By Lacie Zhang, Researcher at Bitget Wallet

Introduction: On August 7, 2025, Eastern Time, an executive order from the White House could become another historic moment in the crypto market, following the Bitcoin spot ETF. US President Trump signed an executive order directing the Department of Labor to revise its rules to formally include alternative assets such as cryptocurrencies, real estate, and private equity as investment options in 401(k) retirement plans .

This not only concerns the $8.7 trillion in American life savings, but also potentially paves an unprecedented regulatory highway for the second wave of institutional capital inflow. With the retirement accounts of tens of millions of Americans directly linked to crypto assets, a profound transformation is brewing.

Next, let’s join Bitget Wallet Research Institute to explore this transformation.

1. The $8.7 Trillion “Golden Key”: Why is 401(k) the key variable?

To understand the power of this transformation, we first need to understand the central role of the 401(k) in the U.S. pension system. The U.S. pension system is like a three-legged golden tripod, supporting the retirement lives of its citizens:

| The United States currently has a three-pillar pension system: government + employer + individual | |||

| project | Government social security | Employer-sponsored plans (401(k), etc.) | Individual retirement plans (IRA, etc.) |

| nature | Government-run public pension insurance | Employer-provided retirement savings plans | Individually opened retirement investment accounts |

| How to participate | Mandatory, eligible employees must participate | Voluntariness | Voluntariness |

| Funding | Payroll taxes (paid jointly by employees and employers) | Employee pre-tax contributions, matched by employers | Personal funds deposit |

| Fund Management | Unified government management | Individually managed accounts | Individually managed accounts |

| Investment Options | No personal choice | Limited investment options provided by employers | Individuals are free to choose their investments |

| Early withdrawal | Not allowed | Allowed, but subject to a 10% fine | Allowed, but subject to a 10% fine |

| Amount | $8.9 trillion | $12.2 trillion | $16.8 trillion |

Source: Fintax. This does not take into account insurance companies’ corporate annuity reserves and private sector fixed income protection.

- The first pillar: government-led social security, which is similar to China’s basic pension insurance and is compulsory, but individuals do not have investment options.

- The second pillar is employer-sponsored retirement plans, of which the 401(k) is the backbone. Jointly funded by employees and employers, 401(k)s offer broad coverage and a stable cash flow, making them a core tool for the American middle class to accumulate retirement wealth. While investment options are predetermined by the employer, they offer broad coverage and a stable cash flow.

- The third pillar: Individual Retirement Accounts (IRA), which are opened and managed entirely voluntarily by individuals, giving individuals great investment freedom. It is more like an "open professional market" that requires participants to actively research and make their own decisions.

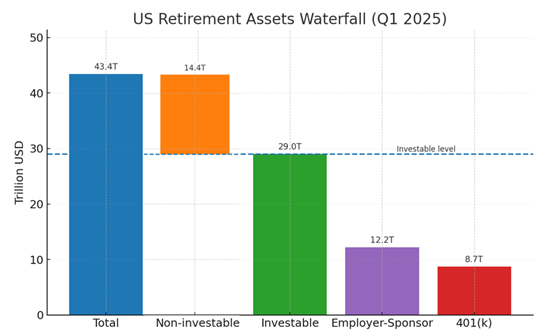

According to data from the Investment Company Institute (ICI) in the first quarter of 2025, the total size of the US pension market reached $43.4 trillion. Within this vast ocean of funds, approximately $29 trillion is actually available for individual investment decisions. Of this $29 trillion, 401(k) plans alone account for $8.7 trillion, or 30% . This massive amount of funds is the very "gold mine" targeted by the new policy.

U.S. 401(k) account balances by age group (as of 2024)

| Age group | Average 401(k) balance | Median 401(k) balance |

| Under 25 years old | $6,899 | $1,948 |

| 25 to 34 years old | $42,640 | $16,255 |

| 35 to 44 years old | $103,552 | $39,958 |

| 45 to 54 years old | $188,643 | $67,796 |

| 55 to 64 years old | $271,320 | $95,642 |

| 65 years and above | $299,442 | $95,425 |

Data source: Vanguard Group, "How America Saves 2024"

Vanguard's 2024 report paints a national portrait of 401(k)s: the average account balance for all participants has reached $148,153. Particularly noteworthy is that account balances rise exponentially with age, reaching nearly $300,000 for those over 65. This suggests that 401(k)s are not only massive in size, but also comprise the middle-aged and older segments of the American population with the highest purchasing power.

Previously, this huge amount of money has been strictly restricted to traditional stocks, bonds, and mutual funds. Now, the Trump administration intends to give it a "golden key" that can open the door to the crypto world.

2. Leveraging the triple wave of the future: How will the new policy reshape the crypto market landscape?

The impact of including cryptocurrencies in the 401(k) investment scope is not simply an inflow of funds, but a structural change that involves three levels: users, institutions, and regulators.

1. The First Wave: A "National-Level" Breakthrough in User Mindsets

One of the biggest challenges for the crypto industry has always been reaching the mainstream: how to convince the mainstream public, especially those middle-aged and older investors with significant capital but conservative mindsets, to accept and allocate crypto assets. This reform can be described as a top-down, national-level market education.

Imagine a 55-year-old American employee seeing a "crypto asset allocation fund" listed alongside an "S&P 500 Index Fund" and a "U.S. Treasury Bond Fund" on the 401(k) investment menu offered by Fidelity or Vanguard. Their perspective would undergo a dramatic shift. This is no longer a distant, high-risk speculative code on social media, but a compliant retirement investment product approved by the U.S. Department of Labor, packaged by a top asset management firm, and accepted by their employer. The dual backing of national sovereign credit and top financial institutions will significantly alleviate ordinary people's skepticism and resistance to crypto assets , achieving the lowest-cost, most widespread user development.

2. The second wave: the continuous flow of institutional capital

If the approval of a Bitcoin spot ETF opens the door to active investment for institutional capital, then the inclusion of 401(k)s opens a continuous "automated water pipeline." ETF capital flows, largely dependent on investor decisions and market sentiment, can fluctuate wildly and then stagnate. However, the 401(k) funding model is fundamentally different: it is directly tied to the vast U.S. national payroll system . This means that every payday, a portion of millions of salaries is automatically allocated to their chosen crypto portfolios, virtually without the holder's knowledge. This stable and substantial incremental capital will provide the market with unprecedented depth and resilience.

This certainty will ignite a new round of product "arms race" among Wall Street giants. Institutions like Vanguard and Fidelity will no longer be content with single crypto products. Instead, they will turn to more diversified, structured, and risk-controlled "401(k) customized" crypto funds. For example, a "basket" index fund might include Bitcoin and Ethereum, supplemented by some blue-chip DeFi tokens , or a "hybrid allocation fund" that combines crypto assets with traditional stocks and bonds to smooth volatility . This will not only enrich the channels for capital entry but also strongly promote the maturity and standardization of the entire crypto asset management industry.

3. The Third Wave: A Trans-Party "Political Moat"

However, the most far-reaching step of this new policy may be hidden beneath the hustle and bustle of the financial markets - it aims to build a "political moat" that can transcend partisan disputes for the turbulent world of crypto.

The policy uncertainty brought about by the alternation between the two political parties in the United States has always been a "Sword of Damocles" hanging over the crypto industry, causing great concerns for any long-term investor. The vacillating regulatory stances between Democrats and Republicans, and even the policy differences between leaders within the same party, have made the long-term development of the industry full of uncertainty. The ingenuity of the new 401(k) policy lies in its deep connection between crypto assets and the "livelihood savings" of tens of millions of American voters . This has fundamentally changed the nature of the game: crypto assets are no longer the exclusive domain of Wall Street and tech geeks, but have become a "common cheese" that every ordinary household cannot ignore.

Imagine the implementation of the new policy: Any future administration attempting to harshly suppress or even overturn existing crypto policies will face immense political pressure, as any move to weaken the crypto market could be directly interpreted by voters as "touching my retirement funds," triggering a fierce political backlash. This blatant conflict of interests elevates the protection of the crypto market from a personal or partisan act by Trump to a "forced choice" for candidates to win over voters and for those in power to protect public property. Thus, a solid moat has been formed, forcing both parties to seek a more stable consensus on crypto regulation, freeing the entire industry from the fate of violent fluctuations caused by party changes and truly cementing "crypto-friendliness" into the long-term financial agenda of the United States.

3. Vision and Reflection: Opportunities and Challenges in the Trillion-Dollar Blue Ocean

We have reason to be optimistic about this new policy. Just as the approval of a Bitcoin spot ETF propelled Bitcoin past the $100,000 mark within a year, the rapid development of compliant products will inevitably trigger a revaluation of the underlying assets. Even assuming only 5% of 401(k) funds (approximately $400 billion) initially flows into the crypto market, this is still a massive amount of capital for the current crypto industry, not to mention the enormous multiplier effect it will have on user development and regulatory oversight.

In the long term, if individually managed pension funds can all invest in crypto assets , then is it possible that the larger social security fund, held by the government, could also open up a crack in the future? This would be a reconstruction of the entire social wealth and financial system.

However, optimism cannot replace reflection, and we must remain cautious, as core challenges remain:

- Will investors buy in? Currently, more than 60% of 401(k) assets are still concentrated in traditional mutual funds. It will take time and market verification for Americans, accustomed to decades of investment patterns, to invest their retirement funds in a highly volatile emerging market.

- How can risks be managed? The dramatic cyclical fluctuations of crypto assets are a natural enemy of retirement savings. How the Department of Labor, asset management institutions, and employers will determine investment ratios and provide risk warnings to protect investor interests—these details will determine the success or failure of this policy.

- What form does the product take? The scope of investment determines the breadth of risk—whether to stick with Bitcoin and Ethereum or open up to the broader token market. Product design determines the depth of risk—how to smooth out volatility to protect investors remains a key unresolved issue.

IV. Conclusion

The Trump administration's executive order is more of a starting gun than a final answer. Using the $8.7 trillion 401(k) fund as a fulcrum, it aims to leverage not only the vast US pension system but also the future of global crypto finance. The road ahead holds vast opportunities, but also uncharted waters. Regardless, as pension funds, the most traditional and conservative of capital, begin to seriously examine the crypto world, the door to a new era is slowly opening.