By Tanay Ved

Compiled by: Vernacular Blockchain

Key Takeaways:

1. Circle achieves $1.7 billion in revenue in 2024, 99% of which comes from interest income on USDC reserves. Allocation costs with partners such as Coinbase and BN total $1.01 billion, reflecting the key role of trading platforms in expanding USDC coverage.

2. USDC total supply has recovered to $60 billion, and the 30-day average transfer volume has reached $40 billion, indicating the recovery of market confidence and cross-chain adoption. However, USDC is still sensitive to interest rate changes, competitive pressures, and regulatory developments.

3. USDC usage continues to grow on major exchanges, currently accounting for 29% of BN spot volume, thanks to a strategic partnership with Circle.

4. Looking ahead, Circle’s next phase may rely on diversification from passive interest income to active income sources, including tokenized assets, payment infrastructure, and capital market integration.

introduction

Circle, the largest U.S. stablecoin issuer and the company behind the $60 billion USDC, recently filed for an IPO, providing insight into the financials and strategic outlook of this fundamental cryptocurrency company. As the only way for public markets to directly invest in the fastest-growing sector of cryptocurrency, Circle's IPO filing comes at a critical time when stablecoin legislation is taking shape and competition is intensifying. Although market conditions may cause IPO delays, combined with USDC's on-chain data, we will extract key information from Circle's IPO filing, analyze its revenue sources, the impact of interest rates on its business, and the role of platforms such as Coinbase and BN in shaping USDC distribution, and evaluate Circle's positioning in an increasingly competitive market.

Circle Financial Overview

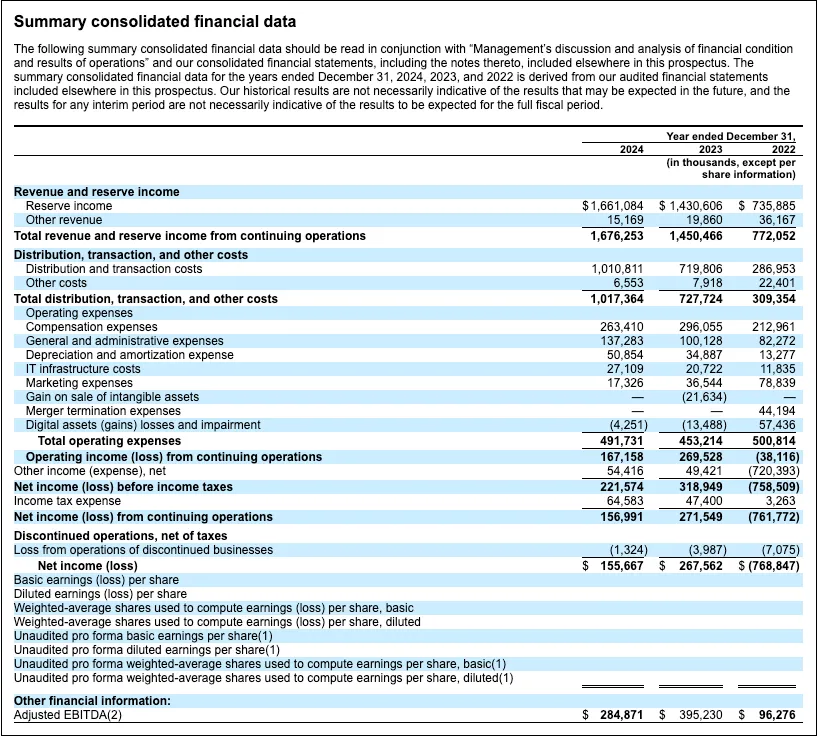

From its original Bitcoin payment application to becoming a leading stablecoin issuer and crypto infrastructure provider, Circle has faced many challenges in its 12-year journey. After explosive revenue growth in 2021 (450%) and 2022 (808%), growth slowed in 2023, with revenue growth of 88%, when USDC was affected by the collapse of Silicon Valley Bank. At the end of 2024, Circle reported revenue of $1.7 billion, a year-on-year increase of 15%, showing a more stable expansion trend.

Source: Circle S-1 filing

However, profitability was compressed, with net profit and adjusted EBITDA falling 42% and 28% to $157 million and $285 million, respectively. It is worth noting that Circle's financial data shows that revenue is highly concentrated in reserve interest income, and the distribution costs with partners such as Coinbase and BN are as high as about $1.01 billion. But these factors have driven the recovery of USDC supply, which increased 80% to $44 billion for the full year.

USDC’s on-chain growth

USDC is the core of Circle's business and was launched in 2018 in partnership with Coinbase. USDC is a tokenized form of the U.S. dollar that allows users to store value in digital form and trade on a blockchain network, enabling near-instant low-cost settlement. USDC uses a full reserve model and is 1:1 backed by highly liquid assets, including short-term U.S. Treasury bonds, overnight repurchase agreements, and cash held by regulated financial institutions.

Source: Coin Metrics Network Data Pro & Coin Metrics Labs

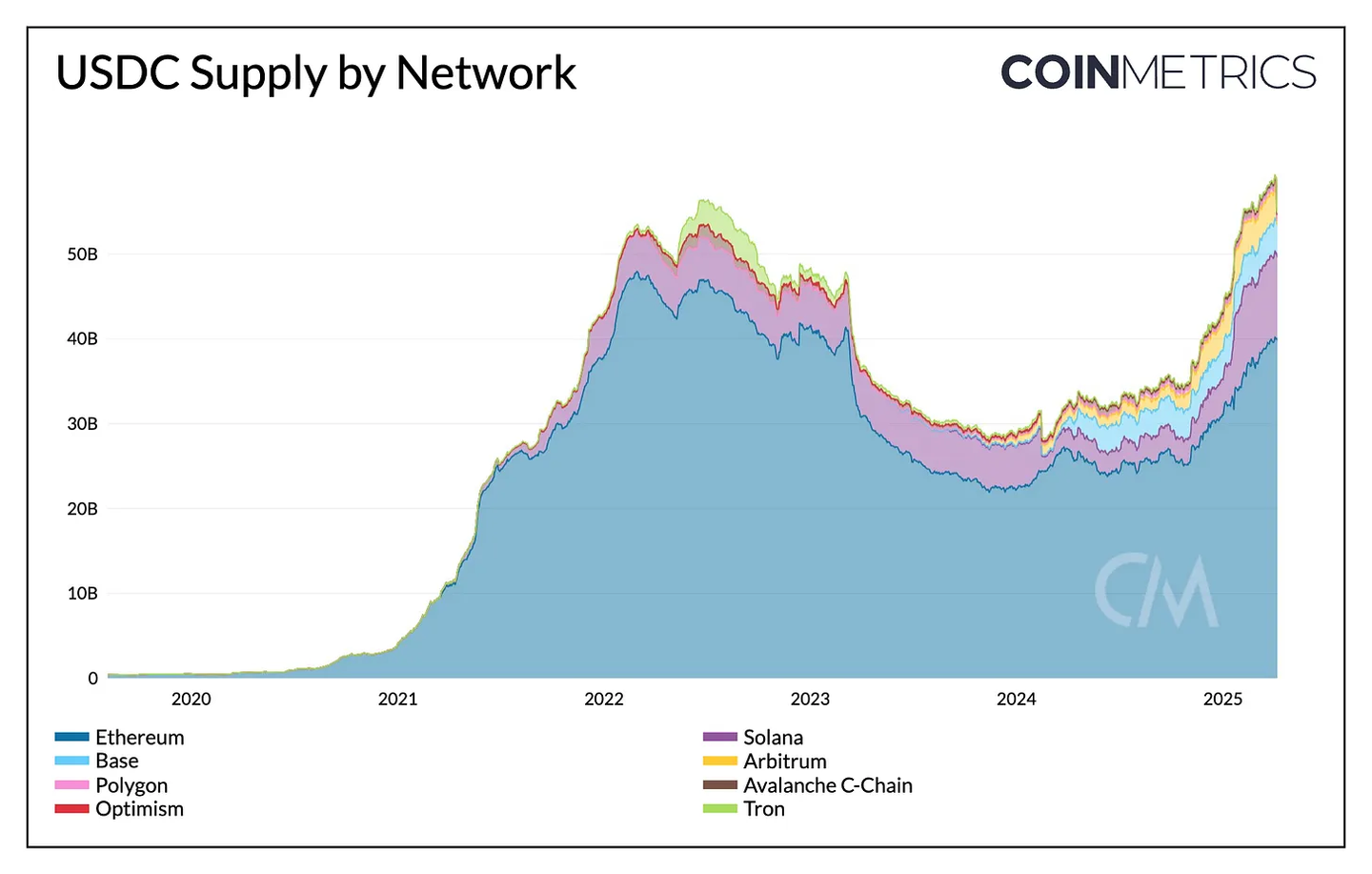

The total supply of USDC has grown to about $60 billion, firmly ranking second in the stablecoin market after Tether's USDT. Although market share was under pressure in 2023, it has rebounded to 26%, reflecting the recovery of market confidence. Of this, about $40 billion (65%) was issued on Ethereum, $9.5 billion on Solana (15%), $3.75 billion on Base Layer-2 (6%), and the rest on Arbitrum, Optimism, Polygon, Avalanche and other chains.

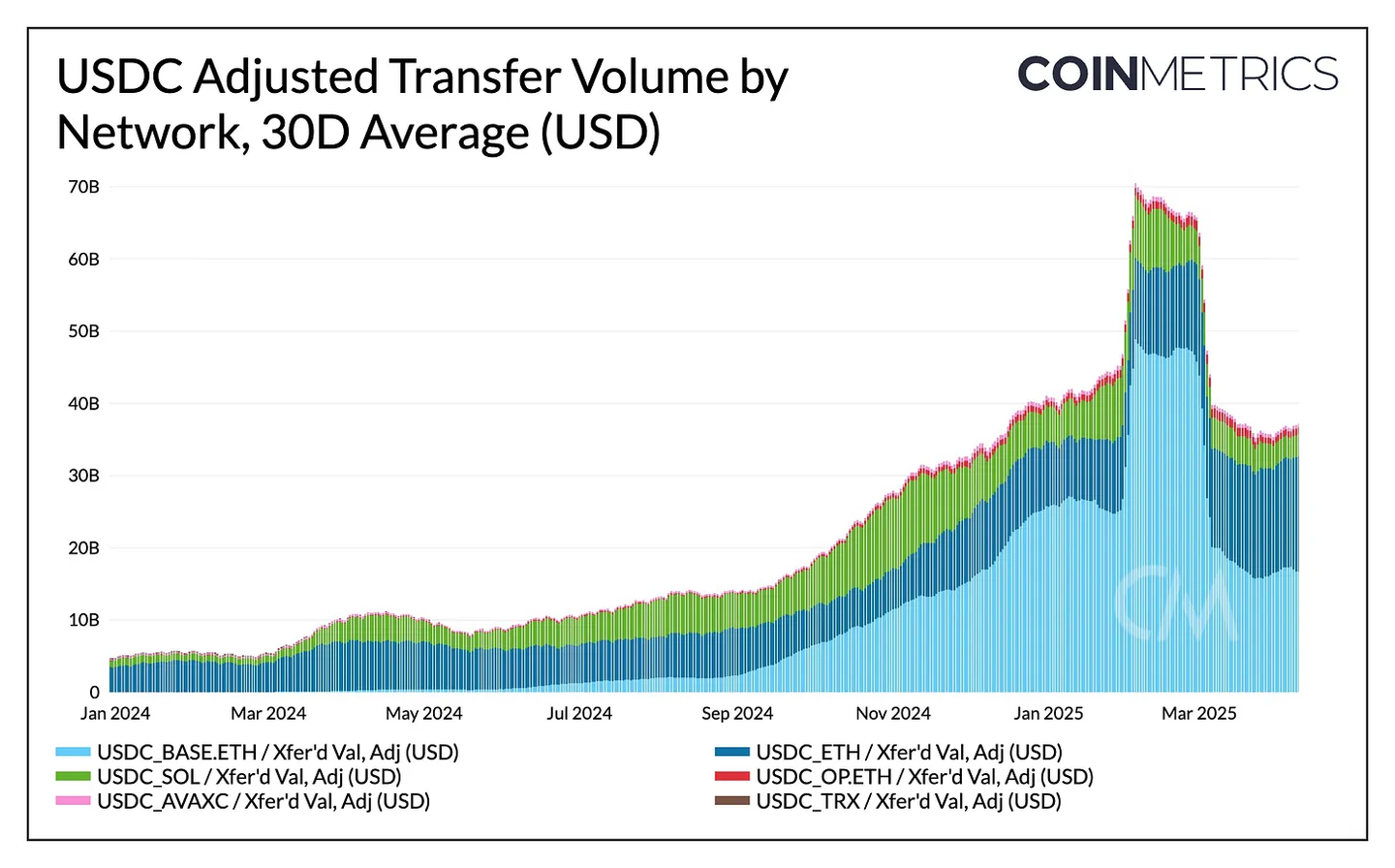

USDC's speed and transfer volume have also grown significantly, with a 30-day average transfer volume of approximately $40 billion. In 2025, USDC transfers occurred primarily on Base and Ethereum, sometimes accounting for 90% of total adjusted transfer volume.

Source: Coin Metrics Network Data Pro

These indicators show that the use of USDC is growing as stablecoins gain traction as an alternative to the US dollar in emerging markets and in payment and fintech infrastructure. This also reflects Circle's cross-chain strategy, with USDC generally available on major blockchains and supported by interoperability tools such as the Cross-Chain Transfer Protocol (CCTP).

Reserve Composition and Interest Rate Sensitivity

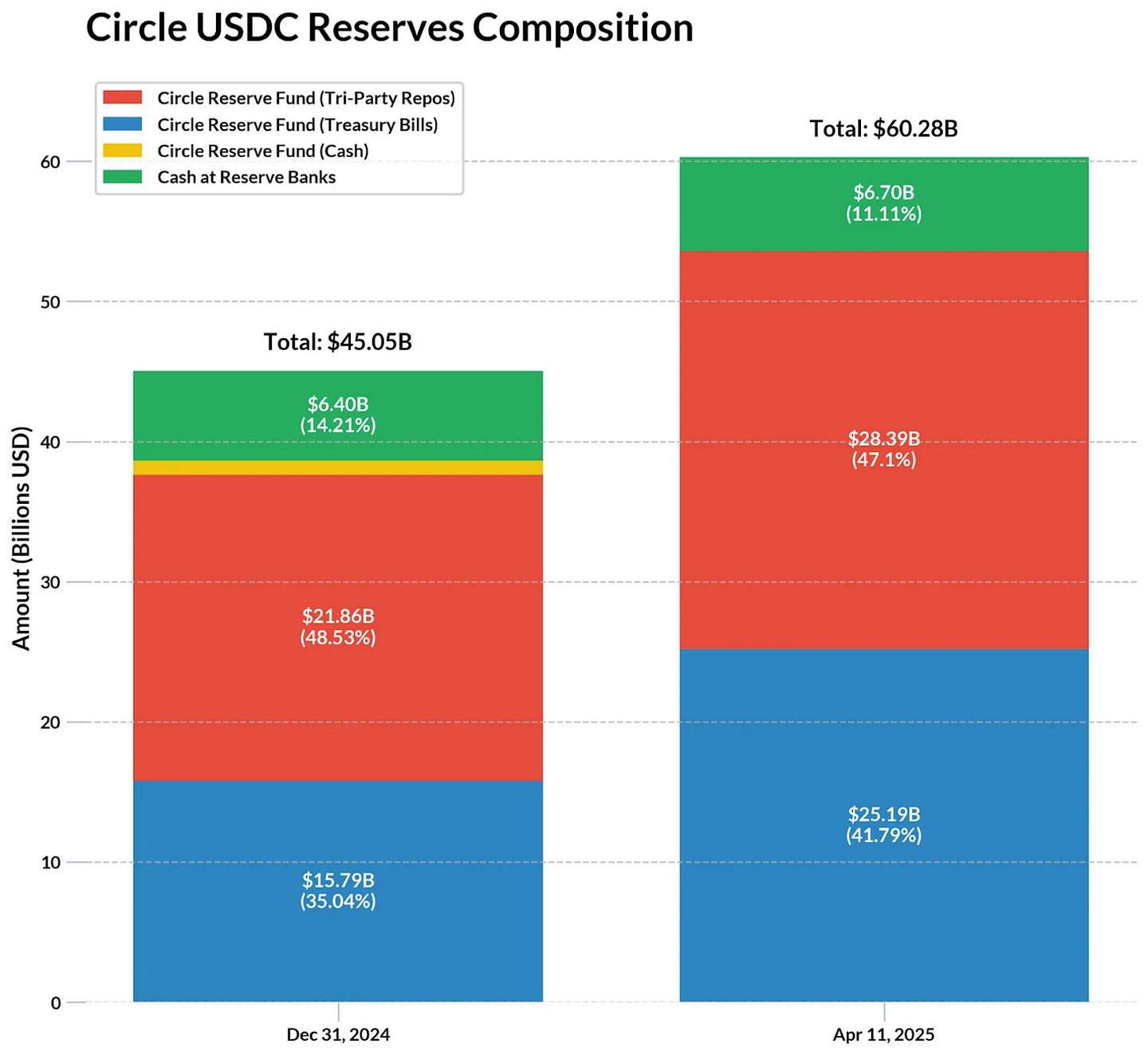

For every dollar of USDC issued, Circle invests the reserve in a portfolio of highly liquid, low-risk assets such as short-term U.S. Treasuries and cash deposits. This structure enables Circle to earn income from reserves while ensuring liquidity and redemption stability for USDC holders. Circle disclosed in the document that reserve income in 2024 was $1.6 billion, accounting for 99% of total revenue, indicating that its revenue structure is highly dependent on interest rates.

USDC reserves are mainly held in the Circle Reserve Fund, an SEC-registered government money market fund managed by BlackRock. According to Circle's monthly certifications, financial statements and the BlackRock Circle Reserve Fund, as of April 11, $53.5 billion (about 88%) of USDC reserves consisted of U.S. Treasuries and overnight repurchase agreements with multiple financial institutions, all with maturities of less than 2 months. In addition, 11% of the reserves are cash deposited in regulated banks.

Source: Circle Transparency & BlackRock Circle Reserve Fund

Based on Circle's $1.6 billion in reserve income and approximately $44 billion in reserve assets in 2024, the estimated annualized yield is approximately 3.6%. If interest rates remain at current levels and the supply of USDC remains stable or grows, Circle's reserve income is likely to remain stable.

Our previous research on the decline in USDC supply during periods of rising interest rates showed that Circle's reserve revenue is highly correlated to current interest rates, indicating the sensitivity of its revenue model to interest rate changes. With the effective federal funds rate between 4.58-5.33% in 2024, what are Circle's prospects if interest rates fall? In the S-1 filing, Circle estimated that a 1% drop in interest rates could result in a $441 million reduction in stablecoin reserve revenue, which is a key risk outlined in the filing.

Because Circle retains all earnings (unlike issuers like Ethena and Maker who pass on interest to holders), its business model remains sensitive to future interest rate changes, competitive pressures, and regulatory evolution.

Distribute, distribute, distribute

The role of Coinbase and BN

Circle’s IPO filing also reveals the importance of partners such as Coinbase and BN in driving USDC adoption. In 2024, its distribution costs totaled $1.01 billion, a 40% increase from 2023 and a 150% increase from 2022.

While Coinbase’s relationship with Circle is well known, the filings show that the two are even more closely tied financially. In 2024, Coinbase earned $908 million from USDC-related activities, or about 13.8% of its total revenue. Under its revenue-sharing agreement with Circle, Coinbase receives 100% interest on USDC held on its platform and 50% interest on USDC held elsewhere. With the supply of USDC on the Coinbase platform increasing from 5% to 20% in 2022, most of the economic gains appear to have accrued to Coinbase. The filings also disclosed a one-time payment of $60.25 million to BN to facilitate distribution in a similar manner.

Source: Coin Metrics Market Data Feed

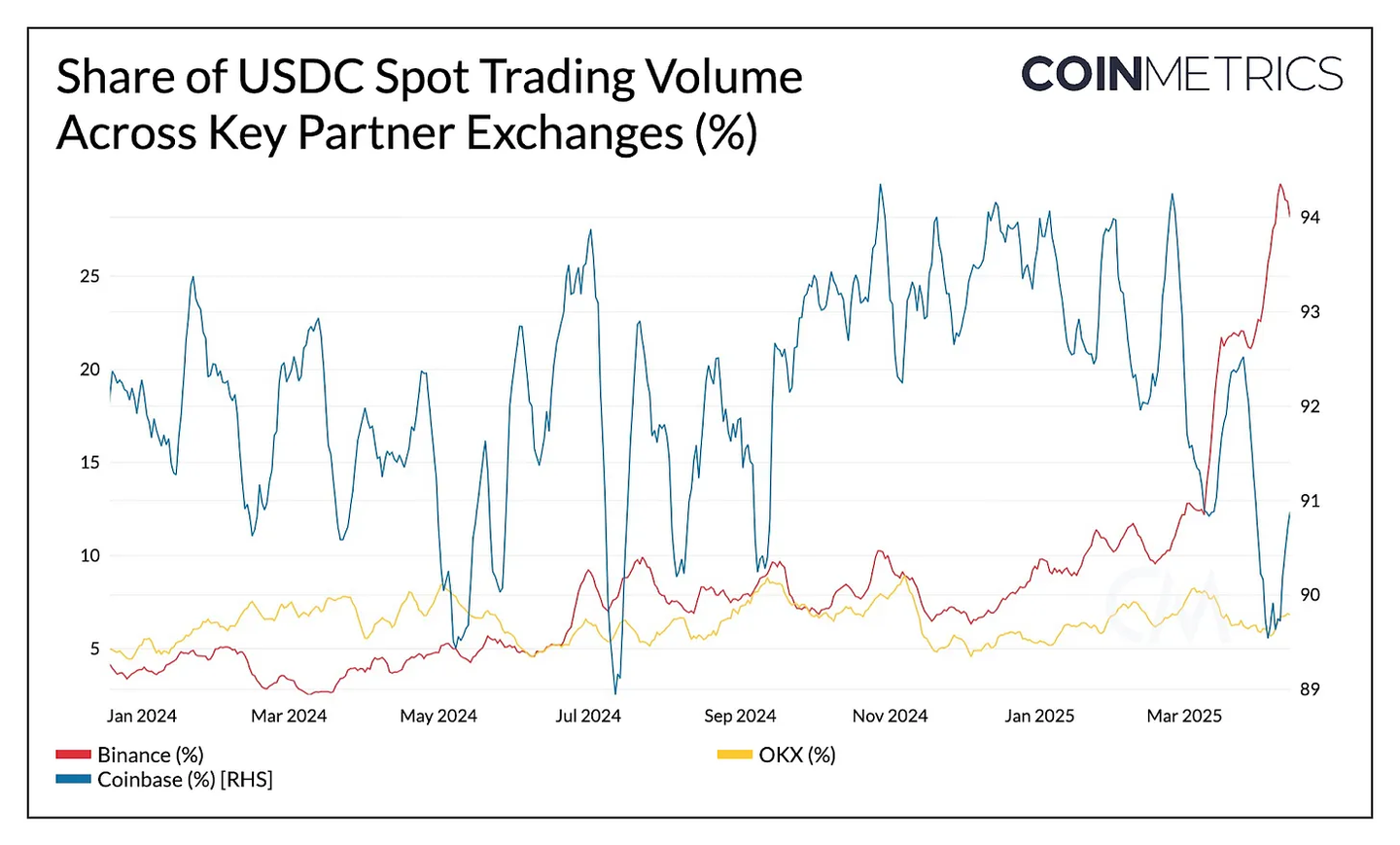

Looking at spot trading activity on key partner exchanges, USDC now accounts for 29% of BN spot trading volume (about $6.2 billion), surpassing FDUSD’s share after its recent decoupling, and second only to USDT, which accounts for about 50%. On Coinbase, USDC drives about 90% of spot trading in the combined USD and USDC market.

Despite the high costs, Circle’s distribution efforts have translated into significant adoption at the exchange level, driving USDC liquidity and $10 billion in trusted spot volume across exchanges.

Beyond Trading Platforms: Empowering DeFi and Business

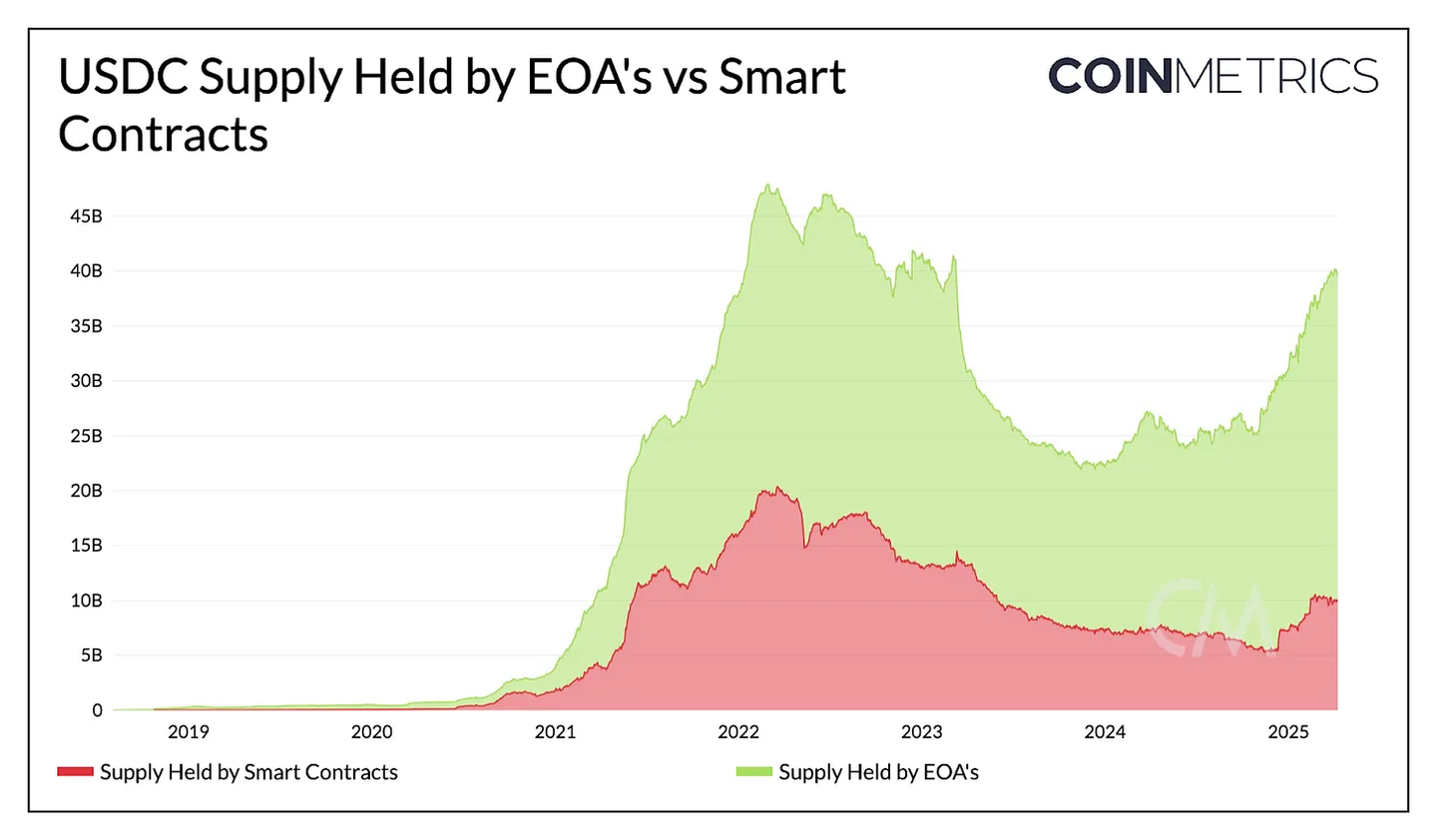

By distinguishing the supply of USDC held in smart contracts and externally owned accounts (EOAs) on Ethereum, we can understand the distribution of USDC in user wallets and applications. Currently, about $30 billion is held by EOAs, a year-on-year increase of 66%, while about $10 billion is in smart contracts, a year-on-year increase of about 42%. The growth of EOA balances may reflect the increase in exchange platform custody and individual user holdings, while the growth of smart contracts indicates the importance of USDC as collateral in the DeFi lending market and the liquidity of decentralized exchanges (DEX).

Source: Coin Metrics Network Data Pro

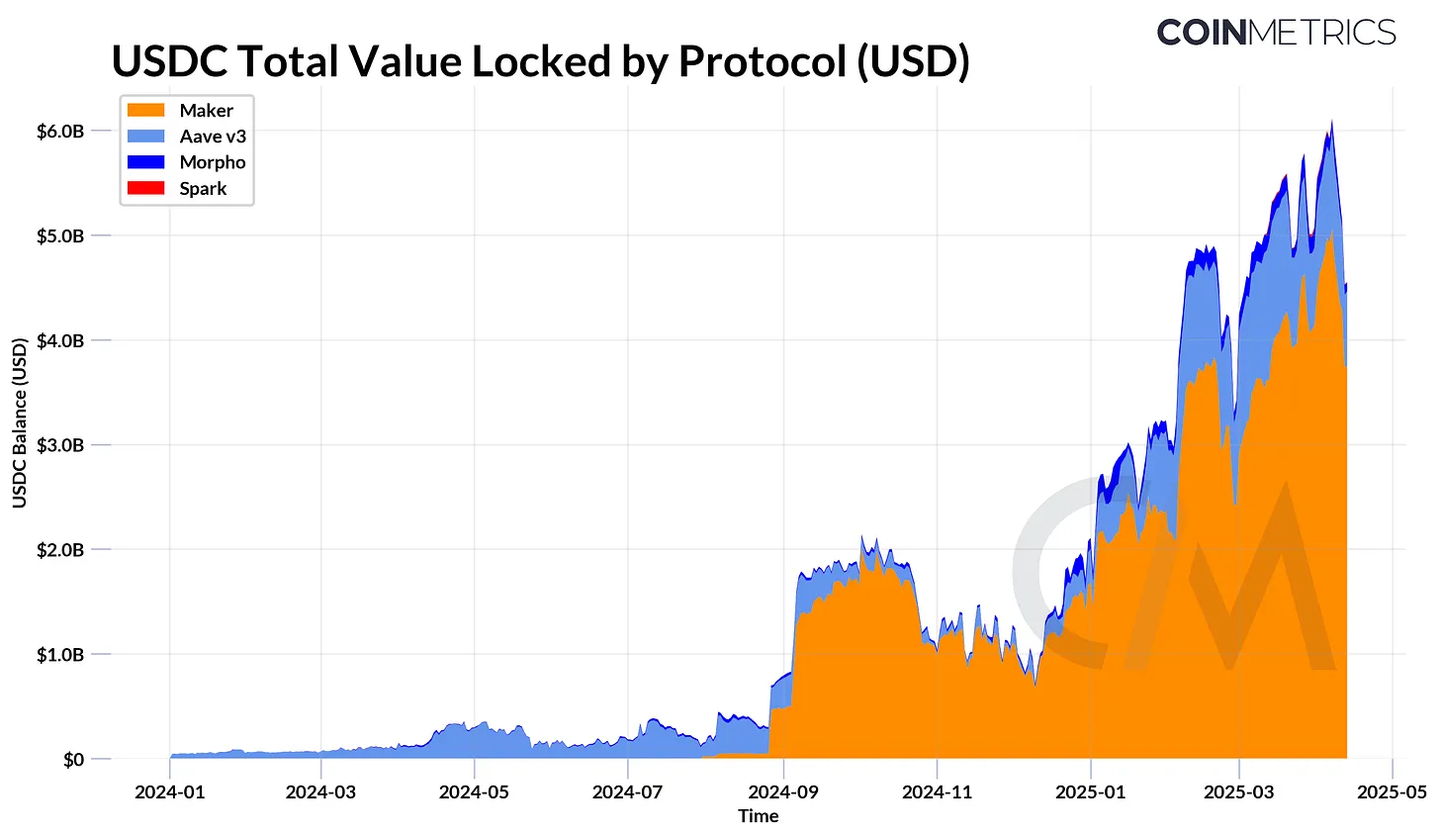

USDC continues to play a fundamental role in the DeFi lending market, with protocols such as Aave, Spark, and Morpho locking in over $5 billion (representing the portion of USDC supply that is not borrowed). For collateralized debt protocols such as Maker (now Sky), about $4 billion of USDC supports the issuance of Dai/USDS through its peg stable module.

Source: Coin Metrics ATLAS & Reference Rates

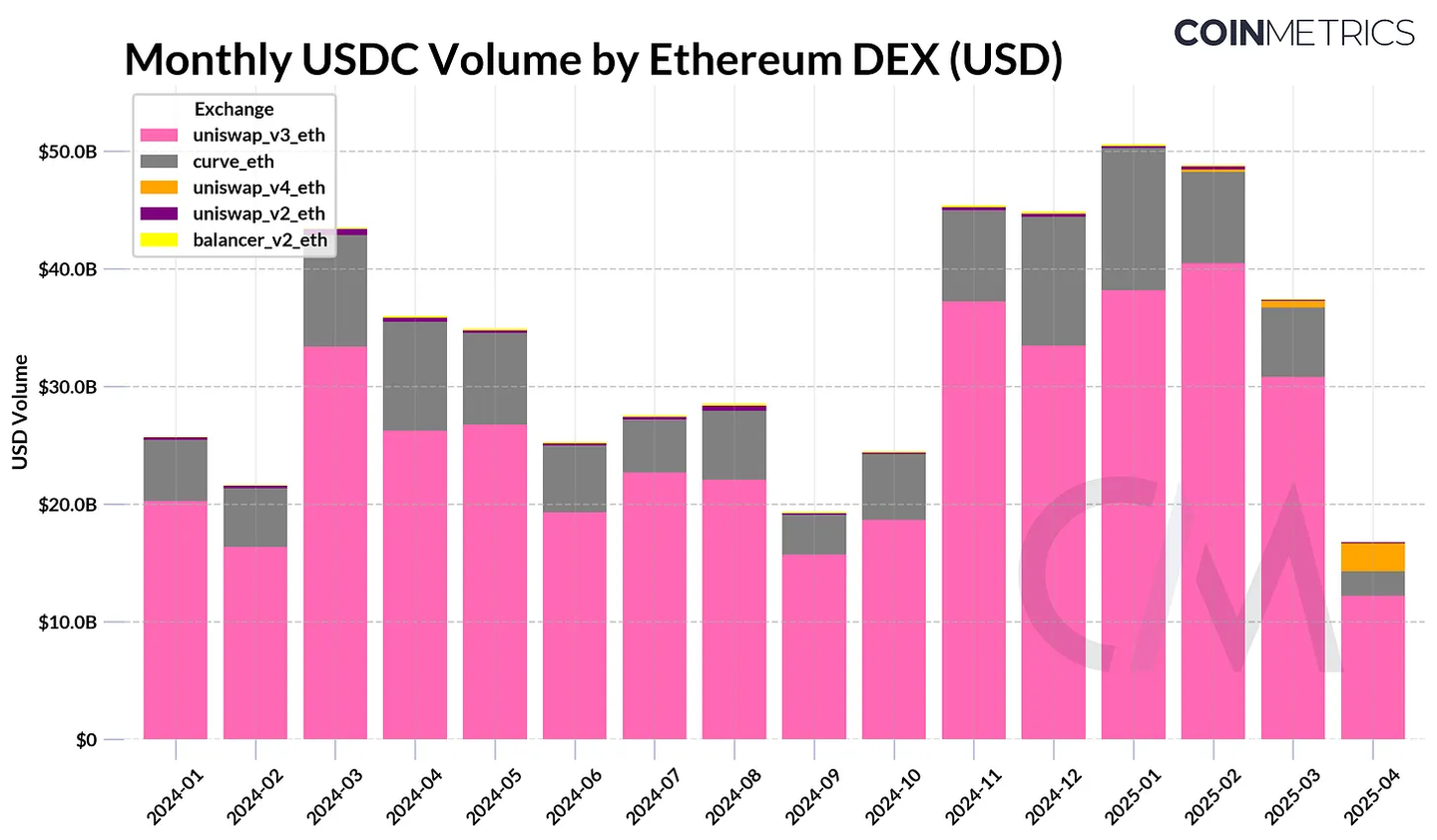

Likewise, USDC is a key source of liquidity for various DEX pools, facilitating the trading of stable value. It also increasingly supports the on-chain foreign exchange market, especially with the rise of other fiat-pegged stablecoins such as Circle’s MiCA-compliant stablecoin EURC.

Source: Coin Metrics DEX Data

in conclusion

USDC's on-chain growth reflects the restoration of market confidence, but Circle's filing also highlights key challenges, especially high distribution costs and heavy reliance on interest income. To maintain momentum in a low-interest environment, Circle aims to diversify its revenue through active product lines such as Circle Mint and by expanding its tokenized asset infrastructure through the acquisition of Hashnote, the largest issuer of tokenized money market funds.

Circle is well-positioned as regulatory clarity improves, particularly the SEC’s stance that stablecoins are not securities. But it now faces increasing competition from overseas issuers like Tether and a new wave of U.S. competitors capitalizing on the momentum of policy changes. While Circle’s valuation has yet to be determined, its IPO will mark the first opportunity for public markets to invest directly in the growth of stablecoin infrastructure.