By Stacy Muur

Compiled by: Tim, PANews

Over the past 15 months, the DeFi liquidity landscape has been reshaped across chains, with projects driven by hype gradually exiting the stage and liquidity quietly concentrated in places where fundamentals are strong rather than driven by market hype.

Key insights

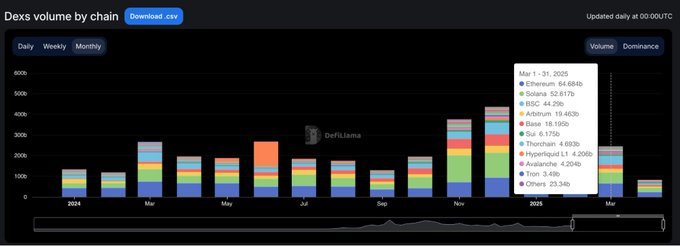

- After DEX trading volume hit an all-time high of $380 billion in January 2025, it fell 35% in the following two months, which suggests that January may have formed a short-term top.

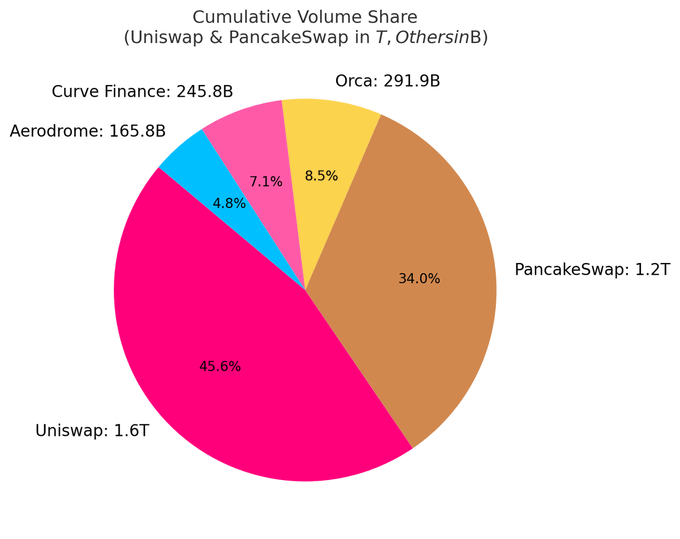

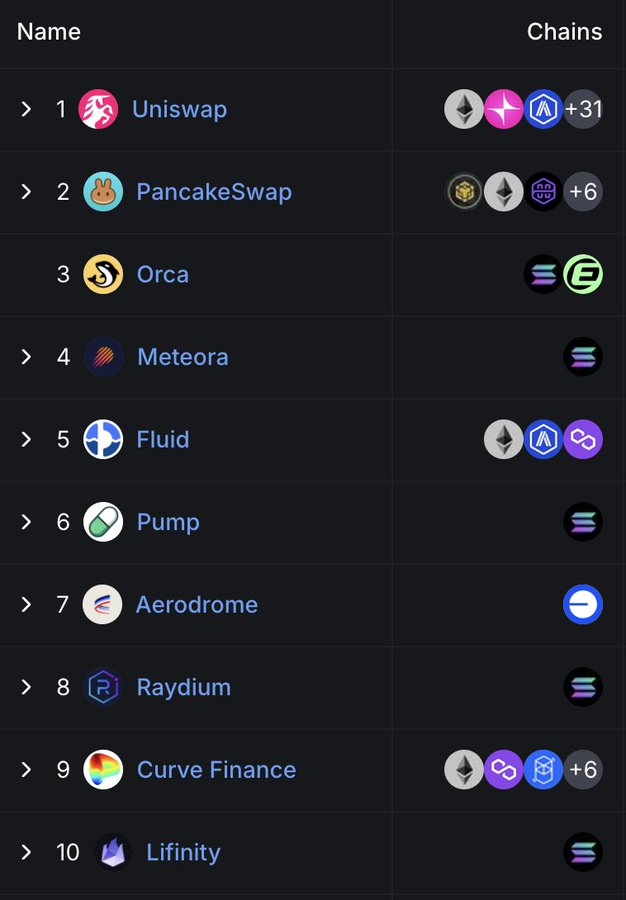

- Currently, the top ten DEXs account for nearly 80% of the total trading volume; Uniswap and PancakeSwap alone account for about 40% of the share.

- Solana-based DEXs have quietly dominated the rankings, occupying 5 of the top 10 spots, with their market share growth driven primarily by trading volume from the meme coin craze.

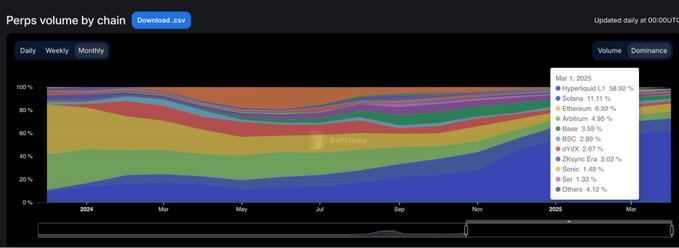

- Hyperliquid has completely changed the landscape of perpetual contracts, rising from a newcomer in the industry to occupying more than 60% of the market share by March 2025.

All insights in this article are based on public data. Special thanks to DefiLlama for continuing to provide high-quality statistics.

Cycles defined by surges and slowdowns

At the beginning of 2024, DEX trading volume was strong in March and May, then gradually slowed down until mid-year.

The situation changed dramatically in the fourth quarter, with trading volumes surging in November and December, a trend that continued until January 2025, when it reached an explosive peak of $380 billion.

However, the rebound was short-lived. By February, market volume had plummeted to $245 billion, a 35% drop that ended a three-month vertical surge. The pullback set the tone for a more cautious second quarter.

DEX dominance: Top protocols take the reins

The DEX market landscape remains highly concentrated. Currently, the top ten protocols account for 79.5% of daily trading volume, while the top five alone account for 59.1%.

Uniswap and PancakeSwap account for about 40% of DEX trading volume and are the only two platforms with cumulative trading volume exceeding one trillion US dollars so far. Their leading position stems from first-mover advantage, extensive support for multi-chain ecology, and deep liquidity.

Uniswap Labs also launched Unichain, a second-layer network on Ethereum built on the Optimism Superchain. The chain aims to enable fast and low-cost transactions through native multi-chain interoperability.

The Quiet Rise of Solana

It is noteworthy that Solana is becoming increasingly prominent in the DEX field. Five of the top ten DEXs, including Orca, Meteora, Raydium, Lifinity, and Pump.fun, are natively developed based on Solana.

Orca (8.02%) and Meteora (6.70%) alone account for approximately 15% of global DEX activity.

This growth is due to low gas fees, fast block times, and the Solana meme coin craze. Pump.fun’s surge into the top 10 is a testament to this enthusiasm.

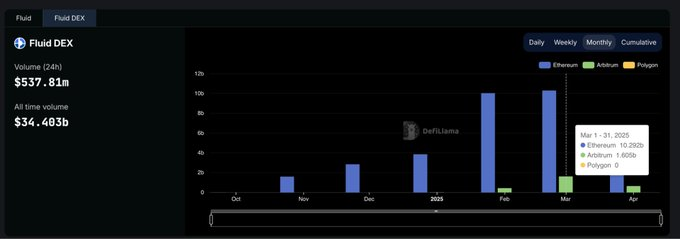

Emerging protocols: Fluid and Aerodrome

Fluid (7.09%) is the most capital efficient platform among the top five DEXs. The protocol is active on Ethereum, with monthly liquidations exceeding $10 billion. It has been particularly impressive since the launch of the Arbitrum ecosystem: trading volume surged from $426 million in February to $1.6 billion in March, fully demonstrating that its adoption rate is far faster than the industry average.

As a native project of Base, Aerodrome demonstrates the continued growth of liquidity on Base L2.

Although Hyperliquid is not ranked high in the spot market, it dominates the perpetual contract market with a market share of over 60%.

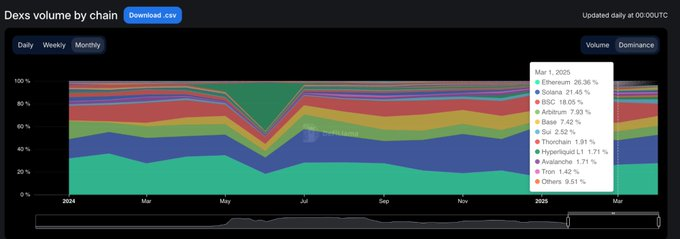

Market share of DEX chains: easy to grow, difficult to retain

The past 15 months have clearly shown a phenomenon: most blockchain projects can attract attention, but only a few can maintain their appeal. From January 2024 to March 2025, the market share of chain-level decentralized exchanges changed rapidly, and only a few projects really had user stickiness.

Solana achieved the biggest breakthrough. It climbed steadily in 2024, driven by the TRUMP and MELANIA meme coin craze, and reached a peak market share of 45.8% in January 2025. But by March, its market share was halved to 21.5%, but it still ranked first among all public chains with an average share of 25.1%.

Ethereum is the exact opposite. It starts 2024 with a share of about 32%, falls to 15.3% in January 2025, and then rebounds to 26.4% in March. Of course, even if Ethereum loses its growth momentum, its ecological resilience remains.

Base is the most stable follower. It continued to grow from 3% in March 2024 to 12.4% in December, and then fell back to 7.4% in March 2025, maintaining an average share of 6.6% during the period. There is no hype, only slow but sticky growth.

BNB Chain remained stable with an average share of 14.7%. There was no sharp rise or fall, and the flow of retail funds was always stable.

Arbitrum had a strong start (16% share) but subsequently lost momentum, and by January 2025 it had fallen to 4.8%, surpassed by both Base and Solana.

Blast reached a peak market share of 42.3% in June 2024, but disappeared the following month. This is a typical case of incentive-driven transaction volume and zero user retention rate.

Summary: The dominance of DEX in each public chain is highly volatile. Solana once emerged, Ethereum achieved value restoration, Base gradually expanded its ecosystem, and the market hype cycle showed ups and downs. The public chain that ultimately occupies a dominant position is not the one with the loudest voice, but the network with the highest actual usage rate.

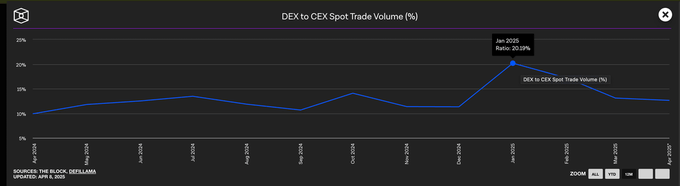

Centralized exchanges still dominate spot trading volume

Despite the explosive growth of DEXs in early 2025, centralized exchanges still dominate the spot market. Even in January, when DEX trading volume peaked, CEXs still accounted for nearly 80% of total trading volume.

While the dominance of centralized exchanges has fallen from 90% at the beginning of 2024 to a low of 79%, the broader trend is clear: while DEXs continue to grow, CEXs remain the default choice for most traders.

Perpetual Protocol Market Share

The landscape of on-chain perpetual contracts has undergone a fundamental shift in 2024.

More than two years after dYdX took the top spot in perpetual contract trading, Hyperliquid emerged and redefined what dominance means. The platform first topped the list in February, but was briefly surpassed by SynFutures in the middle of the year. After regaining the top spot in August, it has been far ahead. As of March 2025, Hyperliquid has accounted for nearly 59% of the total perpetual contract trading volume, completely consolidating its position as the preferred platform for professional traders.

This rising momentum has attracted a lot of market attention, and its product experience is closer to centralized exchanges than any previous decentralized exchanges. In contrast, dYdX's market share has declined rapidly. From 13.2% of the market share at the beginning of 2024, it has plummeted to only 2.7% in March 2025, and users have turned to faster, simpler, and more modern alternative platforms.

Jupiter's perpetual contract took a different approach. With Solana's native liquidity and the diversion effect of its spot DEX, it climbed to the second place with a market share of 8.8%. Although it rose rapidly, it lacked stamina and eventually ranked behind Hyperliquid. Other projects such as SynFutures, Vertex Protocol and Paradex also briefly emerged.

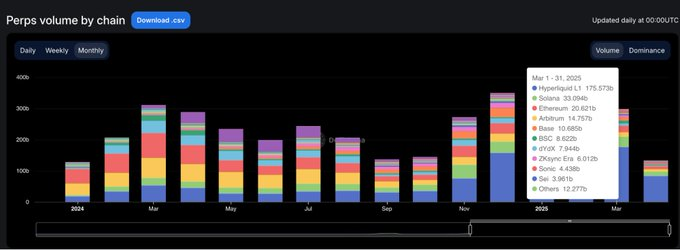

Perpetual Contract Chain: The execution layer is reconstructed within one cycle

The biggest shift in perpetual swap infrastructure over the past year has not been about which protocols users prefer, but rather which chains they trust to execute transactions.

By March 2025, Ethereum and Arbitrum’s share of perpetual contract trading volume had plummeted to 11.8%, in stark contrast to their combined market dominance of over 65% in January 2024, as newer, faster execution layers took over.

The core force driving this transformation is Hyperliquid's self-developed blockchain. The chain has significantly increased its market share from 13.6% to 58.9% during the same period. In less than a year, it has replaced various Layer 1 and Layer 2 solutions that once defined industry standards and become the default execution environment for perpetual contract transactions. Its advantages are not only reflected in faster transaction speeds, but more importantly, it provides the reliability and low latency required by professional traders.

Solana also experienced a strong rise. Driven by the Jupiter and Phoenix projects at the end of 2024, its market share once climbed to nearly 16%. But it eventually stabilized in the 10-11% range and failed to continue its breakthrough growth momentum. Although the Base and ZKsync ecosystems showed vitality (the peak market share reached 6-7%), they have never been able to rank among the top public chains.

Meanwhile, Blast has become a cautionary tale: this short-lived project reached 18.8% market share in June 2024, but disappeared at the same alarming speed. In a field driven by product quality and user retention, pure hype will not last long. The new industry execution standard has been clarified: performance-centric public chains have redefined the competitive benchmark, and traditional infrastructure no longer occupies a default advantage.

The future of DeFi does not lie in multi-chain expansion, but in protocols that can transform industry narratives into user habits.