No.: PandaLY Hotspot Insights Broadcast No.017

As the digital economy develops at a high speed, the crypto asset market is facing unprecedented risks and challenges - on one side, there is the cloak of compliance and regulation, while on the other side, there is severe manipulation and information asymmetry.

At 4 a.m. on April 14, 2025, the cryptocurrency market caused an uproar again. The MANTRA (OM) token, once known as the "RWA compliance vane", was forced to close positions on multiple centralized exchanges (CEX) at the same time. The price plummeted from $6 to $0.5, a single-day drop of more than 90%. The market value evaporated by $5.5 billion, and the contract players lost $58 million. On the surface, it looks like a liquidity storm, but in fact it is a premeditated highly controlled and cross-platform "harvesting game". We will deeply analyze the causes of this flash crash, reveal the truth behind it, and explore the future development direction of the Web3 industry and how to avoid similar incidents from happening again.

1| Comparison between OM flash crash and LUNA crash

The OM flash crash has similarities to the LUNA crash in the Terra ecosystem in 2022, but the causes are different:

LUNA collapse: Mainly caused by the de-anchoring of the stablecoin UST. The algorithmic stablecoin mechanism relies on the LUNA supply balance. When UST deviates from the 1:1 US dollar anchor, the system enters a "death spiral" and LUNA falls from more than US$100 to nearly US$0. This is a systemic design flaw.

OM flash crash: The investigation showed that the incident was a market manipulation and liquidity issue involving forced liquidation of CEX and high-control behavior of the team, rather than a token design defect.

Both caused market panic, but LUNA was an ecosystem collapse, while OM was more like an imbalance in market dynamics.

2. Control structure - 90% of the team and the dealer secretly control

》Ultra-high centralized control architecture

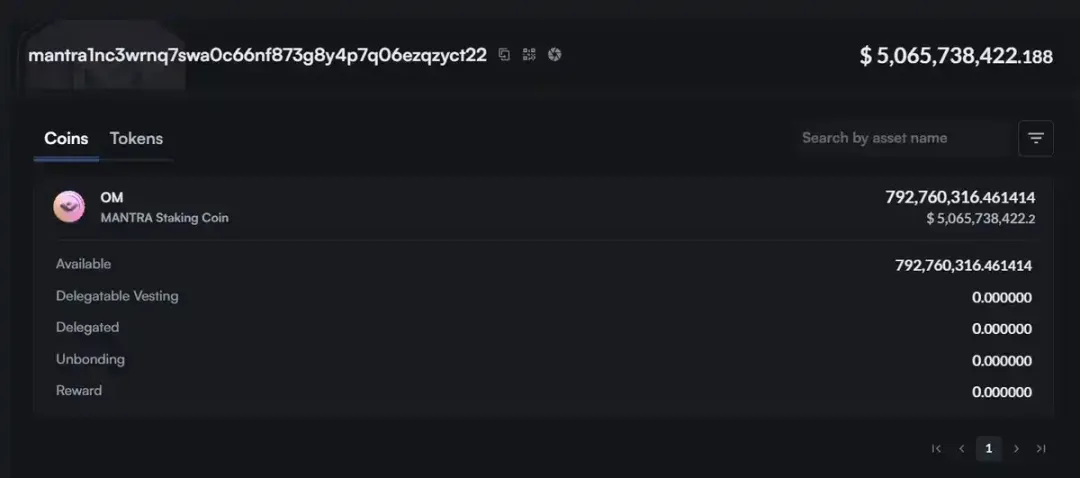

According to on-chain monitoring , the MANTRA team and its associated addresses hold a total of 792 million OMs, accounting for about 90% of the total supply, while the actual number of tokens in circulation is less than 88 million, accounting for only about 2%. Such an astonishing concentration of holdings has caused a serious imbalance in the trading volume and liquidity in the market, and large investors can easily influence price fluctuations during periods of low liquidity.

》Phase-based airdrop and lock-up strategy — creating false hype

The MANTRA project adopts a multi-round unlocking solution, which continuously extends the redemption cycle and settles the community traffic into a long-term lock-up tool.

20% will be released when it is first launched to quickly spread market awareness;

The first month was a cliff-like unlocking, followed by a linear release over the next 11 months , creating the illusion of an initial boom;

The partial unlocking ratio is as low as 10%, and the remaining tokens will be gradually vested within three years to reduce the initial circulation.

This strategy appears to be a scientific allocation on the surface, but in reality it uses high commitments to attract investors. When user sentiment rebounds, the project party introduces a governance voting mechanism to shift responsibility in the form of "community consensus." However, in actual operations, voting rights are concentrated in the hands of the project team or related parties. As a result, the results are highly controllable, creating a false trading boom and price support.

》 OTC discount trading and arbitrage

Selling at a 50% discount : Many reports in the community pointed out that OM was sold at a 50% discount on a large scale off-market, attracting private equity and large investors to take over.

Off-chain-on-chain linkage : Arbitrageurs purchase OM at low prices off-chain and transfer OM to CEX, creating on-chain trading heat and volume, attracting more retail investors to follow up. This double cycle of "cutting leeks off-chain and creating momentum on-chain" further amplifies price fluctuations.

III|The historical issues of MANTRA

MANTRA’s flash crash also caused hidden dangers due to its historical problems:

Hype of the "Compliant RWA" label: The MANTRA project gained market trust with its "Compliant RWA" endorsement. It signed a $1 billion tokenization agreement with UAE real estate giant Damac and obtained the VARA VASP license, attracting a large number of institutions and retail investors. However, the compliance license did not bring real market liquidity and decentralized holdings, but instead became a cover for the team to control the market. With the help of the Middle East compliance license to attract money, the regulatory endorsement has become a marketing tool.

OTC sales model: According to reports, MANTRA has raised more than $500 million through the OTC sales model in the past two years. The way it works is to absorb the selling pressure of the previous round of investors by continuously issuing new tokens, forming a cycle of "new for old, old for new". This model relies on continuous liquidity, and once the market cannot absorb the unlocked tokens, it may cause the system to collapse.

Legal disputes: In 2024, the Hong Kong High Court handled the MANTRA DAO case involving allegations of asset misappropriation. The court required six members to disclose financial information, and its governance and transparency itself had problems.

4. A deeper analysis of the causes of flash crashes

1) Failure of liquidation mechanism and risk model

Risk parameters fragmentation across multiple platforms:

The risk control parameters (leverage limit, maintenance margin rate, and automatic liquidation trigger point) of OMs on various CEXs are not unified, resulting in the same position facing completely different liquidation thresholds on different platforms. When a platform triggers auto-deleveraging (ADL) during a low liquidity period, the sell orders spill over to other platforms, causing "cascading liquidations."

Tail risk blind spot of risk model:

Most CEXs use the VAR (Value at Risk) model based on historical volatility, which underestimates extreme market conditions (tail events) and fails to simulate "gap" or "liquidity exhaustion" scenarios. Once the market depth drops sharply, the VAR model becomes invalid, and the triggered risk control orders actually increase liquidity pressure.

2) On-chain capital flows and market maker behavior

Large hot wallet transfers and market maker withdrawals:

FalconX hot wallet transferred 33 million OM (≈20.73 million USD) to multiple CEXs within 6 hours, which was suspected to be caused by the liquidation of positions by market makers or hedge funds. Market makers usually hold a net neutral position in high-frequency strategies, but under the expectation of extreme volatility, in order to avoid market risks, they often choose to withdraw the two-way liquidity they provide, resulting in a rapid expansion of the bid-ask spread.

The amplification effect of algorithmic trading:

When a quantitative market maker's automatic strategy detected that the OM price fell below the key support (5% below the 10-day moving average), it activated the "flash selling" module, arbitrage between index contracts and spot products, further exacerbating the spot selling pressure and the surge in funding rates for perpetual contracts, forming a vicious cycle of "funding rate-price difference-liquidation".

3) Information asymmetry and lack of early warning mechanism

On-chain warnings and community responses lag behind:

Although there are mature on-chain monitoring tools (Arkham, Nansen) that can provide real-time warnings for large transfers, the project owner and major CEXs have not established a closed loop of "warning-risk control-community", resulting in the failure to convert on-chain capital flow signals into risk control actions or community announcements.

The herd effect from the perspective of investor behavior:

In the absence of authoritative information sources, retail investors and small and medium-sized institutions rely on social media and market push notifications. When prices fall rapidly, panic liquidation and "bottom fishing" are intertwined, which amplifies trading volume (trading volume in 24 hours increased by 312% month-on-month) and volatility (30-minute historical volatility once exceeded 200%) in the short term.

5| Industry reflection and systematic countermeasures and suggestions

In order to deal with such incidents and prevent similar risks from recurring in the future, we put forward the following countermeasures and suggestions for reference only:

1. Unified and dynamic risk control framework

Industry standardization: For example, the development of a cross-exchange liquidation protocol (CELP), including: interoperability of liquidation thresholds, real-time sharing of key parameters (maintenance margin ratio, ADL trigger line) and snapshots of large positions across platforms; dynamic risk control buffer, starting the "buffer period" (liquidation grace period, T+δ) after liquidation is triggered, allowing other platforms to provide limit buy orders or algorithmic market makers to participate in the buffer to avoid instantaneous large-scale selling pressure.

Strengthening the tail risk model: Introduce stress testing and extreme scenario analysis, implant "liquidity shock" and "cross-product squeeze" simulation modules in the risk control system, and conduct regular systematic drills.

2. Decentralization and insurance mechanism innovation

Decentralized Liquidation Chain

The clearing system based on smart contracts puts the clearing logic and risk control parameters on the chain, and all clearing transactions are open and auditable. The cross-chain bridge and the oracle (Chainlink) are used to synchronize prices on multiple platforms. Once the price falls below the threshold, the community nodes (liquidators) will bid to complete the clearing, and the income and fines will be automatically allocated to the insurance pool.

Flash Crash Insurance

Launch an option-based flash crash insurance product: When the OM price drops by more than a set threshold (such as 50%) within a specified time window, the insurance contract automatically compensates the holder for part of the loss. The insurance premium rate is dynamically adjusted based on historical fluctuations and on-chain fund concentration.

3. On-chain transparency and early warning ecosystem construction

Large investor behavior prediction engine

Project owners should cooperate with data analysis platforms such as Nansen and Dune to develop an "Address Risk Score" (ARS) model to score potential large transfer addresses. Once a large transfer occurs to an address with a high ARS, it will automatically trigger a warning from the platform and the community.

Community Risk Committee

It is composed of project parties, core consultants, major market makers and representative users. It is responsible for reviewing major on-chain events and platform risk control decisions, and issuing risk notices or suggesting risk control adjustments when necessary.

4. Investor education and market resilience enhancement

Extreme market simulation platform

Develop a simulated trading environment to allow users to practice stop-loss, position reduction, hedging and other strategies in simulated extreme market conditions to enhance risk awareness and response capabilities.

Tiered leverage products

In response to different risk preferences, we launched leveled leverage products: low-risk levels (leverage ≤ 2×) use the traditional liquidation model; high-risk levels (leverage ≥ 5×) require additional payment of "tail risk margin" and participation in the flash crash insurance pool.

VI. Conclusion

The flash crash of MANTRA (OM) is not only a major shock in the cryptocurrency field, but also a severe test for the overall risk management and mechanism design of the industry. As we have discussed in detail in the article, the extreme concentration of holdings, the market operation of false prosperity, and the lack of cross-platform risk control linkage have jointly created this "harvest game".

Only through cross-platform standardized risk control, decentralized clearing and insurance innovation, on-chain transparent early warning ecosystem construction, and extreme market education for investors can we fundamentally enhance the shock resistance of the Web3 market, prevent similar "flash crashes" from happening again in the future, and build a more stable and trustworthy ecosystem.