summary

●In April 2025, the Trump administration announced the launch of a "reciprocal tariff" policy, imposing a uniform "minimum benchmark tariff" of 10% on global trading partners. This policy triggered violent fluctuations in global risk assets.

●Bitcoin is a public chain that mainly uses the PoW (Proof of Work) mechanism. The PoW mechanism relies on physical mining machines for mining. Mining machines are not on the US tariff exemption list, so mining companies face greater cost pressure.

●The decline of mining machine manufacturers in the past month is the most obvious. The core reason is that mining machine manufacturing has been hit by tariff policies on both the supply side and the demand side.

● Self-operated mining farms are mainly affected by the supply side, and the business process of selling Bitcoin to cryptocurrency exchanges is less affected by tariff policies.

●Cloud computing mining farms are relatively least affected by tariff policies because the essence of cloud computing is to pass on the cost of purchasing mining machines to customers through computing service fees. Therefore, the erosion of platform profits is significantly weaker than the traditional mining model.

●Although the tariff policy has hit the Bitcoin mining industry in the United States, Bitcoin spot ETF funds represented by BlackRock IBIT and US stock companies that hoard Bitcoin represented by MicroStrategy still hold the pricing power of Bitcoin.

●Bitcoin price is no longer the only indicator. Policy trends, geo-security, energy scheduling, and manufacturing stability are the real keys to the survival of the mining industry.

Keywords: Gate Research, tariffs, Bitcoin, Bitcoin mining

Preface

On April 2, the Trump administration announced the launch of a "reciprocal tariff" policy, imposing a uniform "minimum base tariff" of 10% on global trading partners, and imposing "personalized" high tariffs on countries with significant trade deficits. The policy triggered a sharp shock in global risk assets, with both the S&P 500 and Nasdaq recording their largest single-day declines since March 2020; assets in the cryptocurrency industry also shrunk significantly. Since Trump announced the tariff policy, China has announced an 84% retaliatory tariff on the United States, the European Union has imposed a 25% tariff on 21 billion euros of US goods, and the total market value of global stock markets has evaporated by more than $10 trillion in a single week.

On April 9, the tariff policy reversed, with Trump announcing a 90-day suspension of additional tariffs on 75 countries except China. The EU also suspended additional tariffs and started negotiations with the US. On that day, the S&P 500 rose 9.51%, the Nasdaq rose 12.02%, the price of Bitcoin rebounded 8.19% to $82,500, and the price of Ethereum rebounded to $1,650.

Among the many tracks of crypto assets, Bitcoin mining has become one of the on-chain economic modules most directly affected by tariff policies due to its strong dependence on hardware equipment, wide global supply chain span, and high capital intensity. The global trade frictions caused by the US reciprocal tariffs have multiple impacts on the crypto mining industry. Since most of the world's Bitcoin mining machines are manufactured in China, the Sino-US tariff war will push up the import cost of mining machines. China's export tax rate to the United States has risen to 145%, which will compress the expansion plan of North American mines; the depreciation of the RMB has increased the pressure on Chinese mining companies' dollar debts, and coupled with the fluctuations in electricity and energy prices, operating costs continue to rise. At the same time, the fluctuation of currency prices has also affected miners' income. The price of Bitcoin has retreated from US$82,500 before the announcement of tariffs to below US$75,000.

At the macro level, the Fed's concerns about stagflation and risk aversion are superimposed, the high yield of 10-year US Treasury bonds suppresses risk appetite, the financing environment is tightening, and the share prices of mining companies have fallen in tandem with the technology sector. Against the backdrop of geopolitical tensions, the global mining layout is facing reconstruction, and companies may accelerate their transfer to tariff-friendly regions such as Southeast Asia and the Middle East. In the short term, policy uncertainty will continue to amplify the risks of Bitcoin mining, and the industry may enter a new round of reshuffle.

1. Bitcoin mining suffered a direct impact from the tariff policy, and the stock prices of most related companies fell more than the NASDAQ 100 index

Bitcoin is a public chain that mainly uses the PoW (proof of work) mechanism and is also the crypto asset with the highest market value. It is widely regarded as "digital gold". Since the PoW mechanism relies on physical mining machines for mining, and mining machines and their upstream key components such as semiconductors are not on the tariff exemption list, related mining companies are facing greater cost pressure. The upstream impact brought by the tariff policy may indirectly affect the medium- and long-term trend of Bitcoin prices through the cost transmission mechanism.

The main ecosystem of Bitcoin mining includes mining machines, self-operated mining farms, and cloud computing mining farms. Mining machine companies include Bitmain, Canaan Technology (NASDAQ: CAN), MicroBit, and Ebang International (NASDAQ: EBON). The main factories of several companies are located in mainland China. Among them, Bitmain occupies a major share of the mining machine market (its 2018 prospectus disclosed that its market share exceeded 70%).

Self-operated mining companies include Marathon Digital (NASDAQ: MARA), Riot Platform (NASDAQ: RIOT), Cleanspark (NASDAQ:CLSK) and many other companies. The headquarters of the self-operated mining companies listed on NASDAQ are all located in the United States, but their mining farms are distributed in many countries such as the United States, the United Arab Emirates, and Paraguay. Marathon has the world's largest mining farm, with a total computing power of more than 54EH/s, accounting for about 6% of the current total network computing power.

The main companies in cloud computing mining farms include Ant Pool, Bitdeer (NASDAQ: BTDR), BitFufu (NASDAQ: BFBF), Ecos and other companies. Unlike self-operated mining farms, cloud computing mining farms transfer part of the risk of Bitcoin price fluctuations to customers by selling the computing power required for mining to individual or institutional customers in packages. The platform itself focuses on the site selection, construction and daily operations of the mining farm. Bitdeer has some self-operated mining farms and some cloud computing mining farm businesses. BitFufu only has cloud computing business.

Affected by Trump's tariff policy, the stock prices of Bitcoin mining companies fell. Their declines exceeded the NASDAQ 100 index. Through Yahoo's yfinance database, the author captured the closing prices of 8 Bitcoin mining companies in the past month, as well as the NASDAQ 100 index as a reference standard. When Trump announced the tariff policy on April 2, the stock prices of Bitcoin mining companies fell sharply. After Trump announced the tariff policy was postponed for 90 days on April 9, the stock prices of Bitcoin mining companies rebounded significantly.

After the data is standardized, since the tariff policy was issued on April 2, mining machines have been the sector with the most significant decline in the Bitcoin mining industry, with Canaan Technology falling by more than 17% and Ebang International falling by more than 11%. The second largest sector is the self-operated mining farm sector, with Core Scientific leading the decline, with a drop of more than 10% in the past month; Marathon's drop is only 0.8%, the lowest in the sector. Finally, cloud computing mining farms are less affected, with BitFufu falling by only 5.9%. The NASDAQ100 index, which is used as a reference standard, fell by 2.2%.

Table 1: Performance of Bitcoin Mining Companies and Nasdaq 100 Index (NDX) in the Last Month

2. Analysis of the impact of tariff policies on various sectors of Bitcoin mining

After Trump announced the tariff policy, Bitcoin mining companies all experienced different declines, but as mentioned above, the stock price performance of each sub-sector also showed a certain degree of differentiation. The core reason for this is that each link in the Bitcoin mining supply chain is subject to different levels of tariffs.

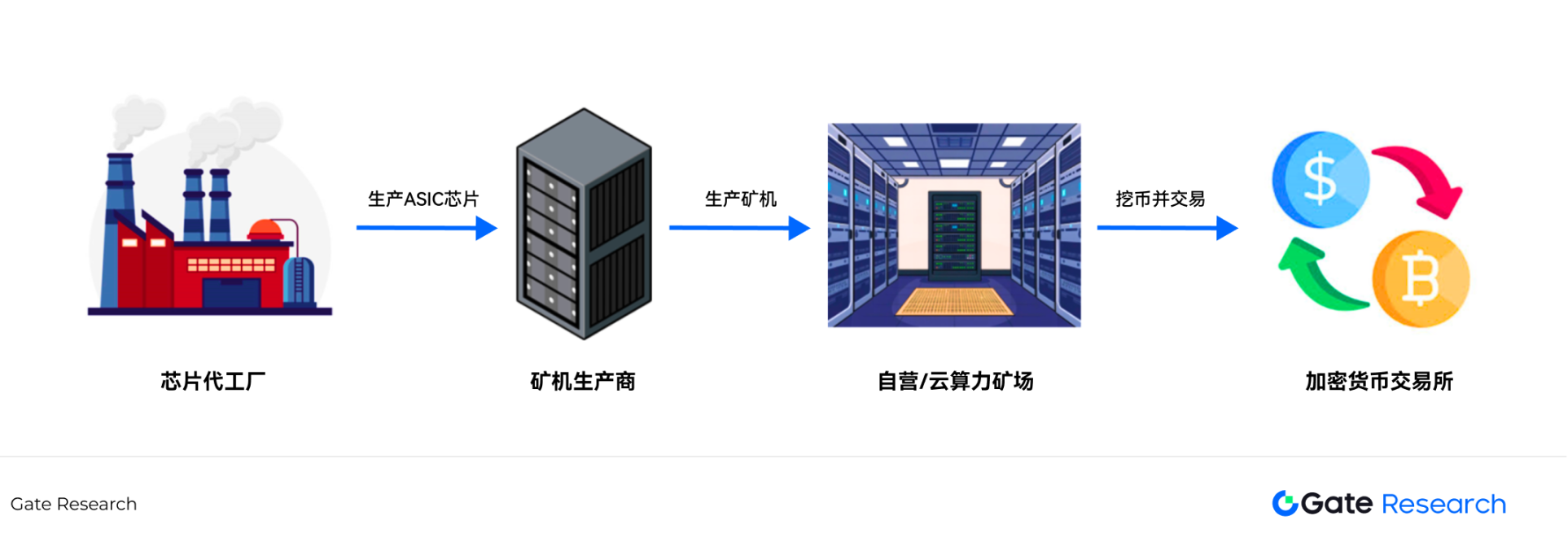

Figure 1: Bitcoin mining core supply chain

2.1 Mining Machine Manufacturers

Judging from the stock price performance, the decline of mining machine manufacturers in the past month is the most obvious. The core reason is that mining machine manufacturing has been hit by tariff policies on both the supply side and the demand side. The upstream of mining machine production is TSMC, Samsung, SMIC and other foundries. The mining machine company first completes the IC design of the ASIC chip independently, and then delivers the drawings to the foundry for tape-out. After the tape-out is successful, the foundry will mass-produce the ASIC chip, and the mining machine company will get the chip and package it into a mining machine.

TSMC holds a 64.9% market share in the chip foundry sector [1]. The Trump administration requires TSMC to build a factory in the United States, otherwise it will impose tariffs of more than 100% [2]. Foundries such as SMIC, Hua Hong Semiconductor, and Samsung are also under pressure from high tariffs from the United States. Foundries have only two options: paying tariffs or reducing orders from the United States. Either way, the profits of the foundries will decline. This part of the pressure may be transferred to downstream mining machine manufacturers, forcing manufacturers to pay higher prices in order to increase the gross profit margin of foundry orders.

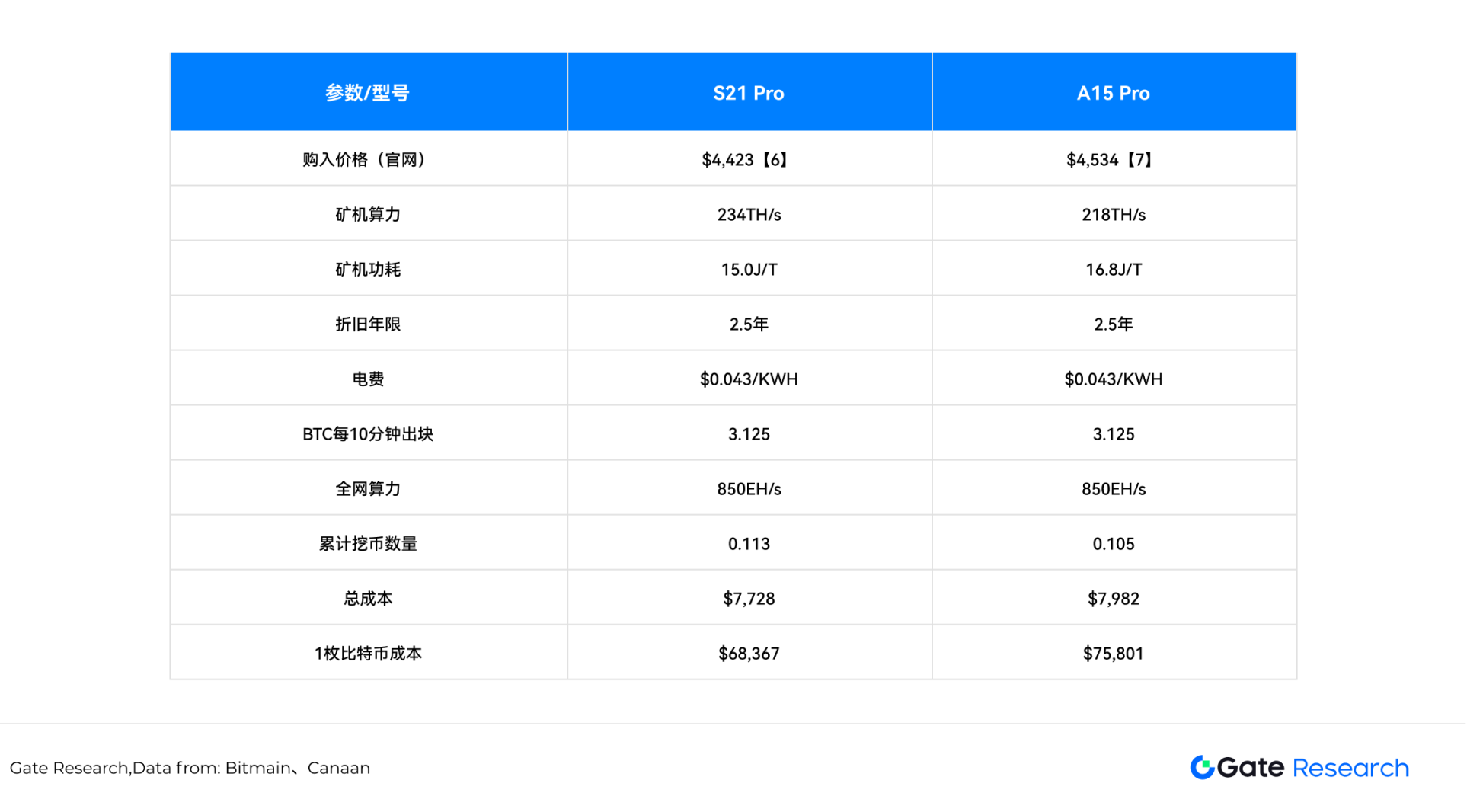

From the demand side, since Bitmain, Canaan Technology, MicroBT and other companies are all registered in China, American mining farms such as Marathon, Riot, and Cleanspark have to bear high tariffs and pay higher costs when purchasing mining machines. Therefore, in the short term, orders for mining machines will shrink significantly. Take Bitmain's main model Ant S21 Pro and Canaan Technology's main model Avalon A15 Pro as examples. Before the tariff policy is implemented, without considering operating costs, assuming that the electricity price cost is $0.043/KWH (Cleanspark's electricity price cost in 2024) [3], the total network computing power is 850EH/s [4], and the depreciation period of the mining machine is 30 months [5]. At present, the cost of mining one bitcoin for S21 Pro is $68,367, and the cost of mining one bitcoin for A15 Pro is $75,801.

Table 2: Parameters of mainstream mining machines in Bitcoin mining

Note 1: The main calculation formula is as follows:

Cumulative number of coins mined = mining machine computing power × 60 × 24 × 365 × depreciation period × block reward / 10 / total network computing power / 1000,000

Total cost = mining machine price + mining machine computing power × mining machine power consumption × electricity cost × 24 × 365/1,000 (excluding personnel and site rental costs)

Mining cost = total cost / cumulative number of mined coins

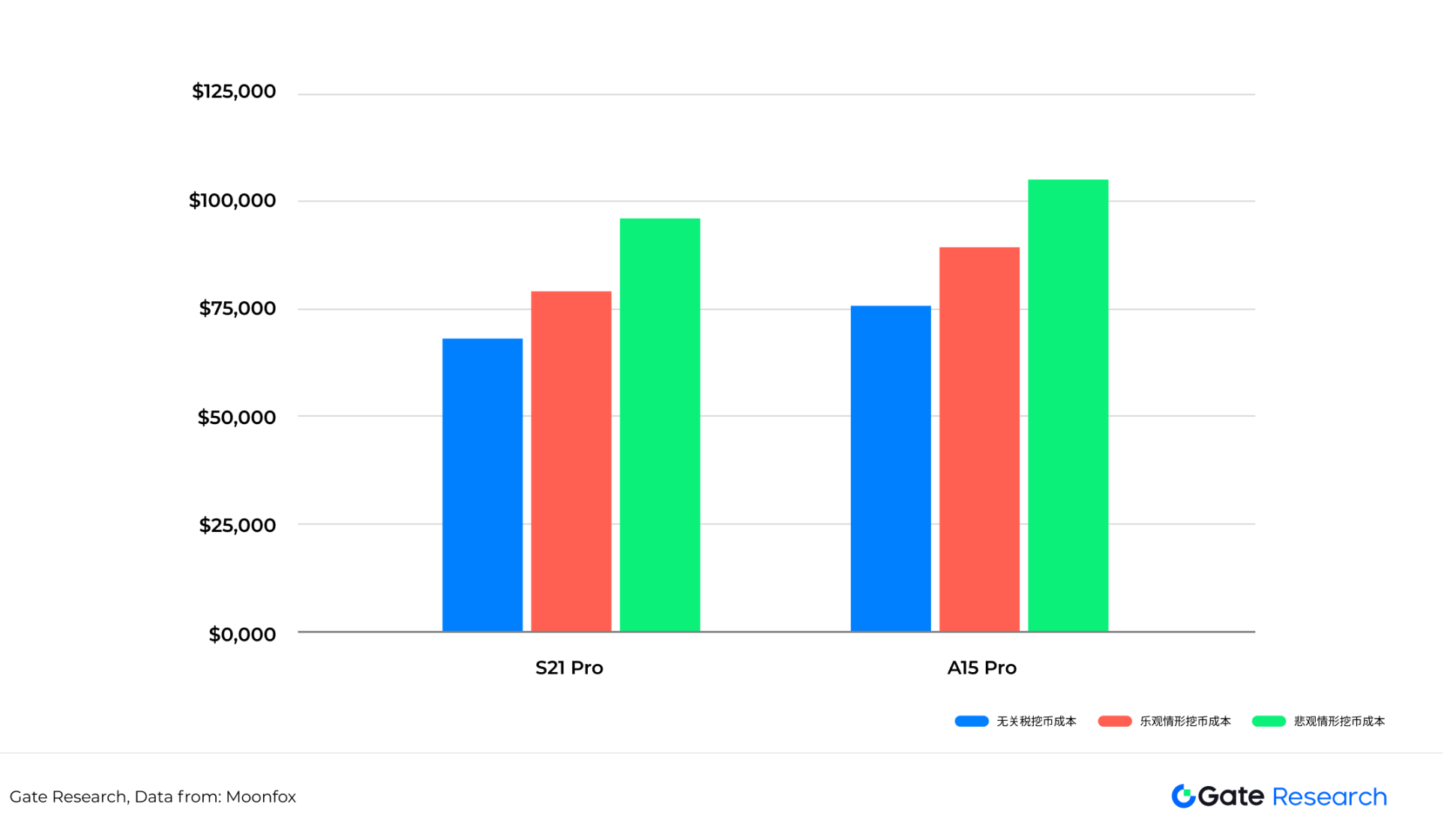

Once the tariff policy is implemented, in the optimistic scenario, the price of exported mining machines will increase by 30% from the original basis, and the cost of mining 1 Bitcoin for S21 Pro will be $80,105, and the cost of mining 1 Bitcoin for A15 Pro will be $88,717. In the pessimistic scenario, the price of exported mining machines will increase by 70% from the original basis, and the cost of mining 1 Bitcoin for S21 Pro will be $95,756, and the cost of mining 1 Bitcoin for A15 Pro will be $105,938.

Table 3: Mining costs of mining machines under different tariff scenarios

The above prices do not take into account the complex operating costs of the mines, which include site rental costs and personnel costs. If these costs are taken into account, the mining costs will rise further. A substantial increase in tariffs will make the mines bear higher mining costs, and the weakening of demand will also have a significant impact on upstream mining machine manufacturers.

From a long-term perspective, mining machine manufacturers may give priority to tariff-friendly regions for capacity layout, and through global capacity allocation strategies, effectively avoid potential tariff policy risks and achieve supply chain cost optimization.

2.2 Self-operated mines

Compared with mining machine manufacturers, which are squeezed by both supply and demand, self-operated mining farms are mainly affected by the supply side. The business process of selling Bitcoin to cryptocurrency exchanges is less affected by tariff policies. The price of Bitcoin is affected by tariff policies. Funds hate uncertain policies, so short-term funds choose to flow out, and Bitcoin has fallen significantly. However, self-operated mining farms represented by Marathon will choose a hoarding strategy when there is sufficient cash flow, rather than selling Bitcoin on the exchange immediately after it is mined. Similar to MicroStrategy's strategy of borrowing money to buy coins, Marathon has issued convertible bonds many times to directly purchase Bitcoin. Therefore, large mining farms are relatively less affected by the decline in Bitcoin prices. [8][9][10][11]

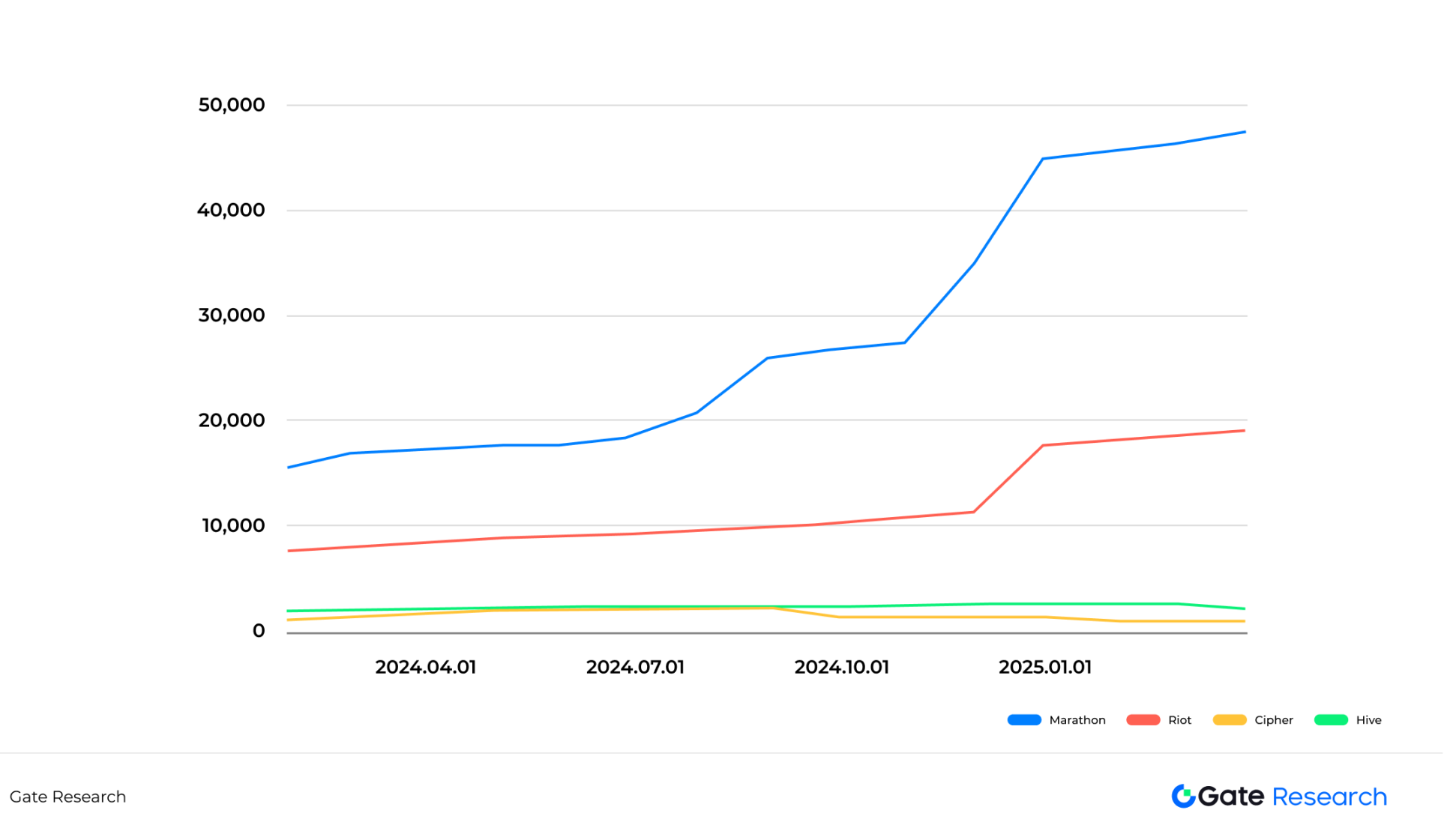

For small mining farms with tight cash flow, the decline in Bitcoin prices has a particularly significant impact on their stock prices. Due to limited funds, these mining farms are usually unable to hold the mined Bitcoin for a long time and can only sell it immediately after mining to maintain operating funds. During market downturns, this "mine and sell" strategy may increase market selling pressure and further affect Bitcoin price trends. As shown in the figure below, Cipher and Hive held 1,034 and 2,201 Bitcoins in March 2025, respectively, down 40% and 3% year-on-year; while Marathon and Riot held 47,531 and 19,223 Bitcoins in March 2025, up 173% and 126% year-on-year, respectively.

Table 4: Changes in the number of coins held by self-operated mining companies (January 2024 to March 2025)

In the past month, the share prices of small and medium-sized self-operated mining farms Cipher and Hive Digital have risen and fallen by -7.1% and -5.5% respectively since the announcement of the tariff policy. The decline in share prices is significantly greater than that of large mining farms such as Marthon that insist on hoarding coins.

However, in the long run, the depreciation cycle of mining equipment is usually 2.5 to 3 years, which means that self-operated mines need to continue capital expenditures (CAPEX) to purchase new mining machines to replace old equipment. Although the statistical calibers adopted by various mining companies when disclosing computing power data are different (such as average monthly computing power, power-on computing power, and computing power at the end of the month), it is difficult to directly compare the computing power indicators of different companies horizontally. From January 2024 to March 2025, the computing power data disclosed by mainstream listed mining companies showed that their computing power growth rate generally exceeded 70%. The core driver of the continued growth of computing power lies in "relative competitiveness": in the context of the continuous increase in the computing power of the entire network, if the computing power of the mine itself does not increase accordingly, the number of bitcoins it can mine will continue to decline. Bitcoin mining is a dynamic game, and the expansion of computing power is like sailing against the current, if you don't advance, you will retreat.

In this context, if the mining machine tariff policy is officially implemented, the cost increase pressure of upstream mining machine manufacturers will inevitably be transmitted to downstream mines, further pushing up the industry's marginal production costs and posing a challenge to the profitability of medium-sized mines.

2.3 Cloud computing mining farm

Cloud mining farms are essentially a leasing model, with mining machine manufacturers as the upstream and individual and institutional customers as the downstream. Cloud mining farms do not hold or sell coins, but instead sell 30-day, 60-day, and 90-day computing power to customers in packages. Customers will choose to hoard or sell coins based on their own judgment. Therefore, cloud mining farms mainly earn service fees paid by customers, and do not directly bear the profits or losses caused by the rise and fall of Bitcoin.

The core competitiveness of cloud computing mining farms lies in reducing rental, electricity and labor costs through site optimization, while maintaining a high degree of flexibility in computing power deployment to cope with market fluctuations - in a bull market, mining machines and sites need to be expanded rapidly to meet customer needs, and in a bear market, operations need to be streamlined and redundant computing power converted to self-mining. This dynamic balance ability directly determines the company's market competitiveness.

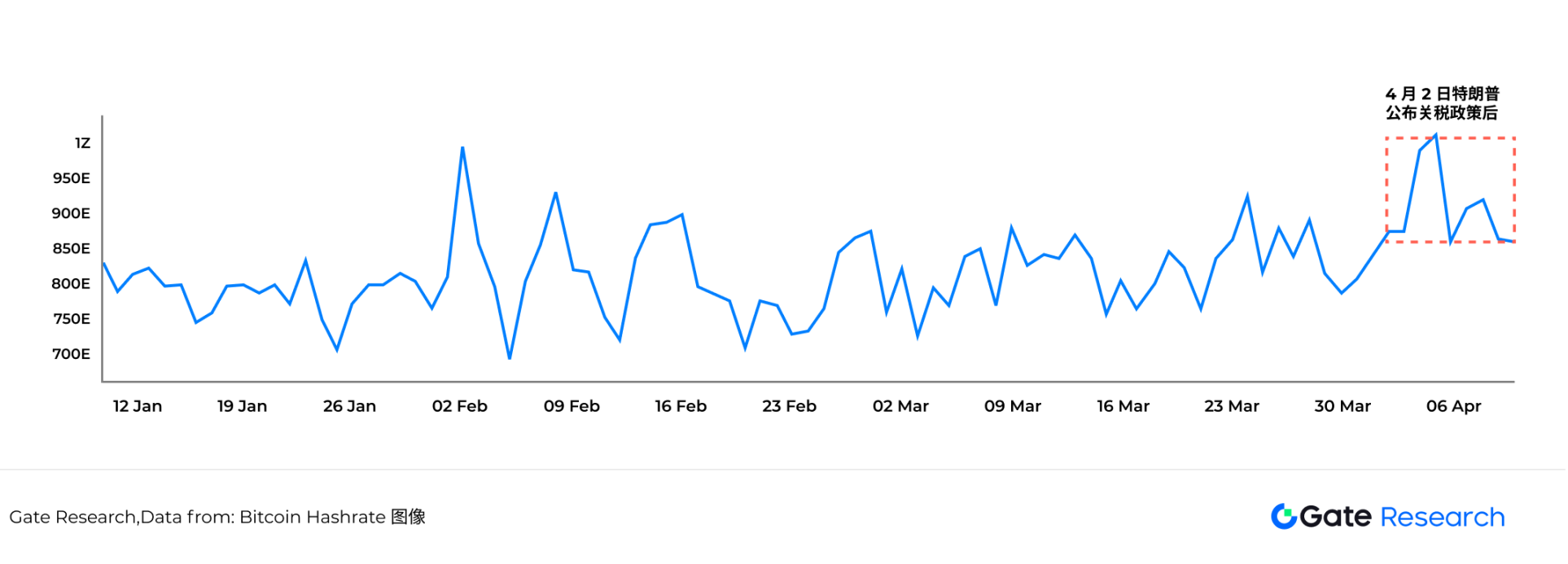

The revenue of cloud computing companies is mainly driven by the total network computing power. When the total network computing power increases, it proves that most miners are still optimistic about the future price of Bitcoin, or more customers choose to purchase cloud computing power; when the total network computing power decreases, it means that miners are not optimistic about the trend of Bitcoin prices, and the cloud computing power portion of the total network computing power will also decrease. The data in the figure below shows that after Trump announced the tariff policy on April 2, the average daily total network computing power of Bitcoin even hit a record high on April 5, breaking through 1 ZH/s for the first time. [12]

Figure 2: Changes in Bitcoin network computing power (January 2025 to April 2025)

From the cost perspective, although the price of mining machines is under upward pressure due to the transmission of tariff policies, the leasing business model of cloud computing power mining farms naturally has a risk buffer mechanism - its essence is to pass on the purchase cost of mining machines to customers through computing power service fees, and some customers directly share the hardware investment through mining machine hosting agreements, making the erosion of mining machine premiums on platform profits significantly weaker than the traditional mining model. This cost transfer and sharing feature makes cloud computing power mining farms a field that is less affected by the Trump administration's tariff policy.

3. The impact of the reshaping of the Bitcoin mining landscape on Bitcoin prices

The recent US tariffs on Bitcoin mining equipment imported from China and other countries have significantly increased the operating costs of US miners. This provides greater potential opportunities for non-US companies to enter the Bitcoin mining industry, as they can purchase Chinese-made mining machines from other countries at a lower cost, thereby gaining cost advantages. Although US mining farms can circumvent some of the impact of tariffs by setting up operating bases overseas, it is undeniable that these tariff policies have increased the operating costs and policy risks of US domestic mining farms.

According to the above deduction, the daily output of Bitcoin is 450, and the miners who mine Bitcoin will be more dispersed, and the voice of American mining companies such as Marathon, Riot, and Cleanspark may decline. Since large mining companies such as Marathon have adopted a hoarding strategy in the past, and companies in other countries that potentially enter the mining industry have an unclear attitude towards Bitcoin, they may choose a "mine, withdraw, and sell" strategy (withdraw Bitcoin immediately after mining and sell it on the exchange). From this perspective, the high tariff policy is bearish on the price trend of Bitcoin as a whole. The departure of some mining farms from the United States also violates Trump's original intention to ensure that all remaining Bitcoins are "Made in the USA".

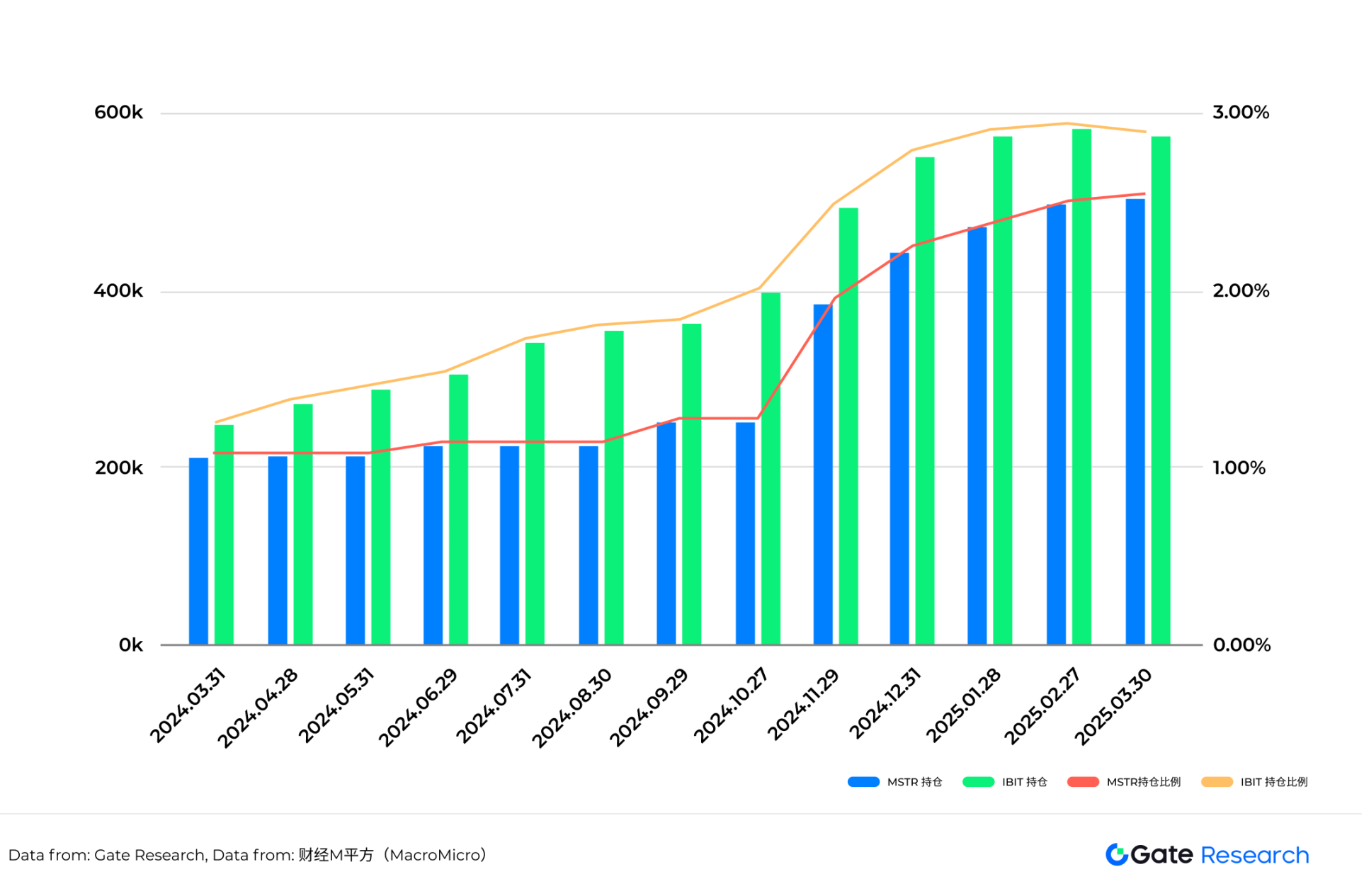

But in the long run, the core logic of Bitcoin has undergone fundamental changes in 2024. Bitcoin spot ETF funds represented by BlackRock IBIT and US stock coin hoarding companies represented by MicroStrategy still have the pricing power of Bitcoin. As of April 2025, IBIT holds 570,983 Bitcoins [13] and MicroStrategy holds 528,185 Bitcoins [14]. The proportion of Bitcoin holdings of both companies in the total circulation of Bitcoin continues to increase [15], and the purchasing power of both companies is sufficient to absorb the number of newly produced Bitcoins every day.

Table 5: Bitcoin holdings and proportions of MicroStrategy and IBIT

Summarize

The Trump administration's promotion of the "reciprocal tariff" policy poses a dual challenge to the upstream cost and geopolitical layout of the Bitcoin mining industry. Mining machine manufacturers are under the heaviest pressure due to the limited foundry chain and reduced demand, while self-operated mining farms are facing the double squeeze of cost increases and capital expenditure growth, while cloud computing power mining farms have a relatively buffering capacity relying on the "risk transfer" mechanism. Overall, the pace of North American mining expansion may be limited, and global computing power will be further dispersed to low-tariff regions such as Southeast Asia and the Middle East. The voice of American mining companies in the Bitcoin ecosystem may decline in stages.

Mining companies often have huge investments, long cycles, and weak risk resistance. The Bitcoin network itself cannot actively adjust these risks. Its mechanism is "openness, fairness, and competition" rather than "defense, response, and regulation." This has created a structural contradiction: the world's most decentralized asset, and the industrial chain behind it, is one of the areas most vulnerable to centralized policy intervention. Therefore, mining participants must re-recognize the importance of policy. Bitcoin prices are no longer the only indicator. Policy trends, geopolitical security, energy scheduling, and manufacturing stability are the real keys to the survival of the mining industry.

In the short term, the rising mining costs and the "mining, withdrawing and selling" behavior of some miners may have a marginal negative impact on the price of Bitcoin; but in the medium and long term, institutional forces represented by BlackRock IBIT and MicroStrategy have become the dominant force in the market, and their continued buying power is expected to hedge supply pressure and stabilize the market structure. The Bitcoin mining industry is in a critical period of policy reshaping and structural transfer. Global investors need to pay close attention to the rebalancing of the industrial chain brought about by policy evolution and computing power migration.

Data Source

1. Patent PC, https://patentpc.com/blog/tsmc-samsung-and-intel-whos-leading-the-semiconductor-race-latest-market-share-data

3. Cleanspark, https://www.sec.gov/Archives/edgar/data/827876/000095017024056324/clsk-ex99_1.htm

4.Bitinfocharts,https://bitinfocharts.com/comparison/bitcoin-hashrate.html

5. CoinShares Research, http://www.minerupdate.com/news/miner-insights/majority-of-bitcoin-miners-profitable-at-current-prices-according-to-coinshares-research

6. Bitmain, https://m.bitmain.com/cn/product/detail?pid=00020240402210032893O1Et7keX0682

7. Canaan, https://shop.canaan.io/products/avalon-miner-a15pro?VariantsId=10492

8. Marathon Digital, https://ir.mara.com/news-events/press-releases

9. Riot Platform, https://www.riotplatforms.com/overview/news-events/press-releases/

10. Cipher, https://investors.ciphermining.com/news-events/press-releases

11. Hive Digitalhttps://hivedigitaltechnologies.com/news/

12. Bitinforcharts,https://bitinfocharts.com/comparison/bitcoin-hashrate.html#3m

13. iShares, https://www.ishares.com/us/products/333011/ishares-bitcoin-trust-etf

14. Bitbo, https://treasuries.bitbo.io/microstrategy/

15. Finance M Square https://sc.macromicro.me/series/8120/bitcoin-circulating-supply [Bitcoin mining core supply chain https://docs.google.com/presentation/d/1BjG5mUX7eeIw48ILD6VqIlnsOQY2fQhYXigXw5XxqL4/edit?slide=id.p#slide=id.p]