From BlackRock’s entry, to Robinhood’s self-developed public chain, to Nasdaq’s layout of stock tokenization, the narrative of real-world assets (RWA) has long been a foregone conclusion. However, we must be soberly aware that moving stocks and bonds onto the chain is only the first domino in this grand transformation.

The real disruption is not what we can "buy" on the chain, but what new species and new gameplay we can "create" based on these assets that carry real-world value.

This article aims to further explore what the next stop for RWA is after tokenization, and why it is expected to usher in a DeFi Summer-level narrative and innovation.

Tokenization is just the beginning

In essence, moving RWA assets such as US stocks and gold to the chain only completes the "digital packaging" of assets and solves the problems of asset issuance and cross-regional circulation, but is far from releasing their true potential.

Imagine a tokenized asset that can only circulate in a wallet and cannot be used in combination. This loses the composability advantage of the blockchain. After all, in theory, the introduction of RWA can greatly improve asset liquidity and release new value through DeFi operations such as lending and staking.

Therefore, it should have injected high-quality assets with real returns into DeFi and enhanced the value foundation of the entire Crypto market. This is a bit like ETH before DeFi Summer. At that time, it could not be lent, could not be used as collateral, and could not participate in DeFi. It was not until protocols such as Aave gave it functions such as "mortgage lending" that it released hundreds of billions of liquidity.

If U.S. stock tokens want to break through the dilemma, they must replicate this logic and make the deposited tokens "live assets that can be mortgaged, traded, and combined."

For example, users can use TSLA.M to short BTC and use AMZNX to bet on the trend of ETH. Then these deposited assets are no longer just "token shells", but margin assets that are used. Liquidity will naturally grow from these real trading needs.

This is exactly what the move from RWA to RWAFi means. However, to truly unlock value, we need more than just a single technological breakthrough; we need a systematic solution that covers:

- Infrastructure layer: secure asset custody, efficient cross-chain settlement and on-chain liquidation;

- Protocol layer: standardized tools that facilitate rapid integration between developers and asset owners;

- Ecological layer: Deep linkage and cooperation of various DeFi protocols such as liquidity, derivatives, lending, and stablecoins;

This reveals that putting RWA on the chain is not only a technical issue, but also a systemic issue. Only by introducing RWA safely and with low barriers to entry into diverse DeFi scenarios can the stock dividends of traditional assets be truly transformed into incremental value on the chain.

02. Bringing Real Assets to Life: The Financialization Path of RWA

So where are we stuck now?

The biggest problem in the current RWA token market is no longer the "lack of targets" but the "lack of liquidity structure."

First, there is the lack of financial composability.

In the traditional U.S. stock market, the reason for abundant liquidity does not lie in the spot market itself, but in the trading depth constructed by derivative systems such as options and futures. These tools support price discovery, risk management and capital leverage, create long-short games and diversified strategies, and attract institutional funds to continue to enter the market, ultimately forming a positive cycle of "active trading → deeper market → more users".

But the problem is that the current US stock tokenization market lacks this crucial layer of structure: most of the TSLA and AAPL tokens purchased by users can only be "held" but cannot be truly "used". They can neither be used as collateral to borrow stablecoins in Aave, nor as margin to trade other assets in dYdX, let alone build cross-market arbitrage strategies based on them.

Therefore, although these RWA assets have come to the chain, they are not yet "alive" in the financial sense, their capital efficiency is far from being released, and the road to the vast DeFi world is blocked.

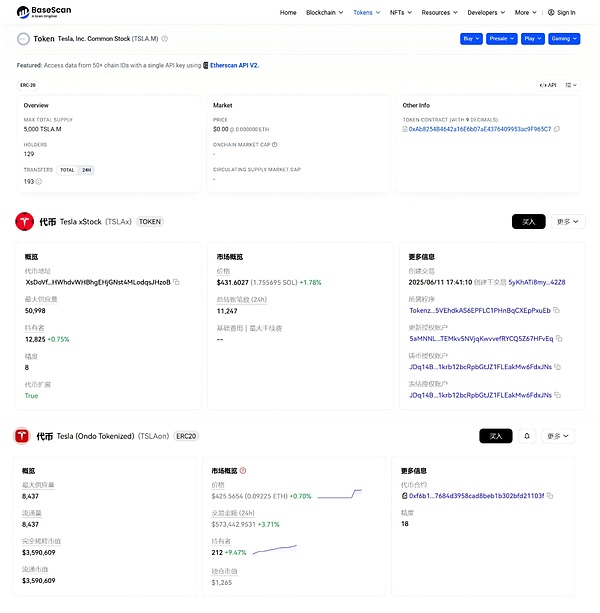

Note: TSLA.M of MyStonks, TSLAx of xStocks, and TSLAon of Ondo Finance

Secondly, there is the fragmentation and fragmentation of liquidity.

This is also a more difficult problem. Different issuers have launched independent and incompatible token versions based on the same underlying assets (such as Tesla stock), such as MyStonks' TSLA.M, xStocks' TSLAx, and Ondo Finance's TSLAon.

This situation of "multiple issuances" can't help but remind people of the early difficulties of Ethereum's Layer2 ecosystem - liquidity was fragmented into isolated islands and could not be gathered into an ocean. This not only greatly diluted the market depth, but also brought huge obstacles to user and protocol integration, seriously hindering the large-scale development of the RWA ecosystem.

03. How to complete the missing puzzle pieces?

How to solve the above dilemma?

The answer lies in building a unified and open RWAFi ecosystem, transforming RWA from a "static asset" into a composable and derivative "dynamic Lego building block."

Therefore, Nasdaq's latest developments are particularly worthy of attention. Once top traditional institutions like Nasdaq enter the market and issue official stock tokens, it will fundamentally solve the trust issue at the source of assets. Then, within the RWAFi framework, a unified RWA asset can be "financialized" in various ways - through mortgage, lending, pledging, income aggregation and other operations, it will not only generate cash flow but also introduce real-world value anchoring to the chain.

What’s important is that this kind of financialization is not limited to highly liquid assets such as U.S. stocks and U.S. bonds. Even fixed assets with extremely poor liquidity and composability in the real world can be “activated.”

We can use an example to illustrate its potential. Take real estate, an asset with extremely poor liquidity in the real world. Once it is standardized and introduced into the RWAFi framework, it is no longer just "real estate" but becomes a highly dynamic financial component:

- Participate in lending: Use it as high-quality collateral to obtain low-interest financing on the chain and activate dormant capital;

- Automated revenue generation: Through smart contracts, monthly rental income is automatically and transparently distributed to each token holder in the form of stablecoins.

- Build structured products: Separate the property's "value-added rights" from its "rental income rights" and package them into two different financial products to meet the needs of investors with different risk preferences;

This "dynamic empowerment" actually breaks the inherent limitations of RWA and injects it with the higher-dimensional composability native to DeFi. Therefore, Nasdaq's stock tokenization is just the first domino. Once they taste the sweetness of US stock tokens, all kinds of assets, from real estate to commodities, will usher in a wave of on-chainization.

Therefore, the real outbreak point in the future will not be these assets themselves, but the derivative ecosystem built around them - mortgage, lending, structuring, options, ETFs, stablecoins, income certificates... All these DeFi modules we are familiar with will be recombined and nested on the standardized RWA to form a new "Real Return Finance (RWAFi)" system.

If the DeFi Summer of 2020 was a "currency Lego" experiment centered around crypto-native assets such as ETH and WBTC, then the next wave of innovation initiated by RWAFi will be a larger and more imaginative "asset Lego" game based on the entire real-world value.

When RWA is no longer just an asset on the chain, but becomes the underlying building block of on-chain finance, a new round of DeFi Summer may also start from here.