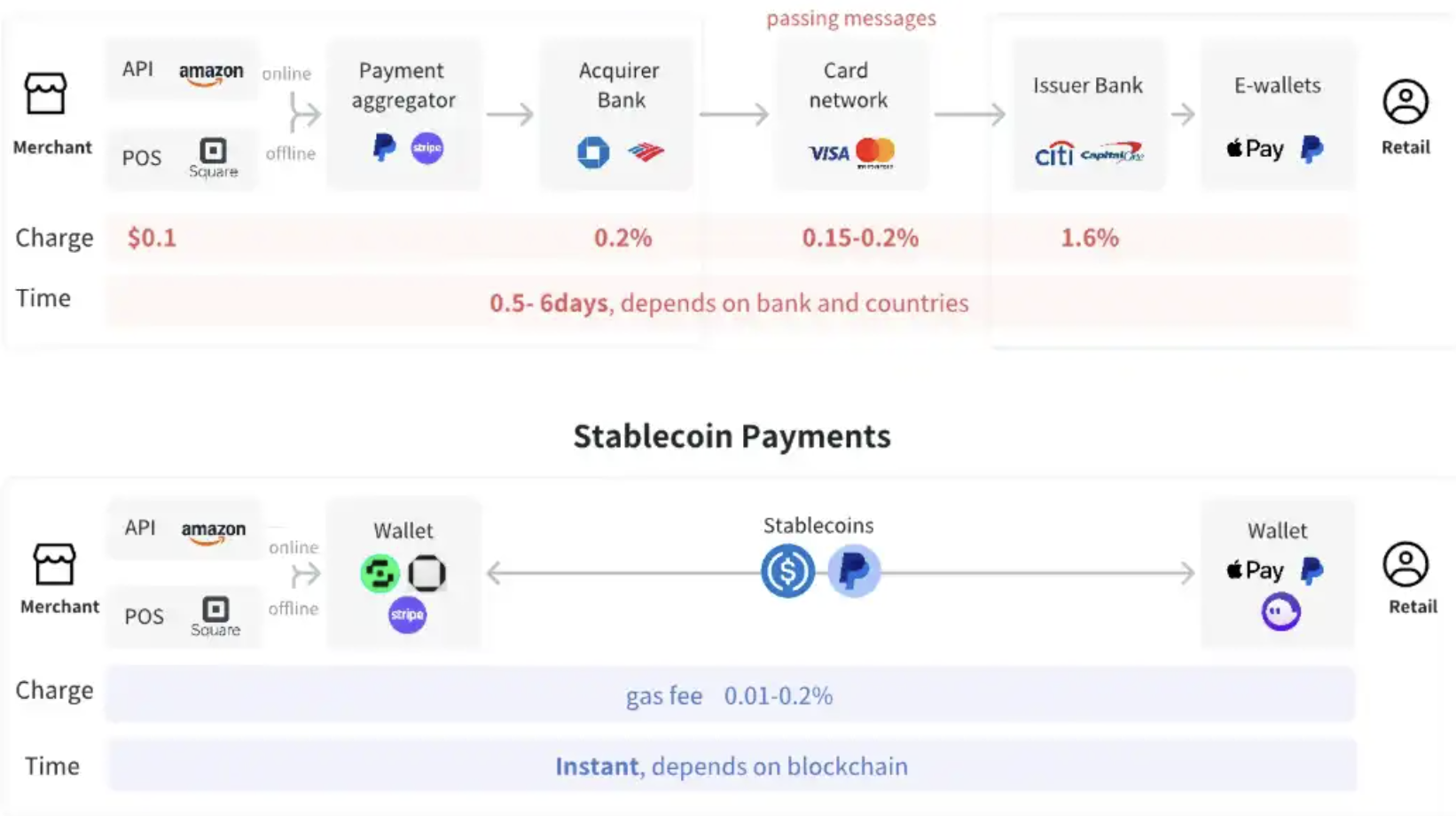

At present, the cross-border B2B payment market processed by traditional payment channels is as large as about 40 trillion US dollars, and the global consumer remittance market generates hundreds of billions of dollars in revenue each year. Stablecoins provide this market with a new means to achieve efficient cross-border payments through encrypted channels. The adoption rate is increasing rapidly, and it is expected to enter and subvert this part of the market and become an important force in the global payment landscape.

https://mirror.xyz/sevenxventures.eth/_ovqj0x0R_fVAKAKCVtYSePtKYv8YNLrDzAEwjXVRoU

The RLUSD stablecoin launched by Ripple is designed for corporate payments and aims to improve the efficiency, stability and transparency of cross-border payments to meet the needs of transactions denominated in US dollars. At the same time, Stripe acquired the stablecoin platform Bridge for US$1.1 billion, which became the largest acquisition in the history of the cryptocurrency industry. Bridge provides seamless conversion between fiat currency and stablecoins for enterprises, further promoting the application of stablecoins in global payments. Bridge's cross-border payment platform processes more than US$5 billion in annual payments and has provided global funds settlement for high-end customers including SpaceX, demonstrating the convenience and effectiveness of stablecoins in international transactions.

In addition, as an innovative stablecoin cross-border payment platform, PEXX supports the exchange of USDT and USDC into 16 legal currencies and can directly remit to bank accounts. Through a simplified onboarding process and instant conversion, PEXX enables users and businesses to make cross-border payments efficiently and at low cost, breaking down the barriers between traditional finance and cryptocurrency. This innovation not only provides a faster and more cost-effective cross-border payment solution, but also promotes the decentralization and seamless connection of global capital flows. Stablecoins are gradually becoming an important part of global payments, improving the efficiency and popularity of payment systems.

Regulation on perpetual contract trading is expected to be relaxed

Since the high leverage of perpetual contract trading can easily lead to customer losses, regulatory authorities in various countries have always had very strict compliance requirements. In many jurisdictions, including the United States, not only are centralized exchanges (CEX) prohibited from providing perpetual contract services, but decentralized perpetual contract exchanges (PerpDEX) are also unable to escape the same fate. This directly compresses the market space and user scale of PerpDEX.

However, with Trump's victory in the election, the compliance process of the crypto industry is expected to accelerate, and PerpDEX is very likely to usher in a spring of development. There are two landmark events worth noting recently: first, David Sacks, the crypto and AI consultant appointed by Trump, has invested in dYdX, a veteran player in this field; second, the U.S. Commodity Futures Trading Commission (CFTC) is expected to replace the U.S. Securities and Exchange Commission (SEC) as the main regulator of the crypto industry. The CFTC has accumulated rich experience in the launch of Bitcoin futures trading at the Chicago Mercantile Exchange (CME), and its regulatory attitude towards PerpDEX is more friendly than that of the SEC. These positive signals may open up new market opportunities for PerpDEX and create more favorable conditions for its growth under the future compliance framework.

The stable income value of RWA is being discovered by crypto users

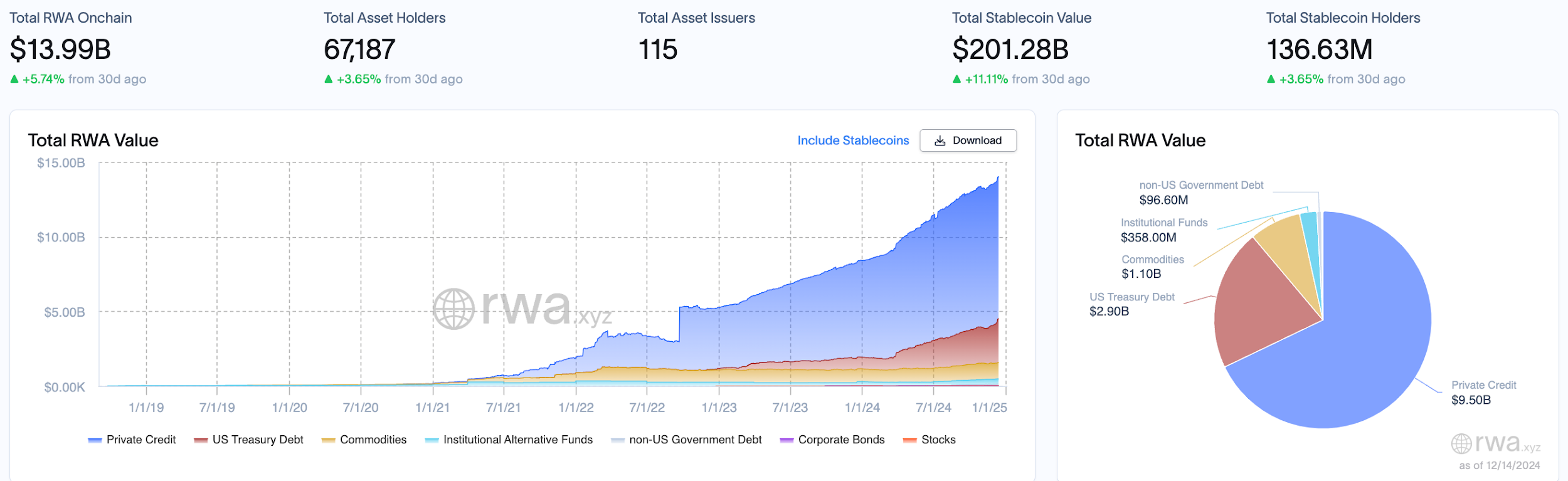

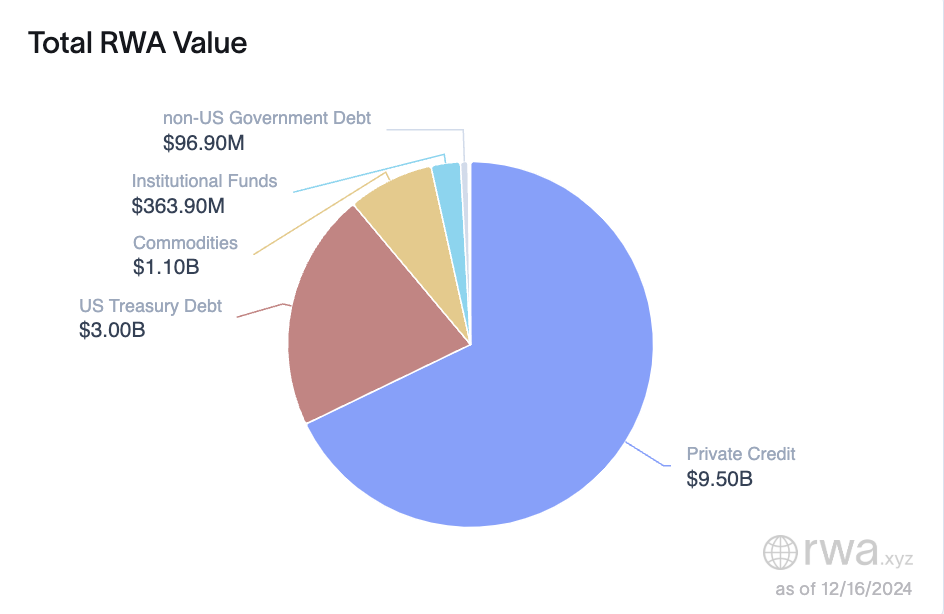

Once upon a time, the high-risk and high-return crypto market environment made the stable income of RWA (real-world assets) unpopular. However, in the past bear market cycle, the RWA market has grown against the trend, and its locked value (TVL) has jumped from less than one million US dollars to the current level of one hundred billion US dollars. Unlike other crypto assets, the value fluctuations of RWA are not affected by the sentiment of the crypto market. This feature is crucial to shaping a robust DeFi ecosystem: RWA can not only effectively improve the diversification of the investment portfolio, but also provide a solid foundation for various financial derivatives, thereby helping investors hedge risks in severe market turmoil.

According to RWA.xyz, as of December 14, RWA has 67,187 holders, 115 asset issuers, and a total market value of $139.9 billion. Web3 giants including Binance predict that the RWA market size is expected to expand to $16 trillion by 2030. This market structure with huge potential and the investment attractiveness brought by its stable returns are gradually becoming an indispensable and important part of the DeFi ecosystem.

https://app.rwa.xyz/

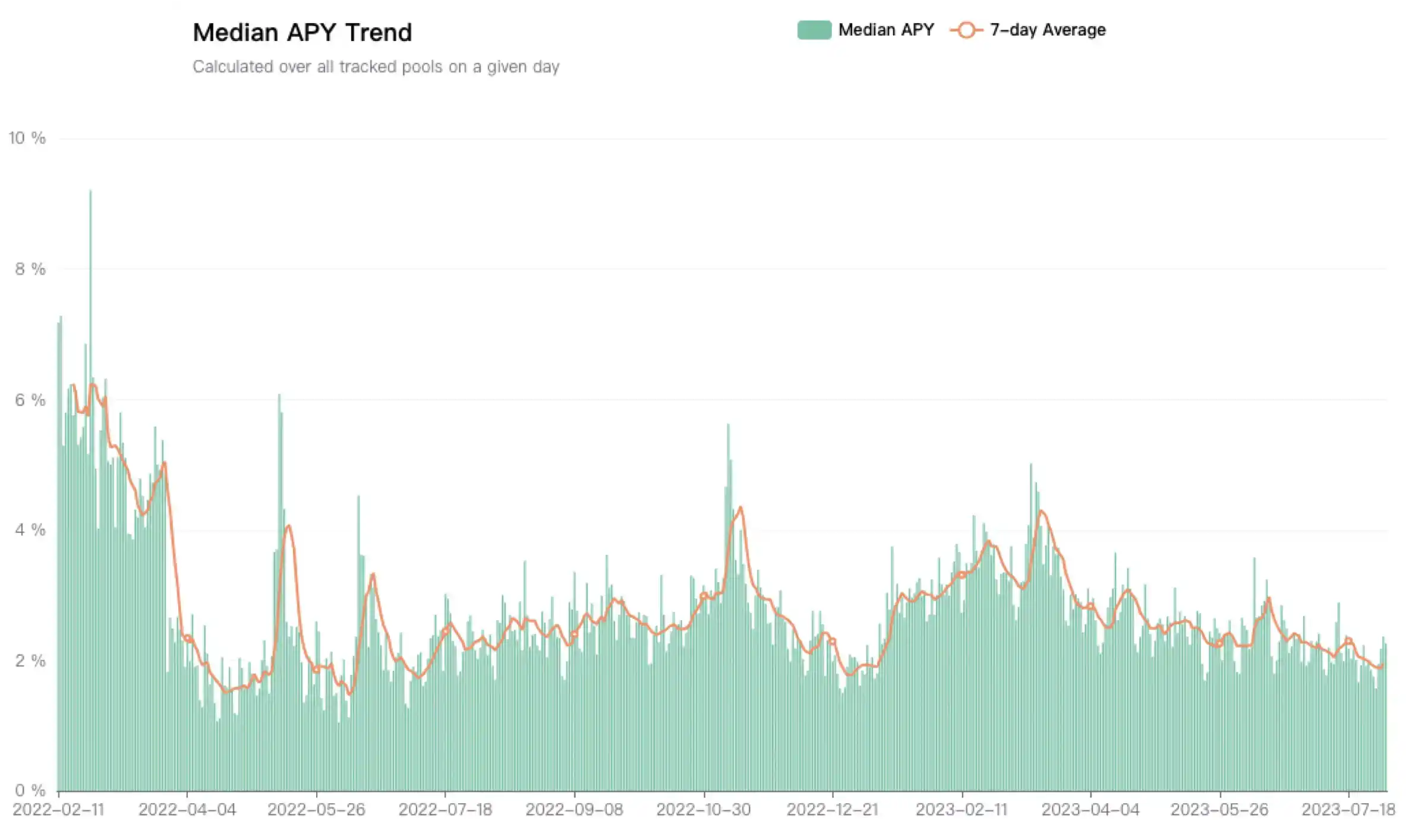

After the collapse of Three Arrows Capital, the crypto industry exposed a key problem: the lack of sustainable return scenarios for assets. As the Federal Reserve begins the process of raising interest rates, global market liquidity has tightened, and cryptocurrencies, which are defined as high-risk assets, have been particularly affected. In contrast, the yields of real-world assets (such as U.S. Treasuries) have steadily risen since the end of 2021, attracting market attention. From 2022 to 2023, the median DeFi return fell from 6% to 2%, lower than the 5% risk-free return of U.S. Treasuries during the same period, causing high-net-worth investors to lose interest in on-chain returns. With on-chain returns drying up, the industry has begun to turn to RWA, hoping to revitalize the market by introducing stable off-chain returns.

https://www.theblockbeats.info/news/54086

In August 2023, MakerDAO raised the DAI Savings Rate (DSR) to 8% in its lending protocol Spark Protocol, triggering a long-dormant DeFi market recovery. In just one week, the protocol's DSR deposits surged by nearly $1 billion, and the circulating supply of DAI also increased by $800 million, a three-month high. The key factor driving this growth is RWA (real-world assets). Data shows that more than 80% of MakerDAO's fee income in 2023 came from RWA. Since May 2023, MakerDAO has increased its investment in RWA, purchasing U.S. Treasuries in bulk through entities such as Monetalis, Clydesdale, and BlockTower, and deploying funds to RWA lending protocols such as Coinbase Prime and Centrifuge. As of July 2023, MakerDAO has an RWA portfolio of nearly $2.5 billion, of which more than $1 billion comes from U.S. Treasuries.

MakerDAO's successful exploration has triggered a new round of RWA craze. Driven by the high returns of blue-chip stablecoins, the DeFi ecosystem responded quickly. For example, the Aave community proposed to list sDAI as collateral, further expanding the application of RWA in DeFi. Similarly, in June 2023, Superstate, a new company launched by the founder of Compound, focuses on introducing real-world assets such as bonds into the blockchain, providing users with stable returns similar to the real world.

RWA has become an important bridge connecting real assets and on-chain finance. As more and more innovators explore the potential of RWA, the DeFi ecosystem has gradually found a new path to stable income and diversified development.

Licensed institutions go on-chain to expand market size

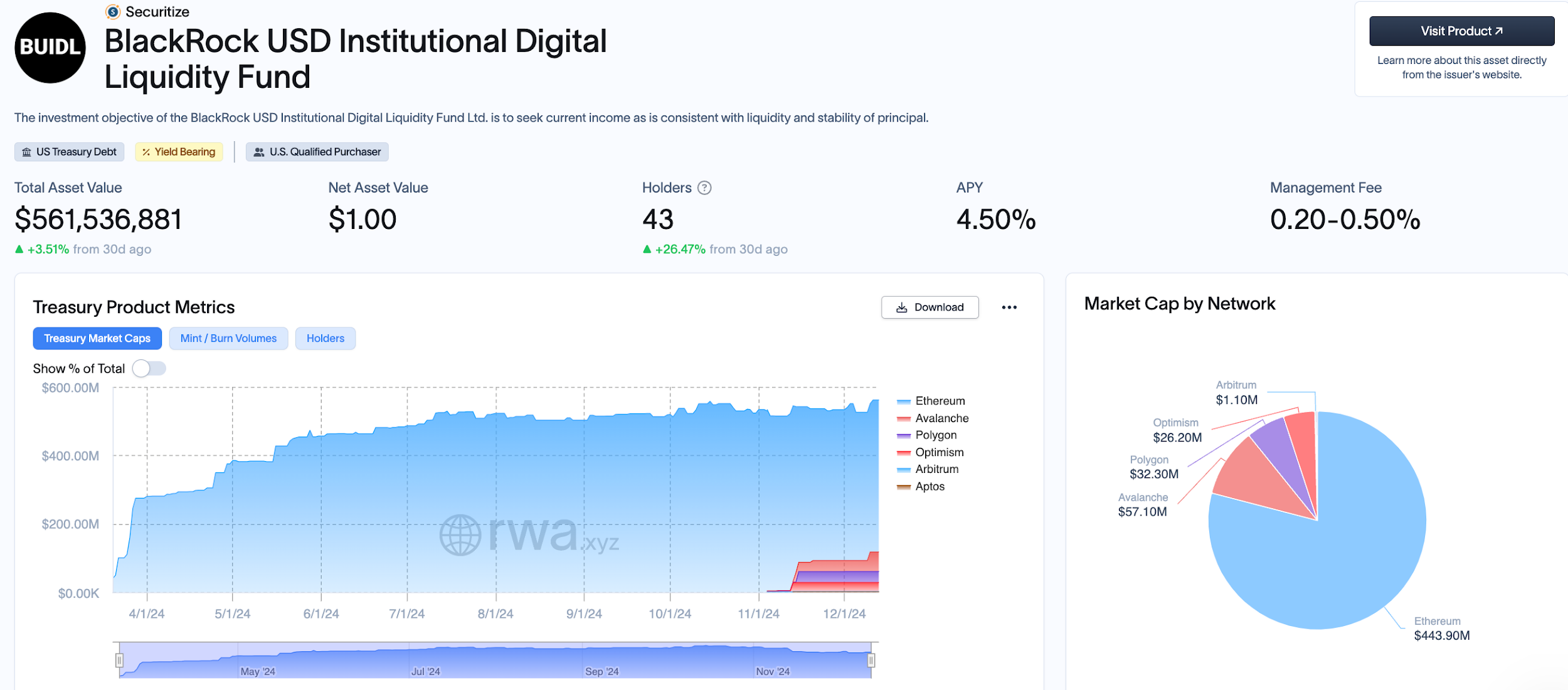

In March this year, BlackRock launched BUIDL, the first U.S. debt tokenized fund issued on a public blockchain, which attracted market attention. The fund provides qualified investors with the opportunity to earn income through U.S. debt, and was first deployed on the Ethereum blockchain, and then expanded to multiple blockchains such as Aptos, Optimism, Avalanche, Polygon and Arbitrum. At present, $BUIDL, as a token income certificate, has no practical utility, but its landmark launch is an important step for tokenized finance.

https://app.rwa.xyz/assets/BUIDL

Meanwhile, Wyoming Governor Mark Gordon announced that the state government plans to issue a stablecoin pegged to the U.S. dollar in 2025 and support it through U.S. Treasury bills and repurchase agreements. It is expected that the stablecoin will be launched in cooperation with the trading platform in the first quarter of 2025, which marks that the government-level stablecoin experiment will become a new highlight of the market.

In the traditional financial sector, State Street, as one of the world's top asset management companies, is actively exploring various ways to integrate into the blockchain payment and settlement system. In addition to considering issuing its own stablecoin, State Street also plans to launch deposit tokens to represent customer deposits on the blockchain. As the world's second largest fund custodian bank, State Street, which manages more than $4 trillion in assets, seeks to improve service efficiency through blockchain technology, marking the positive progress of traditional financial institutions in digital transformation.

JPMorgan Chase is also accelerating the expansion of its blockchain business, planning to launch on-chain foreign exchange functions in the first quarter of 2025 to achieve 24/7 automated multi-currency settlement. Since launching its blockchain payment platform in 2020, JPMorgan Chase has completed more than $1.5 trillion in transactions, covering areas such as intraday repurchases and cross-border payments. Platform users include global large companies such as Siemens, BlackRock, and Ant International. JPMorgan Chase plans to expand its platform, first supporting automated settlement of US dollars and euros, and will expand to more currencies in the future.

JPMorgan Chase's JPM Coin is an important part of the bank's blockchain strategy. As a digital dollar designed for institutional clients, JPM Coin provides instant payment and settlement on a global scale. Its launch has accelerated the process of digital assets on the blockchain for financial institutions and gained an advantage in cross-border payments and capital flows.

In addition, Tether's recently launched Hadron platform has also promoted the process of asset tokenization, aiming to simplify the conversion of digital tokens of various assets such as stocks, bonds, commodities, funds, etc. The platform provides tokenization, issuance, destruction and other services for institutions, funds, governments and private companies, and supports KYC compliance, capital market management and supervision, further promoting the digital transformation of the asset management industry.

RWA token issuance compliance tools emerge

Securitize is an innovative platform focusing on fund issuance and investment on the blockchain. Its cooperation with BlackRock began with deep cultivation in the field of RWA (real world assets), and it provides professional services to many large asset securitization companies, including the issuance, management and trading of tokenized securities. Through Securitize, companies can issue bonds, stocks and other types of securities directly on the blockchain, and use the full set of compliance tools provided by the platform to ensure that the tokenized securities issued strictly comply with the laws and regulatory requirements of various countries.

Since obtaining transfer agent registration from the U.S. Securities and Exchange Commission (SEC) in 2019, Securitize has rapidly expanded its business. In 2021, the company received $48 million in financing led by Blockchain Capital and Morgan Stanley. In September 2022, Securitize helped KKR, one of the largest investment management companies in the United States, tokenize some of its private equity funds and successfully deployed them on the Avalanche blockchain. The following year, also on Avalanche, Securitize issued equity tokens for Spanish real estate investment trust Mancipi Partners, becoming the first company to issue and trade tokenized securities under the EU's new digital asset pilot system.

Recently, Ethena, a leading stablecoin issuer, announced a partnership with Securitize to launch a new stablecoin product, USDtb. The reserve funds of this stablecoin are invested in BlackRock's US Dollar Institutional Digital Liquidity Fund (BUIDL), further consolidating Securitize's position in the blockchain financial ecosystem.

In May 2023, Securitize once again received $47 million in strategic financing led by BlackRock, which will be used to accelerate the expansion of partnerships in the financial services ecosystem. As part of this financing, Joseph Chalom, BlackRock's global head of strategic ecosystem cooperation, was appointed to the board of directors of Securitize. This cooperation marks the further deepening of Securitize's integration of traditional finance and blockchain technology.

Opportunities and challenges

Private credit RWA enters the Payfi era, how to solve the default problem

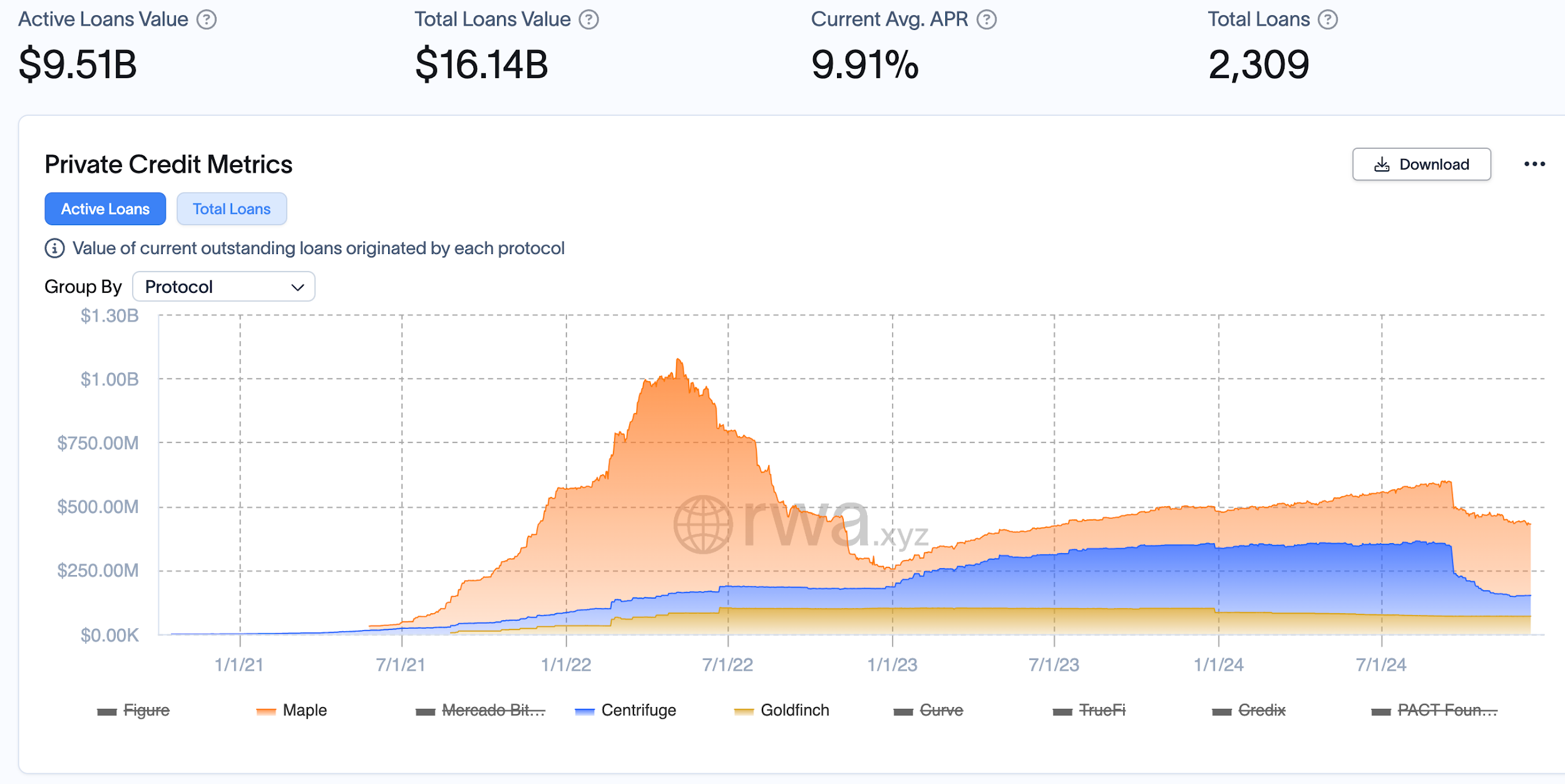

Private credit currently totals approximately $13.5 billion, with active loan value of $8.66 billion and a current average annual interest rate of 9.46%. In the RWA (real world asset) market, private credit remains the second largest asset class, with approximately 66% of issuance provided by Figure Markets.

Figure Markets is a trading platform built on the Provenance blockchain, covering a variety of asset types such as stocks, bonds and real estate. The platform received more than $60 million in Series A investment from institutions such as Jump Crypto and Pantera Capital in March this year. The current TVL (total value locked) has reached $13 billion, making it the platform with the highest TVL in the RWA market. Unlike traditional non-standard private credit RWA, Figure Markets mainly focuses on the standardized market of home loans, which gives it a larger market size and growth potential, and there will be more opportunities in the future.

https://app.rwa.xyz/?ref=ournetwork.ghost.io

In addition, private credit also includes corporate institutional loans. The projects that emerged in the last cycle mainly include Centrifuge, Maple Finance and Goldfinch.

TVL has rebounded this year https://app.rwa.xyz/?ref=ournetwork.ghost.io

- Centrifuge is a decentralized asset financing protocol that tokenizes real-world assets (such as real estate, bills, invoices, etc.) into NFTs through its Tinlake protocol and uses them as collateral for borrowers. Borrowers can obtain liquidity in decentralized pools of funds through these NFTs, and investors provide funds through these pools and receive fixed returns. Centrifuge's core innovation is to combine blockchain with traditional financial markets to help companies and startups obtain financing at a lower cost, and reduce credit risk and intermediary costs through the transparency and decentralization provided by blockchain.

However, Centrifuge also faces risks brought by market volatility. Although its asset tokenization model is favored by many traditional financial institutions, in the case of large market fluctuations, borrowers may not be able to repay on time, leading to default events. For example, some assets with large market fluctuations may not be able to fulfill loan contracts, especially in the bear market stage, when liquidity is insufficient, the borrower's debt repayment ability is greatly tested.

- Maple Finance focuses on providing high-yield secured loans to corporate and institutional borrowers. The loan pools on the platform are usually over-collateralized by crypto assets such as BTC, ETH, SOL, etc. Maple uses an on-chain credit scoring mechanism to allow institutional borrowers to provide lenders with stable returns by creating and managing loan pools. This model is particularly suitable for institutions in the crypto industry, which can reduce risks and increase capital returns by providing over-collateralized loans to these institutions.

However, the Maple platform has also faced severe challenges in the bear market. Several major defaults have occurred one after another, especially when the overall crypto market is down. For example, Orthogonal Trading failed to repay its $36 million loan on Maple Finance, which brought obvious default pressure to the platform.

- Goldfinch is a platform focused on on-chain credit lending, aiming to provide loans to startups and small and micro enterprises that cannot obtain financing through traditional channels. Unlike other RWA lending platforms, Goldfinch adopts an unsecured loan model, relying on the borrower's credit record and third-party assessment agencies to judge their repayment ability. Through the capital pool, Goldfinch lends funds to borrowers in need and provides fixed returns to fund providers.

Goldfinch's problems are mainly reflected in the selection of borrowers. Many borrowing companies face a high risk of default, especially startups and small and micro enterprises from high-risk markets. For example, in April 2022, Goldfinch suffered a $10 million loan default, with the main losses coming from high-risk small and micro enterprises and startups. Although Goldfinch received investment from a16z, these defaults still revealed its shortcomings in risk control and market demand.

https://dune.com/huma-finance/huma-overview

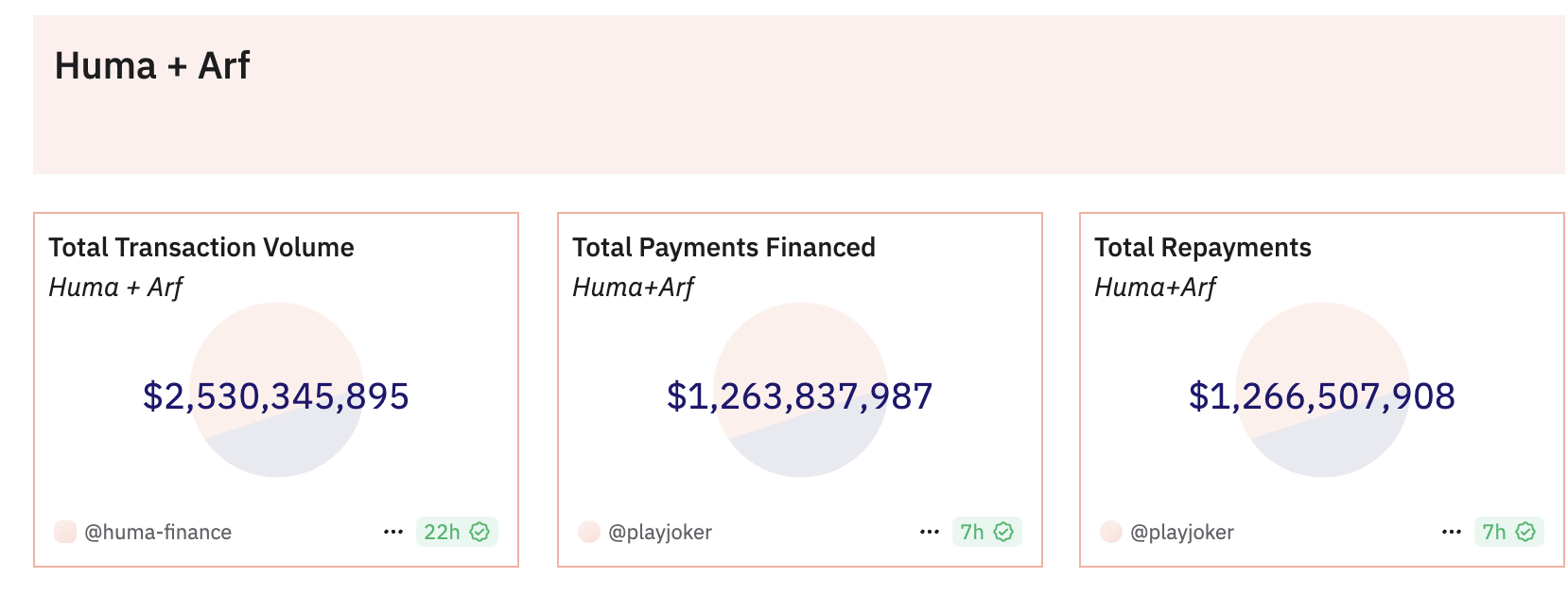

Solana's recently proposed "Payfi" concept has certain similarities in business logic with the private credit field, and further expands its application scenarios to diversified scenarios such as cross-border financing, lending, and cross-border payment swaps. Take Huma Finance as an example. The platform focuses on providing financial services to investors and borrowers. Investors earn returns by providing funds, and borrowers can borrow and repay. At the same time, Huma's subsidiary Arf focuses on cross-border payment advance services, which greatly optimizes the traditional cross-border remittance process.

For example, when sending money from Singapore or Hong Kong to South Africa, the traditional Swift remittance method is often time-consuming and costly. Although many people choose companies such as Western Union, these remittance companies need to cooperate with local partners in South Africa and rely on huge local advances to complete same-day settlement. This model has brought a huge burden to remittance companies because they need to handle advances in different fiat currencies in multiple countries around the world, and efficiency is difficult to guarantee. Arf abstracts the advance service by introducing stablecoins, providing payment companies with fast fund circulation support.

For example, when a user remits $1 million to South Africa, Arf ensures that the funds enter a regulated account and completes cross-border settlement through stablecoins. Huma conducts due diligence on payment companies before settlement to ensure security. Throughout the process, Huma lends and withdraws stablecoins without having to intervene in the deposit and withdrawal operations of fiat currencies, thus achieving fast, secure and efficient capital flow.

Huma's main customers are from developed countries such as the UK, the US, France and Singapore. The bad debt rate in these regions is extremely low, the payment period is usually 1 to 3 days, and the fee is charged on a daily basis. The capital chain is transparent and efficient. Currently, Huma has achieved a cash flow of US$2 billion, and the bad debt rate remains at 0%. Through cooperation with Arf, Huma has achieved considerable double-digit returns, which has nothing to do with tokens.

In addition, Huma plans to further connect to DeFi projects such as Pendle, explore token points reward mechanisms and broader decentralized financial gameplay to further increase user benefits and market appeal. Huma's model may become an innovative way to solve the problem of private credit defaults.

How will the leading income-generating stablecoins be allocated?

In this cycle, there is a possibility that stablecoins similar to USDT/USDC will emerge, which are safe and can provide at least 5% sustainable returns. This market undoubtedly has huge potential. At present, the annual profit of USDT issuer Tether is close to 10 billion US dollars, and its team has only about 100 people. If this part of the profit can be returned to users, can the vision of a yield-based stablecoin be realized?

The underlying gameplay of national debt

Currently, stablecoins built with government bonds as underlying assets are becoming a new trend in the crypto market. These stablecoins introduce traditional financial assets into the blockchain through tokenization, which not only retains the stability and low-risk characteristics of government bonds, but also provides the high liquidity and composability of DeFi. They use a variety of strategies to increase risk premiums, including fixed budget incentives, user fees, volatility arbitrage, and the use of reserve products such as pledge or re-pledge.

USDY launched by Ondo Finance is a typical example of this trend. USDY is a tokenized note secured by short-term U.S. Treasury bonds and bank demand deposits. Its architecture is designed in accordance with U.S. laws and regulations. It can be used as collateral in DeFi protocols and as a medium of exchange for Web3 payments. USDY is divided into two types: accumulation (USDY) and rebasing (rUSDY). The former is suitable for long-term holding, while the latter realizes returns by increasing the number of tokens and is suitable for use as a settlement tool. At the same time, the OUSG token launched by Ondo Finance focuses on providing high-liquidity investment opportunities linked to U.S. short-term Treasury bonds. Its underlying assets are deposited in the BlackRock U.S. Dollar Institutional Fund and support instant minting and redemption.

In addition, OpenTrade provides a variety of Vault products based on government bonds, including fixed-income U.S. Treasury Vault and flexible-income USDC Vault to meet the asset management needs of different users. OpenTrade deeply integrates its tokenized products with DeFi to provide holders with a seamless deposit and income experience.

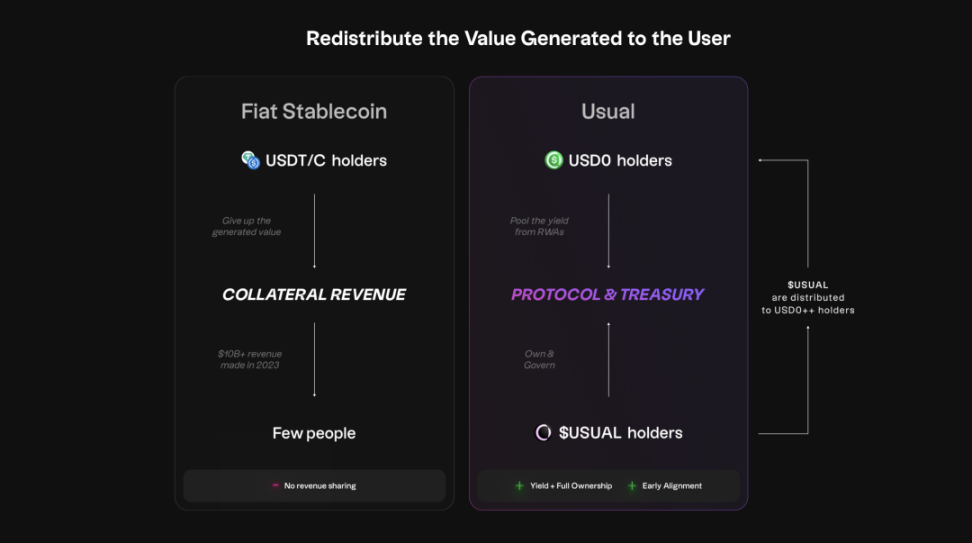

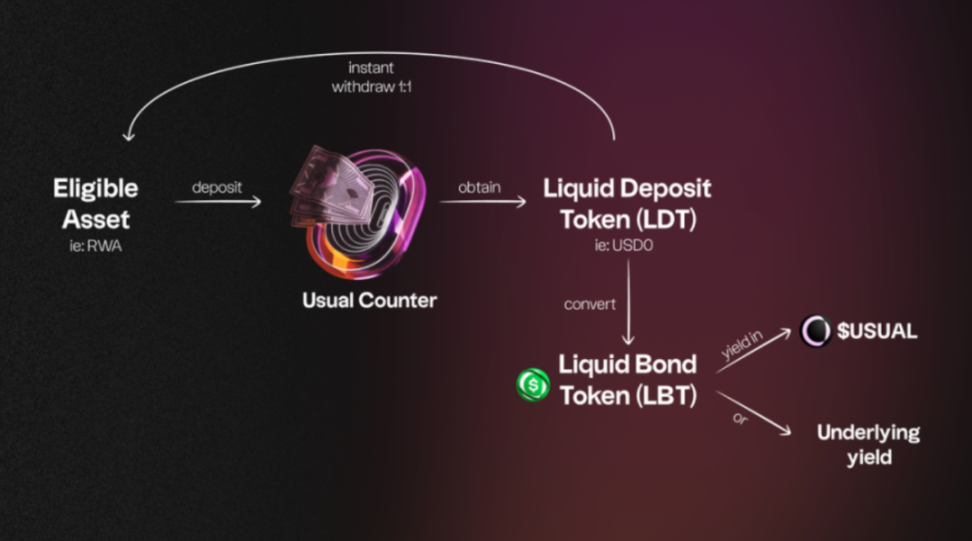

Comparison between USDT issuer revenue distribution and usual revenue distribution https://docs.usual.money/

The stablecoin USD0 launched by Usual Protocol tokenizes traditional financial assets such as U.S. Treasury bonds and provides two minting methods: users can mint USD0 by directly depositing RWA assets or indirectly by depositing USDC/USDT. They can also upgrade USD0 to the higher-yielding USD0++, and provide users with additional loyalty rewards through cooperation with DeFi platforms such as Pendle.

The sUSD stablecoin launched by Solayer on the Solana blockchain uses U.S. Treasury bonds as collateral, provides holders with a 4.33% on-chain yield, and supports it as a pledged asset to enhance the stability and security of the Solana network. Through these mechanisms, the two not only improve the profitability of stablecoins, but also enhance the stability and efficiency of the DeFi ecosystem, demonstrating the huge potential of the integration of traditional finance and blockchain technology.

Low-risk on-chain arbitrage gameplay

In addition to the design based on government bonds, another type of yield-based stablecoin uses the volatility of the crypto market, MEV and other characteristics to conduct arbitrage to obtain low-risk returns.

Ethena is the fastest growing non-currency-collateralized stablecoin project since the collapse of Terra Luna. Its native stablecoin USDe has surpassed Dai with a volume of $5.5 billion and is currently ranked third in the market. The core design of Ethena is based on the Delta Hedging strategy of Ethereum and Bitcoin collateral. By opening a short position on CEX equal to the value of the collateral, it hedges the impact of collateral price fluctuations on the value of USDe. This hedging mechanism relies on OTC clearing service providers to implement it, and the protocol assets are hosted by multiple external entities. It aims to maintain the stability of USDe through the complementary rise and fall between the value of the collateral and the short position.

The project's revenue mainly comes from three aspects: Ethereum pledge income generated by users pledging LST; funding rate or basis income generated by hedging transactions; and Liquid Stables fixed rewards, which is the deposit interest earned by depositing USDC or other stablecoins in Coinbase or other exchanges. In essence, USDe is a packaged CEX low-risk quantitative hedging strategy financial product that can provide a floating annualized rate of return of up to 27% when the market is good and liquidity is sufficient.

Ethena's risks mainly come from the potential collapse of CEX and custodians, as well as the price decoupling and systemic risks that may result from insufficient counterparties during a run. The risks are further exacerbated when interest rates may remain low during a bear market. During the market volatility period in the middle of this year, the protocol yield turned negative at -3.3%, but no systemic risk occurred.

Nevertheless, Ethena provides an innovative design logic of on-chain integration with CEX, which provides scarce short liquidity for exchanges by introducing a large amount of LST assets brought by the mainnet merger, while bringing them fee income and market vitality. In the future, with the rise of order book DEX and the maturity of chain abstraction technology, there may be an opportunity to realize a fully decentralized stablecoin based on this idea.

At the same time, other projects are also exploring different yield-generating stablecoin strategies. For example, CapLabs achieves profits by introducing MEV and arbitrage profit models, while Reservoir adopts a diversified high-yield asset basket strategy to optimize asset allocation. Recently, DWF Labs is also about to launch a yield-generating synthetic stablecoin Falcon Finance, including two versions: USDf and USDwf.

These innovations have brought diverse options to the stablecoin market and promoted the further development of DeFi.

RWA assets and DEFI applications help each other

RWA assets improve the stability of DEFI applications

The reserve funds of USDtb, the stablecoin recently issued by Ethena, are mainly invested in BlackRock's US Treasury Tokenization Fund BUIDL, of which BUIDL accounts for 90% of the total reserves, the highest BUIDL allocation among all stablecoins. This design enables USDtb to effectively support the stability of USDe in difficult market environments, especially during periods of negative funding rates. Last week, Ethena's Risk Committee approved a proposal to use USDtb as a backing asset for USDe, so that when the market is uncertain, Ethena can close USDe's underlying hedging position and reallocate the backing assets to USDtb, further mitigating market risks.

In addition, CDP stablecoins (such as collateralized debt positions) have also improved collateral and liquidation mechanisms by introducing RWA assets to improve peg stability. In the past, CDP stablecoins mainly used cryptocurrencies as collateral, but faced scalability and volatility issues. By 2024, CDP stablecoins have enhanced their risk resistance by accepting more liquid and stable collateral, such as Curve's crvUSD, which recently added USDM (physical assets). Some liquidation mechanisms have also been improved, especially crvUSD's soft liquidation mechanism, which provides a buffer for further bad debts and effectively reduces risks.

DEFI mechanism improves the utilization efficiency of RWA token assets

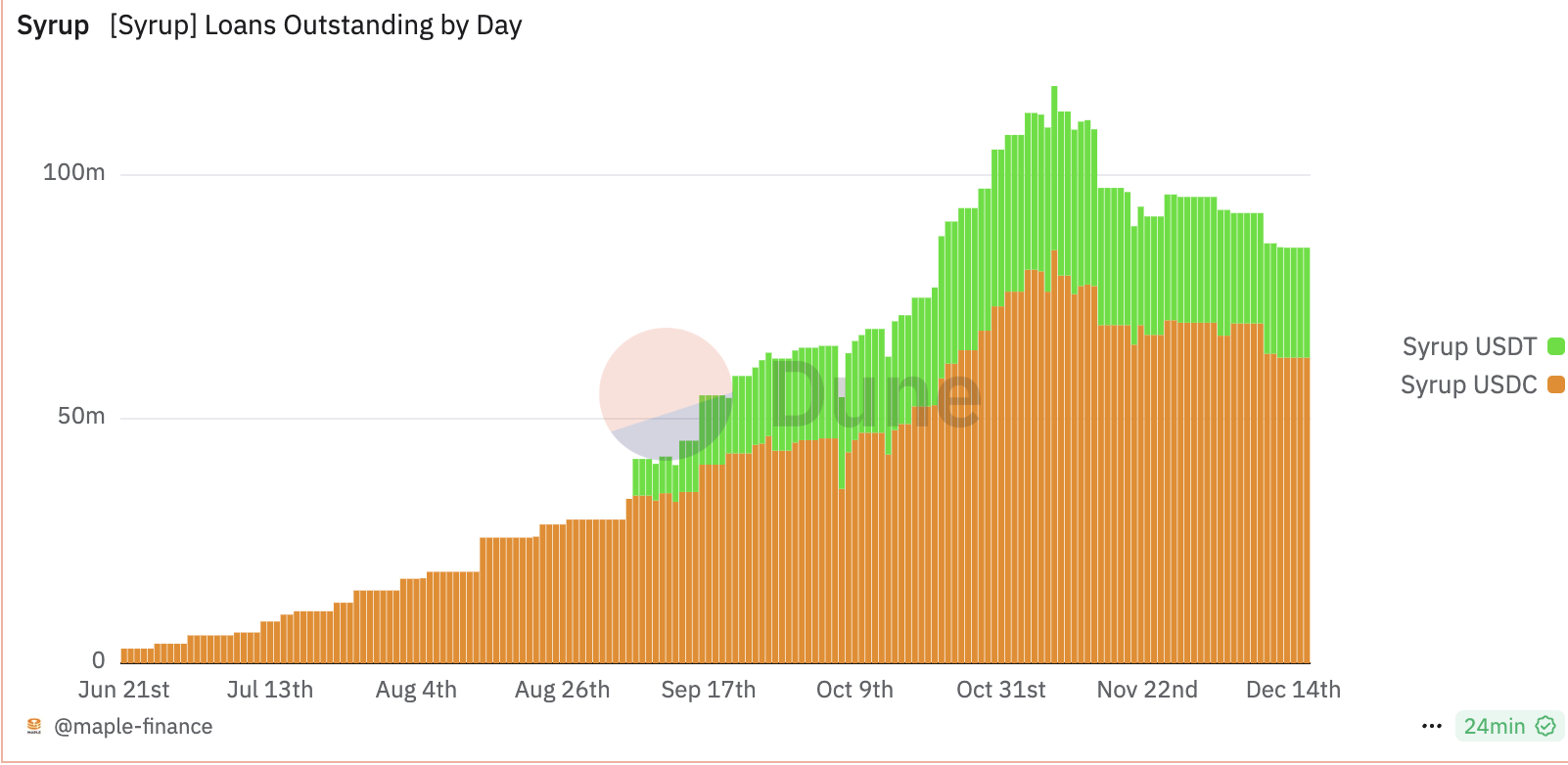

The new "RWA" partition launched by Pendle currently has a TVL of US$150 million in related assets, covering a variety of income-generating assets including USDS, sUSDS, SyrupUSDC and USD0++.

Among them, USDS is similar to DAI, and users can get SKY token rewards after depositing it into the SKY protocol; sUSDS is similar to sDAI, and part of its income comes from MakerDAO's treasury bond investment; SyrupUSDC is an income asset supported by Maple digital asset loan platform, which generates income by providing fixed interest rates and over-collateralized loans to institutional borrowers; and the income of USD0++ comes entirely from 1:1 backed treasury bonds, ensuring a stable rate of return.

Currently, the annualized rate of return provided by Pendle is quite attractive, with sUSDS LP as high as 432.4%, SyrupUSDC LP at 98.88%, USD0++ LP at 43.25%, and USDS LP at 22.96%. The high returns attract users to join in purchasing RWA stablecoins.

Syrup, a project launched by Maple in May this year, also relied on DeFi gameplay to achieve rapid growth, helping Maple to regain its life after experiencing loan defaults in the bear market.

https://dune.com/maple-finance/maple-finance

In addition, YT assets that purchase USD0++ on Pendle can also receive usual airdrops, which gives the on-chain U.S. Treasury bonds more potential profit space through token gameplay.

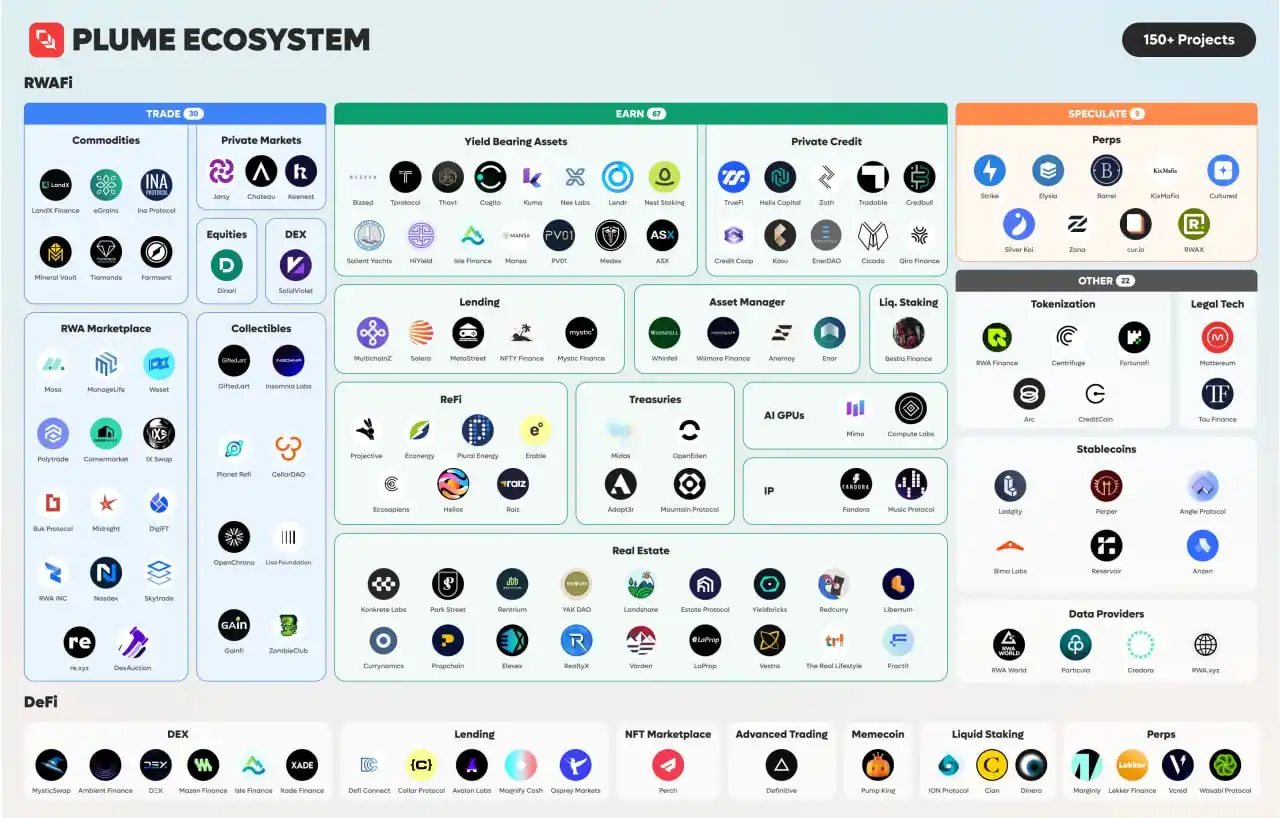

Can the RWAFI public chain empower institutional finance?

Plume is a Layer2 ecosystem focused on RWA, dedicated to integrating traditional finance (TradFi) with decentralized finance (DeFi) to build a financial ecological network covering more than 180 projects. It has established strategic alliances with WisdomTree, Arbitrum, JPMorgan Chase, a16z, Galaxy Digital and Centrifuge through the Enterprise Ethereum Alliance (EEA) and the Tokenized Asset Alliance (TAC) to promote the implementation of industry standards and institutional-level RWAfi solutions.

Plume adopts a modular, permissionless compliance architecture, allowing KYC and AML to be configured autonomously at the application level, with an embedded anti-money laundering (AML) protocol and working with blockchain analysis vendors to ensure global security compliance, while working with regulated brokers/dealers and transfer agents to ensure compliance with securities issuance and trading in markets such as the United States. The platform introduces zero-knowledge proof of reserve (ZK PoR) technology to verify asset reserves while protecting privacy, supports global securities exemption standards such as Regulation A, D and S, and serves retail and institutional investors in multiple jurisdictions.

https://www.plumenetwork.xyz/

In terms of functionality, Plume supports users:

- Borrow stablecoins or crypto assets using tokenized RWA (such as real estate, private credit) as collateral, providing low volatility collateral and security;

- Introducing liquidity staking, users can stake assets to obtain liquidity tokens to participate in other DeFi protocols and increase compound income; the platform provides compound income assets, such as private credit and infrastructure investment, to generate stable returns and help reinvest income;

- Support RWA to be listed and traded on the Perpetual DEX, allowing users to go long/short on assets such as real estate or commodities, realizing the combination of TradFi and DeFi transactions;

- In addition, Plume provides stable income assets with an annualized rate of 7-15%, covering areas such as private credit, solar energy and minerals, attracting long-term investors; in terms of speculative assets, Cultured provides on-chain speculative opportunities based on data such as sports events and economic indicators to meet users' demand for short-term high-yield transactions.

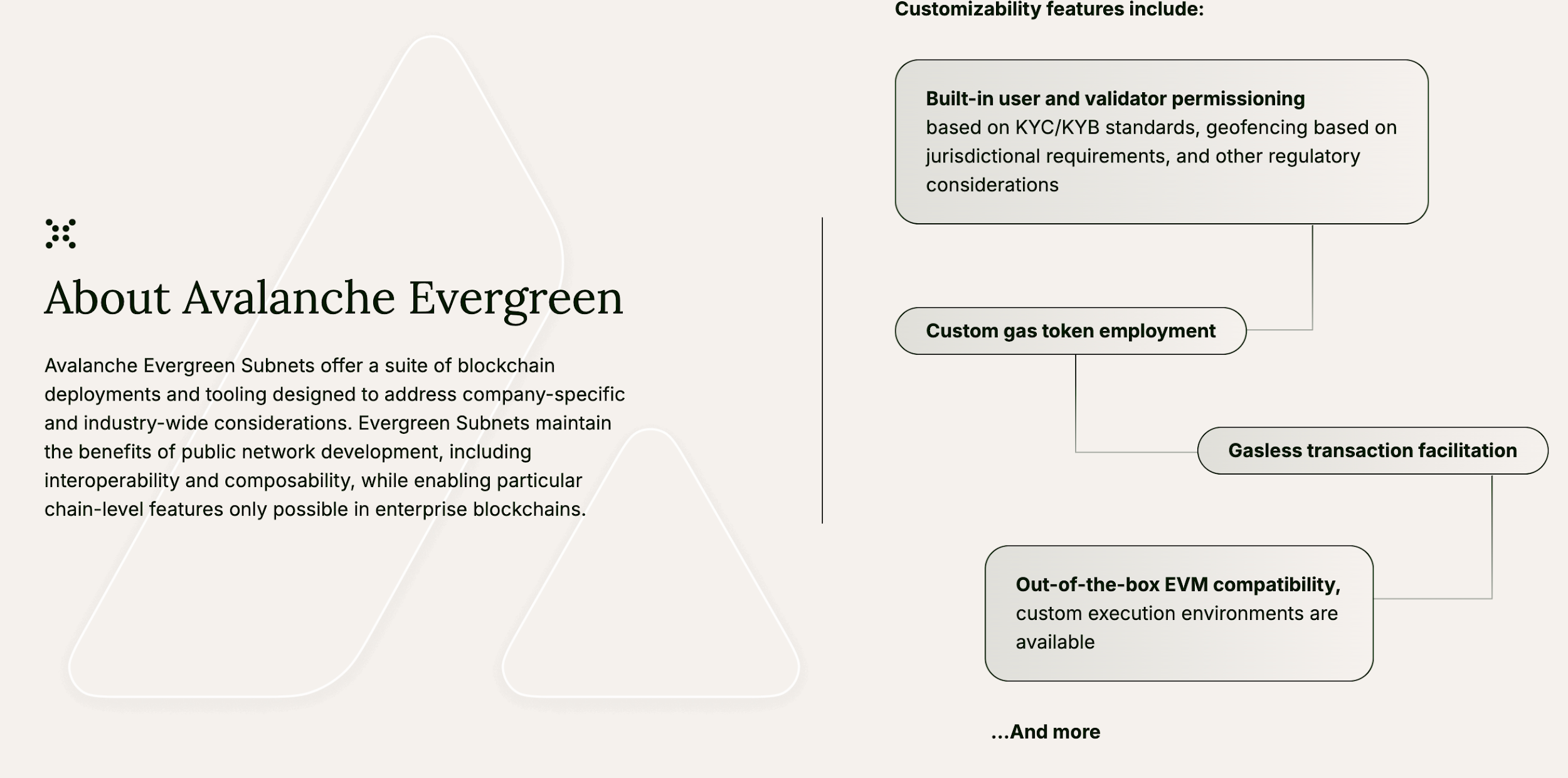

Avalanche is the first L1 public chain to fully embrace RWA. Since the end of 2022, it has been exploring enterprise-level applications at a high frequency. With its unique subnet architecture, it helps institutions deploy custom blockchains optimized for specific use cases and achieve seamless interoperability with the Avalanche network, with unlimited scalability. From the end of 2022 to the beginning of 2023, entertainment giants in South Korea, Japan, and India successively built subnets on Avalanche. Avalanche has also keenly observed Hong Kong's trends in the field of asset tokenization. In April 2023, it launched the Evergreen subnet at the Hong Kong Web3.0 Summit, providing financial institutions with specialized blockchain deployment tools and services, supporting blockchain settlement with licensed counterparties on private chains, and maintaining interoperability through the Avalanche Native Communication Protocol (AWM), attracting institutions such as WisdomTree and Cumberland to join the test network Spruce.

https://www.avax.network/evergreen

In November of the same year, Avalanche cooperated with JPMorgan Chase's Onyx platform, using LayerZero to connect Onyx and Evergreen, and promoted WisdomTree Prime to provide subscription and redemption of tokenized assets. The cooperation was included in the "Guardian Program" of the Monetary Authority of Singapore (MAS). Subsequently, Avalanche continued to expand institutional cooperation. In November, it helped the financial services company Republic launch the tokenized investment fund Republic Note. In February 2024, it conducted tokenization trials of private equity funds on the Spruce test network with Citibank, WisdomTree and other institutions. In March, it cooperated with ANZ Bank and Chainlink to connect Avalanche and Ethereum's asset settlement through CCIP, and in April, it completed integration with payment giant Stripe.

In addition, the internal foundation of the ecosystem is also actively promoting the development of RWA, launching the Avalanche Vista plan, investing $50 million to purchase tokenized assets such as bonds and real estate, and investing in RWA projects such as Balcony and Re through the Blizzard Fund. John Wu, CEO of Ava Labs, said that Avalanche's mission is to "present the world's assets on the chain", and through blockchain advantages such as instant settlement, it will bring the strong regulatory entities of traditional finance into the chain space, enabling the rise of RWA and becoming the best choice for institutions to achieve chain.

New directions worth looking forward to

On-chain foreign exchange

The traditional FX system is inefficient and faces many challenges, including counterparty settlement risk (although CLS improves security, the process is still cumbersome), high coordination costs of multiple banking systems (for example, Australian banks need to coordinate six banks to buy yen), global settlement time zone differences (for example, the Canadian dollar and Japanese yen banking systems overlap for less than 5 hours a day), and limited access to the FX market (retail users pay 100 times the fees of large institutions). On-chain FX provides instant price quotes through real-time oracles (such as Redstone and Chainlink), and achieves cost-effectiveness and transparency with the help of decentralized exchanges (DEX). For example, Uniswap's CLMM reduces transaction costs to 0.15%-0.25%, which is about 90% lower than traditional FX. On-chain instant settlement (replacing traditional T+2 settlement) also provides arbitrageurs with more opportunities to correct market pricing errors. In addition, on-chain FX simplifies corporate financial management, allowing them to access multiple products without multiple currency-specific bank accounts; retail users can get the best exchange rate through wallets embedded with DEX APIs. In addition, on-chain foreign exchange achieves the separation of currency and jurisdiction, getting rid of dependence on domestic banks. Although this approach has pros and cons, it effectively utilizes digital efficiency and maintains monetary sovereignty.

However, on-chain foreign exchange still faces challenges such as scarcity of non-US dollar-denominated digital assets, oracle security, long-tail currency support, regulatory issues, and unified interfaces for on-chain and off-chain transactions. Despite this, its potential is huge, and Citibank is developing a blockchain-based foreign exchange solution under the guidance of the Monetary Authority of Singapore (MAS). The foreign exchange market has a daily trading volume of more than US$7.5 trillion, especially in the global south, where individuals often exchange dollars on the black market to obtain a more favorable exchange rate. Although Binance P2P provides options, due to the lack of flexibility of the order book model, projects such as ViFi are developing on-chain automated market making (AMM) foreign exchange solutions, bringing new possibilities to the on-chain foreign exchange market.

Cross-border payments stack

Cryptocurrencies have long been seen as a key tool to solve the trillion-dollar cross-border payment market, especially in the global remittance market, which generates hundreds of billions of dollars in revenue each year. Stablecoins now provide a new path for cross-border payments, mainly including three layers: merchant layer, stablecoin integration and foreign exchange liquidity. At the merchant layer, through applications and interfaces that initiate retail or commercial transactions, merchants can establish stablecoin flows and form a moat, thereby upselling other services, controlling the user experience and achieving end-to-end customer coverage, similar to Robinhood in the stablecoin field. The stablecoin integration layer provides entry and exit channels, virtual accounts, cross-border stablecoin transfers, and stablecoin and fiat currency conversions. Licenses will become core competitiveness, ensuring the lowest cost and maximum global coverage. For example, Stripe's acquisition of Bridge shows how this moat is built. The foreign exchange and liquidity layer is responsible for the efficient conversion of stablecoins with US dollars, fiat currencies or regional stablecoins. In addition, as crypto exchanges continue to emerge to cater to local participants, cross-border stablecoin payment applications and processors for specific markets will gradually emerge.

Similar to traditional finance and payment systems, building defensible and scalable moats is key to maximizing business opportunities at all levels. Over time, the layers of the stack will gradually integrate, and the merchant layer has the greatest aggregation potential, which can package other layers and provide them to users, further enhance value, increase profit sources, and control foreign exchange transactions, entry and exit channel selection, and stablecoin issuer cooperation, thereby building a comprehensive and efficient cross-border payment solution.

Stablecoin aggregation platform with multi-pool model

In a world where most companies issue their own stablecoins, the fragmentation of stablecoin funding is a growing problem. While traditional on- and off-chain solutions provide short-term relief, they fail to deliver the efficiency promised by cryptocurrencies. To address this, Numéraire on Solana introduces USD*, providing the Solana ecosystem with an efficient, flexible, multi-asset stablecoin exchange platform specifically designed to address the challenge of stablecoin fragmentation.

The platform achieves seamless creation and exchange between different stablecoins through the AMM mechanism. All stablecoins share the same liquidity pool, avoiding the dispersion of funds, thereby significantly improving capital efficiency and liquidity management. As the core element of the system, USD acts as an intermediate unit, simplifies the exchange process between stablecoins, promotes more accurate price discovery, and reflects the market's valuation of various stablecoins in real time. Users can not only mint stablecoins through the protocol, but also customize risk-return configurations using the layered collateralized debt position system to further improve capital utilization. At the same time, the lending function enables excess stablecoins to be efficiently recycled within the system, optimizing capital operations.

Although Numéraire still lags behind platforms such as Raydium in terms of liquidity, its innovative design addresses the fragmentation problem of the stablecoin ecosystem and proposes a more forward-looking solution that can more effectively meet institutional needs and the actual demand for stablecoin liquidity in the real world.

Looking back at the last market cycle, the stablecoin product using the multi-pool model was only successfully implemented on Curve on Ethereum, and this model was widely praised for its high efficiency in stablecoin exchange. Looking forward, as the issuance scale of stablecoins on other public chains continues to expand, similar multi-pool model products are expected to gradually appear in more blockchain ecosystems, further promoting the scale and maturity of the stablecoin market.

References:

https://foresightnews.pro/article/detail/73859

https://app.rwa.xyz/?ref=ournetwork.ghost.io

https://docs.usual.money/

https://www.plumenetwork.xyz/

https://mirror.xyz/sevenxventures.eth/_ovqj0x0R_fVAKAKCVtYSePtKYv8YNLrDzAEwjXVRoU

https://www.theblockbeats.info/news/54086

https://cryptoslate.com/the-8-next-big-trends-in-defi/

https://medium.com/ybbcapital/the-strategic-battleground-stablecoins-ab516ee66f66

About HTX Ventures

HTX Ventures is the global investment arm of Huobi HTX, integrating investment, incubation and research to identify the best and brightest teams in the world. As an industry pioneer, HTX Ventures has more than a decade of history and excels at identifying cutting-edge technologies and emerging business models in the field. In order to drive growth within the blockchain ecosystem, we provide comprehensive support to projects, including financing, resources and strategic advice.

HTX Ventures currently supports more than 300 projects covering multiple blockchain fields, and some high-quality projects have been traded on Huobi HTX Exchange. In addition, as one of the most active FOF funds, HTX Ventures has invested in 30 top funds in the world, and cooperated with top global blockchain funds such as Polychain, Dragonfly, Bankless, Gitcoin, Figment, Nomad, Animoca and Hack VC to jointly build a blockchain ecosystem.

Website: https://www.htx.com/ventures

Twitter: https://x.com/Ventures_HTX

Medium: https://htxventures.medium.com/