What came after the war was not peace, but a long period of reckoning.

October 11th was a comprehensive disaster that had all the elements of previous currency disasters, including the depletion of FTX's liquidity, the policy crisis of the September 4th incident, the depegging of UST's stablecoin, and the "pulling the plug" deleveraging on March 12th.

The main storyline remains the same. Binance and Hyperliquid are facing off for the third time. Following $JELLYJELLY and Aster, Binance is still unable to stop Hyperliquid’s continued growth, even though Hyperliquid’s ADL is triggered earlier and the apparent liquidation scale is larger.

This is not surprising, Hyperliquid's MM alliance strategy is still working, this is too weird, Hyperliquid's HLP is competing for profits.

In an era of extremes, ADL, HLP, and appendectomy

Trump made his announcement at 8 p.m., and the market maker fell critically ill an hour later.

Entangled in a web of internal and external, on-chain and off-chain funds, USDe became the Achilles' heel of market maker liquidity migration, ultimately breaking through Binance's perpetual contract price maintenance system and, under the normal operation of Ethena's minting/redemption, breaking through the weak liquidity on Perp DEX.

Binance's price feed mechanism failed on USDe, and it did not adopt Aave's 1:1 USDT hard-coding, reflecting its extreme confidence in its own liquidity. It's a pity that this confidence was given by external market makers.

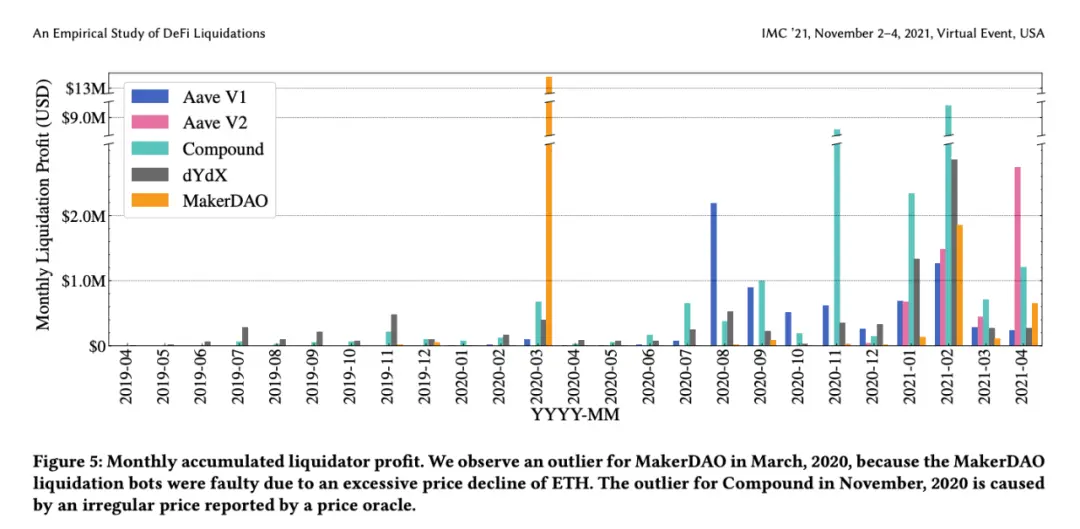

The essence of Perp is still a leveraged lending product. Due to the lack of timely human intervention, the on-chain protocol will be more proactive in considering potential crises. Take the on-chain liquidation during the DeFi Summer period as an example. Amidst the huge fluctuations, the two giants MakerDAO and Aave evolved.

Image Caption: DeFi Summer Liquidation

Image source: @KaihuaQIN

It’s just that Perp’s performance is more intense, and in order to compete, exchanges/Perp DEX will actively increase the leverage ratio or change the margin mortgage ratio. The ambiguity of the full-position/separate-position mode allows some copycats to obtain the mortgage ability of BTC and USDT.

According to a Binance customer service representative, altcoins themselves have no value, and the nearly unlimited leverage will eat up all profits. Even if all the taxes collected in Goose City are collected for decades, it will not be enough to pay it back. Bad debts are caused by the indulgence of exchanges, and are usually supplemented by funds composed of transaction fees, and ultimately by the counterparty. The exchange can still gain a reputation for calming crises.

Unlike second- and third-tier CEXs that openly or covertly support their own market makers, Binance has basically not encountered such accusations. From the previous Web3Port price manipulation to Wintermute and DWF that were FUDed on October 11, none of them can be said to be Binance ecosystem chain companies.

Binance itself is the largest liquidity in the cryptocurrency circle. The choice to maximize Binance's interests is to attract the most project parties and retail investors, so that market makers can automatically maintain liquidity. Binance earns transaction fees, project parties exit, market makers earn spreads, and retail investors pay profits to everyone.

Second- and third-tier small exchanges or numerous Perp DEXs cannot replicate Binance. Small exchanges can directly engage in market making and earn profits directly from retail investors, eliminating the intermediate processes of attracting investment (attracting project parties) and attracting capital (attracting market makers). Perp DEX uses the LP Token method pioneered by GMX to stimulate liquidity.

Ultimately, the strong stay strong, and Hyperliquid takes a middle path.

HLP attracts retail investor retention, while the market maker alliance maintains post-issuance liquidity, achieving the best of both worlds.

Binance's liquidation volume is a black box, ranging from billions to $300 billion to $400 billion. CZ turned to playing the prediction market and paid $283 million to retail investors. Referring to Bybit's operations after the theft, the exchange has been profitable since its opening. Regardless of the facts, retail investors will eventually forget.

The real danger lies with Hyperliquid. After the 1011 liquidation, cracks have appeared in Hyperliquid's alliance. HLP cooperated with ADL (Auto-Deleveraging) to liquidate $7 billion, and HLP made a profit of $40 million.

Image caption: BitMEX during the 3.12 incident

Insurance Fund Image Source: @BitMEX

ADL is called a nuclear weapon because it will take away the unrealized profits of the counterparty that creates bad debts, that is, the longs will repay the shorts' debts, and the shorts will abandon the longs' debts. Therefore, the exchange will do its utmost to avoid this from happening. If it is not handled carefully, it will be like BitMEX in 2020, doing its utmost to avoid the occurrence of ADL, saving the cryptocurrency circle but sacrificing itself (seen by the outside world as "pulling the plug", and Binance took the opportunity to rise).

The usual order of emergency response:

• Exchange: Crisis occurs –> Market-based liquidation –> Insurance funds take over positions –> ADL forces counterparties to close positions

• Perp DEX: Crisis occurs–> Market-based liquidation–> LP Vault takes over positions–> ADL forces counterparties to close positions

Theoretically, in order to maintain trading order, ADL will only be triggered after the insurance fund is unable to maintain or is exhausted. Alternatively, in order to avoid triggering ADL, the bad debt maker can close its position in advance. The price of the Perp product will extend towards -♾️, and the crisis will naturally end if it is closed before the margin is exhausted.

However, HLP will be responsible for both market making and clearing functions, which is fundamentally different from the insurance funds of Binance and BitMEX. Market making will try to maintain price stability, but clearing has a path of creating crises and can even reversely exploit the tension brought about by this contradiction.

In the $JELLYJELLY incident, large investors accumulated positions of more than $4 million in a market with a market value of $9 million. The market was no longer able to maintain counterparties and liquidity, so HLP could only passively take over the positions. In the end, all HLP holders paid for it, worth $12 million.

Neither bad debts nor profits will disappear, they will just be transferred. The profit of 40 million this time comes at the cost of a loss of 12 million last time. For a capacity of 500 million US dollars, it is still safe.

The real danger is that the dual functions of HLP will divide the interests of users, depositors and market makers.

1. Large investors or professional traders need to take advantage of Hyperliquid's No-KYC and liquidity for trading or strategy configuration. They hope that Hyperliquid remains absolutely neutral.

2. Depositors hope that HLP can make more money, that is, maintain a higher market-making share and participate in more “profitable” liquidations.

3. Market makers hope that HLP will do more clearing and less market making, participate less in the currencies in which they can make markets, and exit the market when their liquidity is insufficient.

The Hyperliquid team itself strives to maintain a balance among the three. Jeff stated that HLP's market-making share has dropped from 2% in March this year to 1% in October. Beyond public relations, HLP's market-making volume will decline, but it will not reach zero, and external market makers are not absolutely reliable.

From a development perspective, Hyperliquid needs to get rid of HLP in order to flip T0 Binance, otherwise it can only be an on-chain version of T1 CEX;

Realistically speaking, Hyperliquid cannot abandon HLP. The losses of retail investors are the source of all profits, and retail investors will invest in HLP.

Image Caption: Trading Volume and Profit

Image source: Three pictures stitched together, the original author cannot be found

Judging from the above data, Hyperliquid is the undisputed number one in Perp DEX. Even if it encounters the largest proportion of retracement, it is still the absolute OI king. The flywheel of dominance has been established, while the treasury product LLP of HL Killer such as Lighter still needs more practice.

People can discuss whether Hyperliquid was right or wrong in launching ADL too early in the controversy, but they will directly laugh at the failure of LLP's first stress test. You can be bad, but you can't be a loser.

In the extreme PVP market, Hyperliquid has at least won for now. There are really big whales who can leave with profits, and there are really HLP users who can get commissions. This is enough to support it until the time of unwinding. But what will happen in the future? HLP needs to find a balance between traders and market makers.

Who is the lender of last resort?

Liquidation is a process of gradual dam collapse, and liquidity is the strongest gravity dam.

Liquidation seems to be a failure of market making, but in fact it is a violent price fluctuation, which eventually leads to the flight of all liquidity due to stampedes and bank runs.

The ballast that was supposed to smooth out price fluctuations has now become a huge wave that makes prices more unstable.

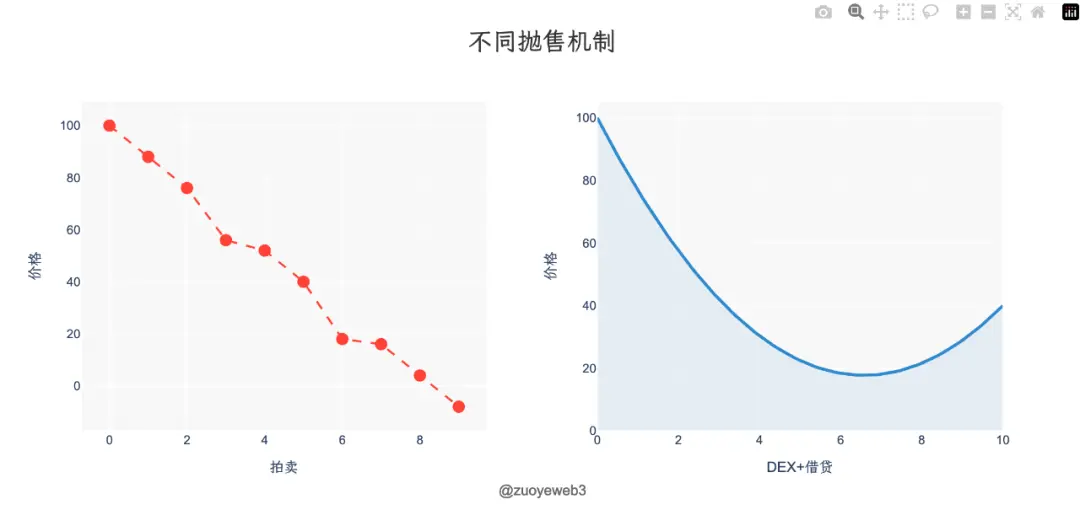

As mentioned earlier, Perp is nothing more than another form of leveraged lending, but the lending product is over-collateralized, and the liquidation mechanism has evolved from crude auction bidding and discounts to a fusion of DEX and lending. When the over-collateralization ratio drops, it is gradually sold on the DEX, turning discrete downward sell-offs into a continuous and smooth recovery.

Image caption: Price changes for different sell-off mechanisms

Image source: @zuoyeweb3

The integration of AMM DEX and lending is more friendly to liquidation, but the liquidity of Perp DEX cannot get rid of its dependence on the vault mechanism. Hyperliquid cannot do it, so don’t make it difficult for HL Killers.

Just a complaint: anything called XX Killer will ultimately fail to achieve anything great. Refer to Ethereum Killer Avalanche, Solana, and Binance Killer FTX.

Perp DEX's extreme liquidation problem (daily liquidation can be solved in a market-oriented manner) will inevitably reduce market efficiency by directly restricting price declines. The establishment of insurance funds, ADLs, margin funds, or circuit breakers can only alleviate the problem, but it is impossible to convince everyone through product design.

There is no room for power vacuum.

Binance has a large liquidation volume because of its large market size. HL's liquidation scale is also larger than Lighter's. HLP gives up the interests of traders. In the long run, in order to make the protocol more neutral, the market making/liquidation role must be productized, otherwise the protocol will inevitably act as the final liquidator.

Who acts as the lender of last resort in the crypto market? Assets like BTC, super market makers, or exchanges?

• Perp DEX Protocol: Current trading volume cannot sustain its existence, even Hyperliquid has not escaped the gravity of Binance

• BTC: Assuming the asset will slowly recover its market value, it may take many years, and the half-life of a 4-year cycle is about 2 years, refer to the FTX crash

• MM: I am lucky not to lose everything. There is no way to force action. The fate of Wintermute / GSR / Flow Traders / DWF is uncertain.

• CEX: Without external supervision, it is almost impossible to be established or operate. No one really believes that Binance will take care of the interests of retail investors, right?

One more thing to say is that Binance is still far superior to Hyperliquid. The large liquidation volume this time is also due to scale issues. From the perspective of system robustness, HL>BN>Lighter. From the perspective of market stability, BN>HL>others.

If Hyperliquid's trading volume expands 10 times to the scale of Binance, Binance's current problems will also become Hyperliquid's problems in the future. After all, what more industrially developed countries show to less industrially developed countries is only the future picture of the latter.

On the issue of liquidation, HLP is the appendix of Perp DEX since GMX, imitating AMM DEX LP. In addition to providing liquidity, it adds liquidation functions. However, the interests of HLP and Hyperliquid themselves cannot be completely separated. Even if ADL liquidation does not "take care" of HLP's positions, no one can guarantee that this will always be the case.

Market rumors say that Ethena and CEX have formed an alliance of interests and will be "taken care of" by the ADL system, because CEX is mainly an investor in Ethena. If they can protect Ethena, they can protect themselves, market makers and large investors, and a world where only retail investors are harmed will be achieved.

From the perspectives of assets and price discovery mechanisms, the former regards ADL as a fat-tail event. Due to the volatility and lack of supervision of cryptocurrencies, the frequency of black swans far exceeds that of traditional financial markets, and the recovery mechanism mainly relies on self-healing.

Image source: @zuoyeweb3

Here is an ADL options product concept I envisioned. Based on Hyperliquid's open, transparent, and automated ADL data, you can design a binary options or prediction market product to encourage everyone to invest part of their commission when opening an order, or HLP to invest part of the commission into it, which will be used as liquidity to predict the probability of triggering ADL.

In terms of liquidity sources, since ADL does not occur frequently (although the probability is relatively high, the probability of it occurring once a day/week/month is still low), it can be designed to expire monthly to attract market makers or retail investors who are betting against each other, or even directly use the HIP-3 mechanism to do it.

Since the liquidation data reported by CEXs such as Binance is not transparent, most of the unrealized profits cannot be recovered. Therefore, the purpose of ADL options is not insurance compensation and it is unable to compensate all the losses of ADL victims. However, as long as it exceeds the compensation of Binance, there is a market for it.

In order to ensure the safety of HLP, the Hyperliquid team has the urge to trigger ADL as soon as possible. Setting up options for hedging is the best way, hedging with spot contracts, hedging with contract options, and unlimited nesting dolls.

The other is the price discovery mechanism, that is, technological innovation. Variational adopts RFQ matching and OLP unified market making mechanism, as well as P2P liquidation strategy.

• RFQ, users ask market makers for prices and become market players

• OLP, Variational unified management of market making mechanism, any user is trading with OLP, users deposit OLP to have income

• P2P, after the user places an order, OLP will find a matching order and fully balance it. Even if bad debts occur, it will not affect other

But this is not a Variational soft article, so we must objectively consider the problems existing in the above mechanism, mainly the liquidity problem. Yes, everything is a liquidity problem.

Variational is essentially a clearing agreement that mixes on-chain/off-chain, CEX/DEX. You bet against OLP, which itself has insufficient liquidity and may even place orders on Hyperliquid or Binance. In other words, users are essentially trading with market makers on Binance. The significance of Variational doing this is that large customers can get discounts.

Secondly, OLP is the only market maker. Although the agreement states that it will not engage in malicious market making, the black box market making strategy is difficult to be fully recognized by the market. Even the fully transparent (Fully 0N-Chain) Hyperliquid's governance mainly takes place in Discord.

Asset X price corresponds to collateral X leverage. The unlimited extension of leverage will eventually make the collateral lose its value.

Conclusion

Hear thunder in the silence, the market microstructure is constantly changing.

On March 12, 2020, BitMEX “pulled the plug” and saved the crypto market. At the expense of BitmEX’s market share, Binance has since risen.

2022.11.8 FTX was insolvent and ultimately failed to save itself, sacrificing SBF and the entire industry, and the crypto market stagnated.

On October 11, 2025, Binance used partial transparency and public relations to save itself. Hyperliquid used ADL to force liquidation of profitable positions, leaving the outcome uncertain.

But in any case, liquidation has become the most difficult problem to solve for Perp products. As Hyperliquid grows, it may only take one more margin call for it to be brought under regulation. Hopefully, before that, the crypto field can cultivate its own lender of last resort, demonstrating its advancement compared to Wall Street.