This month, centralized institutions and decentralized public chain projects and protocols such as BlackRock, Mantra Chain, Ondo, Alchemy Pay, Yala, and Ant Digits have all promoted and experimented with various asset types and protocol infrastructure types in the RWA track.

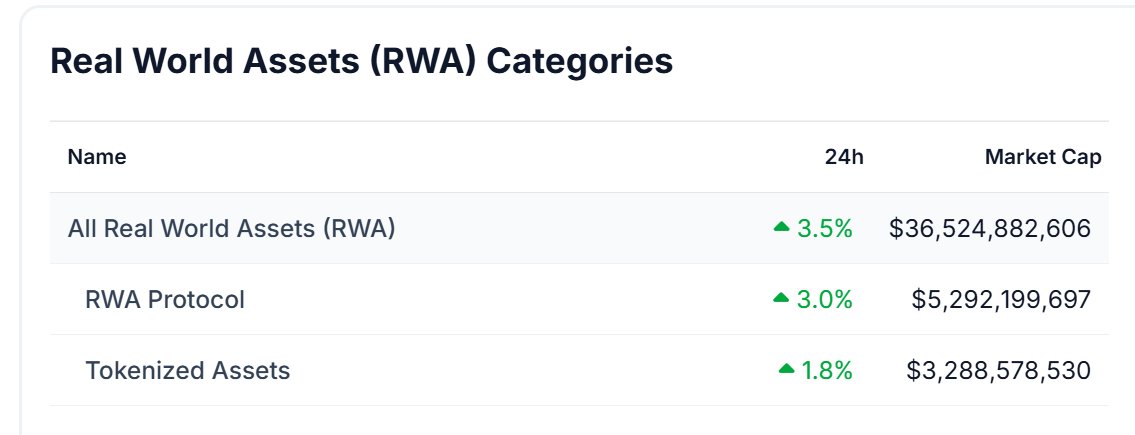

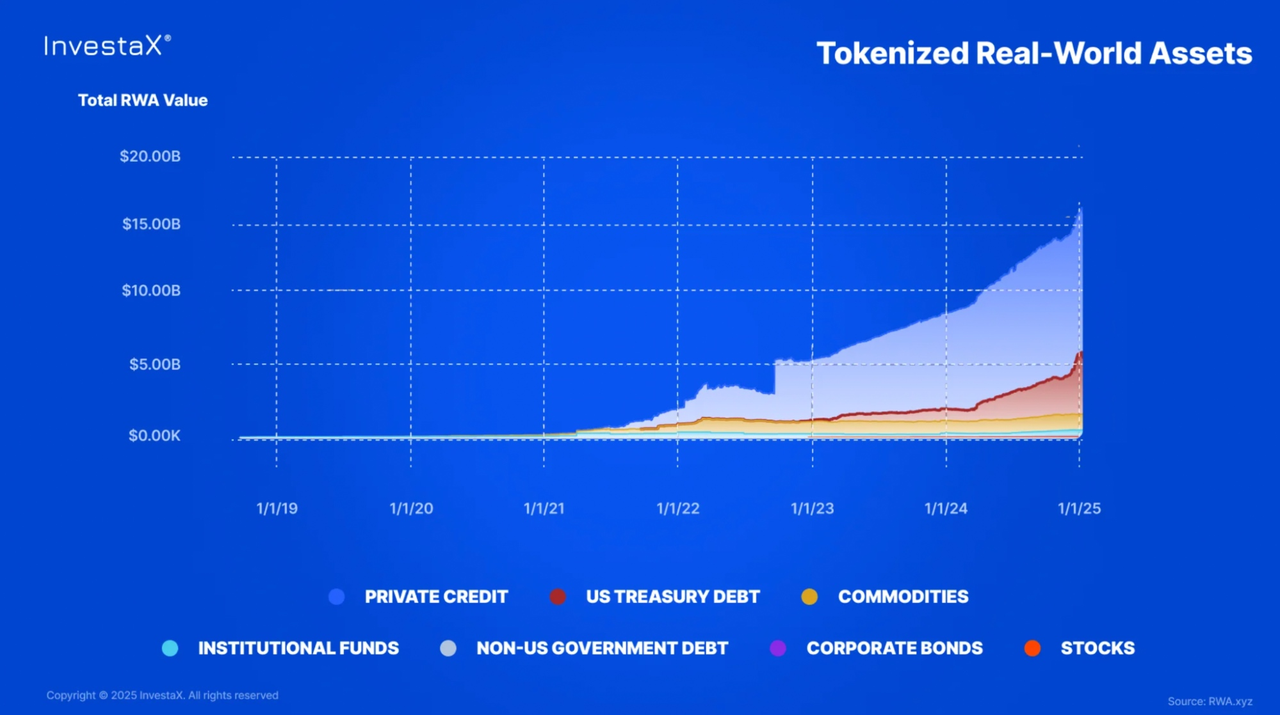

The scale of the RWA track has now reached US$36.5 billion, and the industry growth rate has increased by about 60% year-on-year . The tracks involved mainly include private credit, US bonds, commodities, real estate, stocks and securities, etc., and the main direction of RWA involved in Hong Kong, China is new energy assets as the main category.

Although RWA still has many difficulties and obstacles, as well as compliance and global liquidity issues that need to be resolved, the involvement of traditional financial giants and the accelerated attempts of governments around the world have made it possible for RWA to truly change the hollowing out and scale problems of blockchain finance.

The traditional blockchain world faces the problem of value capture. RWA, as a blockchain financial derivative of the traditional asset world, just makes up for the shortest shortcoming of the blockchain world. Therefore, we believe that RWA is an important bridge between the encryption of traditional finance and the traditionalization of cryptocurrency .

In the Three-Body World, Luo Ji used his own life as a trigger mechanism, deployed nuclear bombs in solar orbit, and used the Dark Forest Law to build a deterrence system against the Three-Body civilization.

In the human world, he is the Sword Bearer of the Earth.

"Dark Forest" is also the nickname for blockchain by most people in the industry, which is also the "original sin" inherent in the decentralized nature.

For some special areas, RWA may be able to act as the sword-bearer of this parallel world .

RWA is in the ascendant. The real goal of RWA is to seamlessly link traditional finance and decentralized finance. While reshaping traditional finance, it can also bring opportunities in the real world to the chain, rather than a bunch of private protocols stored on the public chain. At the same time, we expect RWA to bring us a global and unbounded asset investment method and financial expression method. It is conceivable that we can buy Nasdaq stocks in Hong Kong during the day, deposit money in the Russian Federal Savings Bank in the early morning, and invest in Dubai real estate with hundreds of shareholders in the world who do not know each other's names the next day.

Yes, we believe that RWA can build a world on a public ledger of real assets! A greater world without boundaries!

1. Recent market dynamics and key events

Market-related dynamics

1. Market size trend

As of April 21, 2025, the total market value of the RWA market reached $36.5 billion, up 0.7% in the past 24 hours, showing continued investor interest. The number of RWA-related crypto tokens has exceeded 185, with a total market value of more than $10.62 billion (March 2025 data), up 61% from the previous month.

Traditional financial giants such as BlackRock and Fidelity have begun to pay attention to the RWA field and explore the possibility of asset tokenization through blockchain technology.

Major fund manager BlackRock is seeking regulatory approval for tokenizing its bonds and stocks, while JPMorgan has launched an internal tokenization platform and is actively exploring risk-weighted asset (RWA) opportunities. The rise in market interest bodes well for further growth, with the sector expected to cross the trillion mark in the next five years.

2. Regulatory compliance promotion

Projects such as Mantra Chain have obtained a Virtual Asset Service Provider (VASP) license from the Dubai Virtual Asset Regulatory Authority (VARA), marking a positive development in regulatory compliance for RWA projects, making Mantra Chain the first DeFi platform to receive this license.

Mantra is a Layer-1 blockchain built specifically for RWAs, allowing ecosystem participants to build permissioned applications in a permissionless environment.

This dual model enables regulators to maintain oversight while enabling developers, institutions, and retail investors to take advantage of DeFi. Platforms that adopt this approach will have a unique advantage in meeting global compliance requirements without stifling innovation.

Mantra Chain allows ecosystem participants to develop and use time-sharing risk-weighted assets (RWA).

Recently, Mantra Chain has partnered with Damac, a well-known real estate developer with a diversified portfolio, to tokenize assets worth at least $1 billion in its portfolio and use them for investment through time-sharing ownership .

3. Stellar blockchain cooperation expansion

The Stellar blockchain has announced partnerships with Paxos, Ondo, Etherfuse, and Societe Generale’s SG Forge.

Lauren Thorbjornsen, COO of the Stellar Development Foundation (SDF), said that the Stellar blockchain will facilitate the onboarding of $3 billion in real-world assets by the end of 2025, which would represent a more than 10-fold increase from the $290 million in RWA on the Stellar chain by the end of December 2024.

4. Alchemy Pay products will integrate RWAs

On April 1, crypto payment company Alchemy Pay announced that its products will integrate real-world assets (RWAs). By cooperating with mainstream RWA providers, it will introduce high-quality traditional financial assets such as U.S. Treasuries and blue-chip stocks into the crypto ecosystem, supporting users in multiple regions to purchase with fiat currency.

Alchemy Pay said that the business is committed to building a compliant channel connecting traditional finance and decentralized finance, providing users with diverse investment options, and lowering the participation threshold for global users.

5. Yala RealYield Platform Launched

On April 5, Bitcoin liquidity protocol Yala officially launched an innovative product - Yala RealYield, the first structured yield market platform based on Bitcoin and integrating real-world assets (RWA). It aims to provide users with highly flexible investment autonomy by aggregating diversified RWA providers.

The RealYield platform hopes to allocate BTC liquidity to tokenized high-quality interest-bearing RWAs (such as U.S. Treasuries, private credit, corporate bonds, and real estate mortgage assets), providing Bitcoin holders with an institutional-level stable income channel.

Users can freely choose and combine various interest-bearing assets on the premise that all assets are on-chain.

6. RWA REAL UP Dubai Summit 2025 will be held in Dubai

On April 30, RWA REAL UP Dubai Summit 2025, led by Ant Digits and co-participated by multiple Web3.0 partners including Solana, Sui, ZKsync, Pharos, ChainIDE, Chainlink, ZAN, AAVE, etc., will meet with you in Dubai.

Tracking Technological Innovation Dynamics

1. Quant Network launched Overledger , an interoperable blockchain operating system that supports multi-chain applications. It enhances the liquidity of RWA between different blockchains. The multi-chain approach can achieve liquidity and interoperability of RWA assets between different assets, which can greatly stimulate the issuance of RWA in multi-chain form.

2. Securitize launches sToken Vault feature to enhance the liquidity and composability of RWA, and cooperates with Elixir's "deUSD RWA Institutional Program".

The sToken Vault launched by Securitize is an innovative feature based on ERC-4626 vault technology, which is mainly used to enhance the liquidity and composability of real-world assets (RWA) in decentralized finance (DeFi).

Core role: Allows institutional investors to hold RWA issued by Securitize, while obtaining liquidity in DeFi in the form of deUSD (decentralized US dollar token) and continue to earn returns from the underlying assets.

Cooperation model: This functionality is provided through cooperation with Elixir's "deUSD RWA Institutional Program", with the goal of connecting traditional finance (TradFi) and DeFi.

Currently, BlackRock’s BUIDL token and other assets such as Hamilton Lane’s SCOPE are supported, with plans to expand in the future.

Project financing related news

1. Plume received $20 million in financing to build a real-world asset financial ecosystem.

2. Tether announced its investment in Quantoz, plans to launch a stablecoin that complies with MiCAR regulatory standards, and expand its tokenization capabilities through Hadron by Tether Tech.

Hong Kong and China RWA Development Events

1. Conflux Network and Ant Digital Technologies reach cooperation

Conflux Network and Ant Digital Technologies have partnered to drive the growth of RWA in Hong Kong. The two parties are jointly involved in China's first renewable energy battery swap RWA project, which is located in Hong Kong and uses blockchain technology to build a secure, transparent and compliant digital infrastructure.

2. The Hong Kong Monetary Authority (HKMA) launched the “Digital Bond Grant Program”

The Digital Bond Grant Scheme aims to encourage the adoption of tokenization technology in the capital markets.

In addition, HKMA has launched the “Project Ensemble” sandbox project to support institutions in experimental tokenized applications, including traditional securities and RWAs.

3. 2025 Web3 Festival held in Hong Kong

At this year's Web3 conference, RWA tokenization became a hot topic.

During the meeting, the Hong Kong Monetary Authority’s Project Ensemble initiative was discussed, which aims to explore innovative market infrastructure to support settlement using tokenized currencies and identify practical application cases both domestically and across borders.

The stable regulatory environment and diverse product offerings, including virtual assets and tokenized RWAs, have attracted a large number of investors. However, the participation of retail investors is still limited due to strict requirements.

4. China Pacific Insurance (CPIC)’s tokenized fund

China Pacific Insurance (CPIC) Investment Management Company has launched a tokenized USD money market fund (eStable Money Market Fund, MMF) on HashKey Chain.

The fund raised $100 million on its first day, focusing on short-term fixed-income assets and money market instruments denominated in U.S. dollars. The fund is only for professional and institutional investors, the token issuance platform is PAC, and fund management services are provided by Standard Chartered Bank.

CPIC plans to continue tokenizing more traditional assets using the compliance-driven blockchain platform, indicating that China’s exploration in the RWA space is still ongoing.

2. Industry Observation and Thinking

The main difficulties in the current development of the RWA industry

(1) Regulatory uncertainty

There are significant differences in the laws and regulations on Web3 technology and asset tokenization in different countries and regions, resulting in a lack of a unified regulatory framework. This not only affects the global promotion of RWA, but may also increase compliance costs. Large institutions tend to invest in fiat currencies rather than on-chain assets due to regulatory uncertainty.

European and American countries focus on compliance thresholds. Although Asia and the Middle East have attracted projects through experimental policies, the compliance threshold is still not low. Therefore, the current status of the RWA protocol is that it can exist on the public chain, but it must be supplemented by various compliance modules to adapt to the compliance framework. These compliance protocols cannot interact directly with traditional DeFi protocols. Secondly, based on different jurisdictions, a protocol that complies with the Hong Kong compliance framework cannot interact with compliance protocols in other regions. From the current status quo, the RWA protocol does not have sufficient accessibility and is extremely lacking in interoperability. It is like an "isolated island" and runs counter to the ideal form.

In 2025, some regions such as Dubai have begun to experiment with regulatory frameworks (such as Mantra Chain obtaining a VASP license), but global consistency will still take time.

Different countries and regions now adopt different regulatory frameworks, making it difficult for RWA to circulate globally.

At the end of the article, there is a description and summary of the regulatory framework in different countries and regions.

(2) Barriers to adoption

RWA needs to be accepted and used by a wider user group (including users of different ages and backgrounds). This includes using cryptocurrency as a payment method and overcoming the learning curve of new technologies. At present, the participants and promoters of RWA are mainly institutions. Whether in the United States or Hong Kong, large institutions are the main driving force for implementation. Now the industry standards have not been established, resulting in many retail investors not participating, and ordinary investors are still not aware of RWA.

(3) Sustainability and volatility

The tokenization of RWAs could trigger excessive speculation, leading to unreasonable price fluctuations in otherwise stable assets (such as real estate or bonds), which could in turn lead to market instability and affect long-term investor confidence.

(4) Technical challenges

Smart contract vulnerabilities and blockchain platform scalability issues may affect the security and reliability of RWA. For example, processing a large number of RWA transactions requires efficient infrastructure, and existing technologies may not yet fully meet the needs. Technical risks may lead to asset security issues and weaken investor trust. Quant Network and DECO are developing privacy protection and scalability solutions, but it will take time to verify.

(5) Liquidity issues

Some RWAs (especially less liquid assets such as real estate or art) may still face illiquidity issues after tokenization, especially in poor market conditions. In particular, RWA tokenization tokens in Hong Kong and China, which are mainly institutional, have basically lost liquidity after their first round of financing.

Although standardized assets such as U.S. Treasuries provide a certain starting point for RWA, their on-chainization is more of a technical package and has not released structural value. The key to future RWA is to activate "silent assets" that have long been outside the traditional financial system, difficult to value, and lack liquidity, and to express their value and circulate freely through on-chain, thereby creating new market momentum. This will make RWA an opportunity window for funds willing to take risks and invest, attracting more types of funds to the chain, and achieving a dual qualitative change from the "asset side" to the "fund side."

(6) Investor confidence

Building investor trust is key to the development of RWAs, but deficiencies in transparency, security and regulatory compliance can undermine confidence.

DePINone Labs Observation and Thinking

(1) Centralized pre-chain supervision and decentralized post-chain circulation are the final forms of expression of RWA

Taking Hong Kong as an example, Hong Kong has now established a three-tier coordination mechanism of the Mainland, Hong Kong and Singapore.

The first layer is the domestic title confirmation layer , which conducts data and standardizes processing on the domestic data asset trading platform, completes asset preparation through the sandbox mechanism, and ensures operations such as domestic title confirmation of core data.

The second layer is the offshore issuance layer , where Hong Kong licensed institutions package the processed data assets into compliant fund products and complete private placements based on License No. 9.

The third layer is the global circulation layer . Singapore takes advantage of its RMO license to undertake secondary market circulation and achieves compliant cross-border circulation through the China-Singapore International Data Channel.

The innovative value of this architecture is reflected in three dimensions. First, the domestic links strictly adhere to the bottom line of data security and avoid the regulatory risks of Document No. 38. Second, Hong Kong leverages the professional advantages of licensed institutions and focuses on primary market issuance. Third, Singapore opens up the secondary retail market to activate global capital participation.

(2) Activating the vitality of the RWA secondary market is the beginning of the RWA industry's take-off

Now RWA is facing the primary market phenomenon of "assets becoming silent as soon as they go online". Given that various compliance and regulatory systems have not been implemented, liquidity in the secondary market is difficult to release, which suppresses the market vitality of RWA.

To this end, we believe that the distributed digital identity (DID) system will form an important strategic watershed.

Taking BlackRock’s research as an example, BlackRock clearly positioned DID as the infrastructure for inclusive finance in public documents, attempting to break down the barriers between institutional and retail markets through a verifiable credit system.

The development of RWA should never be limited to the professional investor market. Building underlying capabilities such as digital identity authentication and on-chain clearing will be the most important infrastructure condition for introducing secondary market liquidity.

(3) RWA can both tokenize cryptocurrencies and traditional finance , and also tokenize cryptocurrencies.

The two are moving towards each other, not in opposite directions.

Traditional assets are rushing to blockchain for value release and on-chain flow;

What cryptocurrencies are rushing towards traditional finance is the construction of currency niches and value capture, rather than the memecoins that had no value support in the past.

RWA can truly realize the process of transforming good cryptocurrency into bad cryptocurrency, making the crypto world have real value support rather than a mirage built on the dream of decentralization.

Appendix: Details of the regulatory framework for RWA in major jurisdictions around the world as of April 2025

USA

Regulatory agencies: SEC (Securities and Exchange Commission), CFTC (Commodity Futures Trading Commission)

Core regulations:

- Security tokens: They must pass the Howey Test to determine whether they are securities and are subject to the registration or exemption provisions of the Securities Act of 1933 (such as Reg D, Reg A+).

- Commodity tokens: regulated by the CFTC, Bitcoin, Ethereum, etc. are clearly classified as commodities.

Key measures:

- KYC/AML: BlackRock’s BUIDL fund is only open to accredited investors (net assets ≥ USD 1 million), with mandatory on-chain identity verification (such as Circle Verite).

- Expanded securities recognition: Any RWA that involves dividends may be considered a security. For example: SEC’s penalty against Securitize, a tokenized real estate platform (unregistered securities offering in 2024).

🇭🇰 Hong Kong

Regulatory bodies: HKMA, SFC

Core framework:

- The Securities and Futures Ordinance brings security tokens under regulation and requires them to comply with investor suitability, information disclosure and anti-money laundering requirements.

- Non-security tokens (such as tokenized commodities) are subject to the Anti-Money Laundering Regulations.

Key measures:

- Ensemble Sandbox Program: Testing dual-currency settlement (HKD/offshore RMB) of tokenized bonds and cross-border real estate mortgages (in cooperation with the Bank of Thailand), with participating institutions including HSBC, Standard Chartered, Ant Chain, etc.

- Stablecoin gate policy: Only stablecoins approved by the HKMA (such as HKDG and CNHT) are allowed to be used, and unregistered currencies such as USDT are prohibited.

🇪🇺 European Union

Regulator: ESMA (European Securities and Markets Authority)

Core regulations:

- MiCA (Market Regulation for Crypto-Assets): effective in 2025, it requires RWA issuers to set up an EU entity, submit a white paper and be audited.

- Token classification: Asset Reference Tokens (ARTs), Electronic Money Tokens (EMTs), and other crypto assets.

Key measures:

- Liquidity restrictions: Secondary market transactions require a license, and DeFi platforms may be defined as “virtual asset service providers” (VASPs).

- Compliance shortcuts: Luxembourg fund structures (such as Tokeny gold tokens) become a low-cost issuance channel, and the compliance costs of small RWA platforms are expected to increase by 200%.

🇦🇪 Dubai

Regulator: DFSA (Dubai Financial Services Authority)

Core framework:

- Tokenization Sandbox (launched in March 2025): divided into two phases (intention application, ITL test group), allowing testing of security tokens (stocks, bonds) and derivative tokens.

- Compliance path: Exemption from some capital and risk control requirements, and the ability to apply for a formal license after a testing period of 6-12 months.

Advantages: Equivalent to EU regulation, supports distributed ledger technology (DLT) applications, and reduces financing costs.

🇸🇬 Singapore

- Security tokens are included in the Securities and Futures Act and are subject to exemptions (small issuance ≤ 5 million Singapore dollars, private placement ≤ 50 people).

- Utility tokens must comply with anti-money laundering regulations, and MAS (Monetary Authority of Singapore) promotes pilot projects through sandboxes.

🇦🇺 Australia

- ASIC (Securities and Investments Commission) classifies RWA tokens that confer income rights as financial products, requiring a financial services license (AFSL) and risk disclosure.