Preface

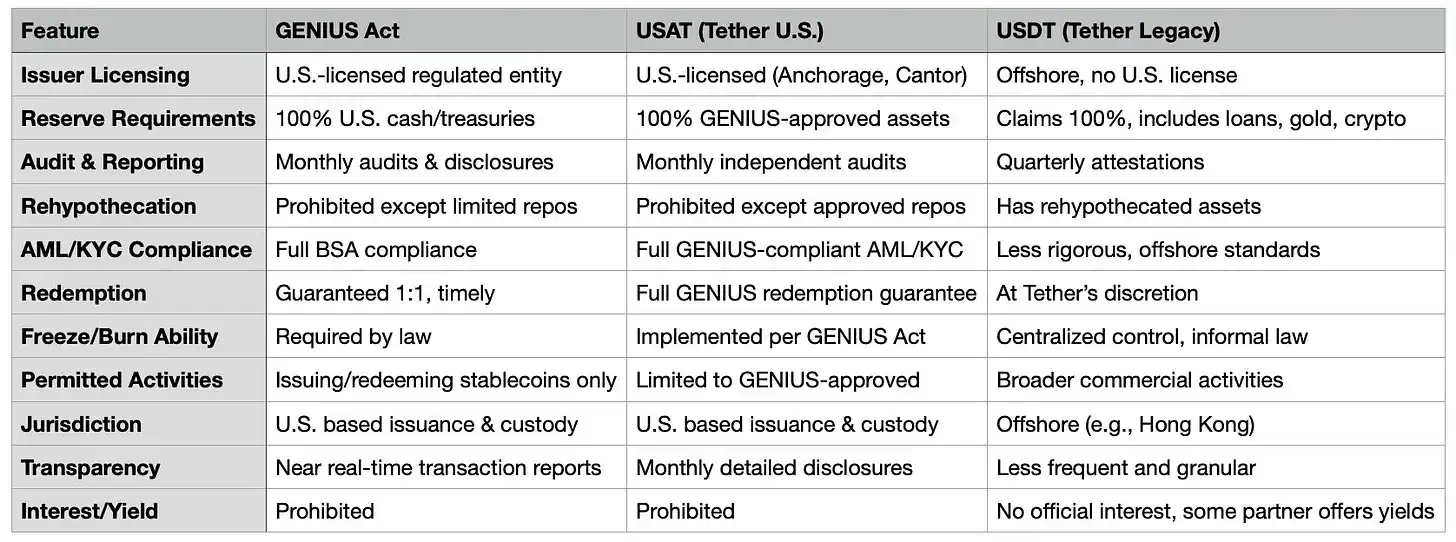

In August, Bo Hines resigned from his position on the White House cryptocurrency commission and quickly became CEO of Tether's newly formed US division. His mission is to launch USAT, a GENIUS Act-compliant stablecoin. USAT will be subject to monthly audits, held entirely in cash and short-term U.S. Treasury bills, and operate under the full supervision of federal banks.

Meanwhile, USDT continues to process over $1 trillion in transactions per month, with its reserves consisting of Bitcoin, gold, and collateralized loans. These assets are managed through offshore entities that have never been fully audited.

Same company, two completely different product approaches.

Tether generated $13.7 billion in profits last year thanks to its "seek forgiveness, not permission" model. Circle, by contrast, went public with a $7 billion valuation thanks to its commitment to due diligence and asking the right questions before moving forward.

The announcement should have been a celebration.

After years of regulatory battles, transparency issues, and persistent questions about the backing of its reserves, Tether is finally offering the U.S. market what critics have long demanded: full compliance, independent audits, a regulated custodian, and reserves held only in cash and short-term U.S. Treasuries.

Yet we find ourselves discussing regulatory arbitrage, competitive moats, and those delightfully awkward moments when revolutionary technologies collide with the established order, while everyone pretends it was all part of the plan all along.

It turns out that with enough creativity in your corporate structure, you can serve two masters at once.

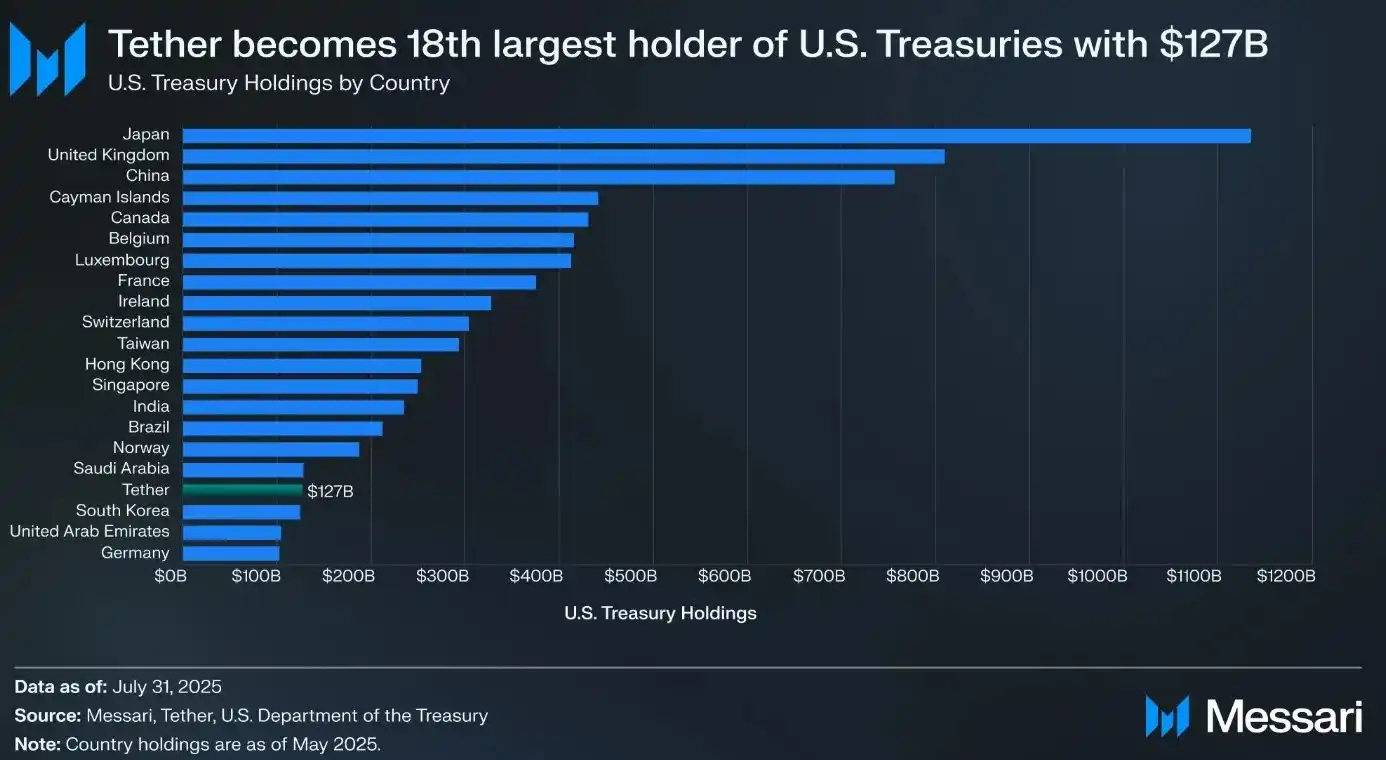

Before delving into USAT, let's first understand Tether's remarkable achievements with USDT. USDT has a circulating value of $172 billion and processes over $1 trillion in cryptocurrency transactions each month. If Tether were a country, it would be the 18th largest holder of U.S. government bonds, holding $127 billion in government bonds.

The company earned $13.7 billion in profits last year—not revenue, but profit—making it one of the most profitable companies, surpassing many Fortune 500 companies.

All of this has been accomplished without the full audits, comprehensive oversight, or transparency that traditional financial institutions are accustomed to. Instead, Tether relies on quarterly “attestations” rather than comprehensive audits and includes assets like gold, Bitcoin, and collateralized loans in its reserves—assets that would be prohibited under strict stablecoin regulations. Furthermore, it primarily operates through offshore entities in Hong Kong and the British Virgin Islands.

This is the ultimate example of how sometimes great things can be achieved by going completely against the regulators' preferences.

The Emergence (and Problems) of the GENIUS Act

Then, in July 2025, the GENIUS Act, the first comprehensive stablecoin regulation in the United States, was introduced. Suddenly, the US market—the most profitable and influential crypto market in the world—had new, strict rules:

100% of reserves are in cash and short-term US Treasury bills (no Bitcoin, gold, or secured loans)

Monthly independent audits, with certification from the CEO and CFO

· Issuer holding a US license and custodian regulated by the US

Fully compliant with Anti-Money Laundering (AML)/Know Your Customer (KYC) requirements, with freezing capabilities

No interest is paid to holders

Full transparency of reserve composition

Looking at this list alongside USDT's existing structure, the challenges are clear. The law effectively draws a clear line between "foreign" and domestically-owned stablecoins. USDT, issued by Tether entities in the British Virgin Islands and Hong Kong, can't simply flip a switch and become compliant. This requires a complete overhaul of its corporate structure, reserve composition, and operational framework.

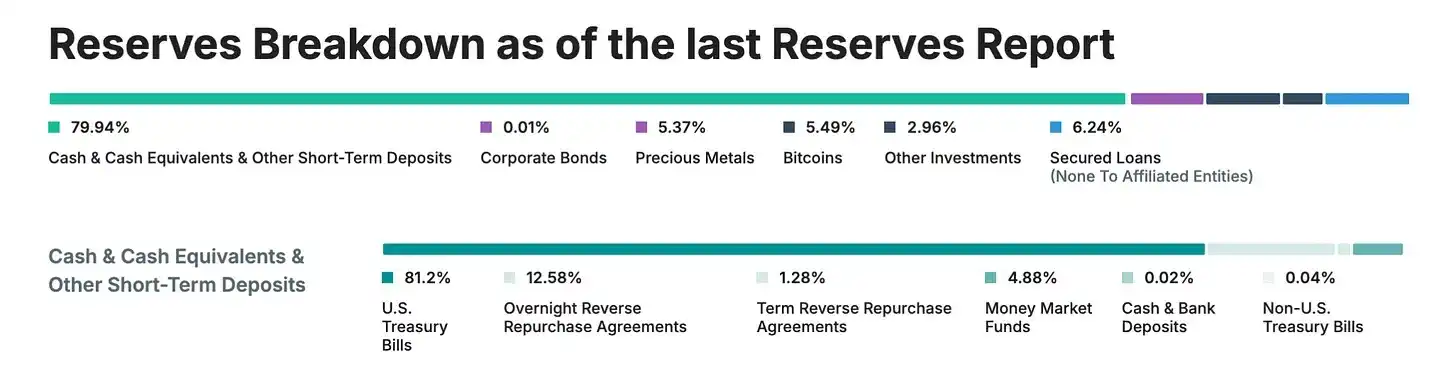

Even more problematic for Tether is that true compliance with the GENIUS Act requires the kind of transparency the company has historically shied away from. As of 2025, Tether still provides quarterly "certifications" rather than full audits. Approximately 16% of its reserves are held in assets explicitly prohibited by the GENIUS Act: gold (3.5%), Bitcoin (5.4%), secured loans, and corporate bonds.

So why not just fix USDT?

Why launch a whole new token instead of simply making USDT compliant?

Simply put, transforming USDT into a compliant currency is like trying to transform a speedboat into an aircraft carrier while it's still sailing. USDT currently serves 500 million users worldwide, who choose it because it's not subject to strict US regulation. Many of these users are in emerging markets, where USDT provides access to US dollars when local banking systems are unreliable or costly.

If Tether were to suddenly impose US-level KYC requirements, freeze functionality, and audit protocols on all USDT users globally, it would fundamentally change the nature of USDT’s success. A small business owner in Brazil using USDT to hedge against currency fluctuations doesn’t want to deal with US regulatory compliance, and a cryptocurrency trader in Southeast Asia doesn’t need monthly certifications from their CEO.

But there's a deeper strategic reason behind this: market segmentation. By creating USAT, Tether can offer a "high-end" regulated product to US institutions while maintaining USDT as the "global standard" for other markets. It's like owning both a luxury brand and a mass-market brand—the same company, offering different products to different customers.

USAT's value proposition (as such)

So what exactly does USAT offer that USDC doesn’t? Tether’s promotion seems a bit vague in this regard.

The technical architecture supports this dual-track strategy. Both tokens utilize Tether's Hadron platform, allowing for seamless integration with existing infrastructure while maintaining regulatory separation. Liquidity can flow between the two systems where legally permitted, but compliance "firewalls" ensure that each token operates independently within its jurisdiction.

USAT will be issued by Anchorage Digital Bank, a federally chartered crypto bank, with reserves held in custody by Cantor Fitzgerald. It will be fully compliant with the GENIUS Act, including monthly audits, transparent reserves, and all the regulatory requirements expected by institutional users. Led by former White House crypto advisor Beau Hines, USAT benefits from strong political support and connections in Washington.

However, Circle's USDC already meets all of these requirements. USDC boasts deep liquidity, mature exchange integrations, institutional partnerships, and a strong regulatory record. It has become the preferred stablecoin for US institutions.

Tether's key advantage is that... well, it's Tether. The company has built the world's largest stablecoin distribution network, holds a massive existing market share, and generates $13.7 billion in annual profits to support its growth. As CEO Paolo Ardoino puts it, "Unlike our competitors, we don't rent distribution channels; we own them."

Tether needed to build liquidity for USAT from scratch. This meant convincing exchanges to list USAT, getting traders to provide liquidity, and institutional clients to actually use it. Even with Tether’s deep pockets and vast distribution network, this was no easy task.

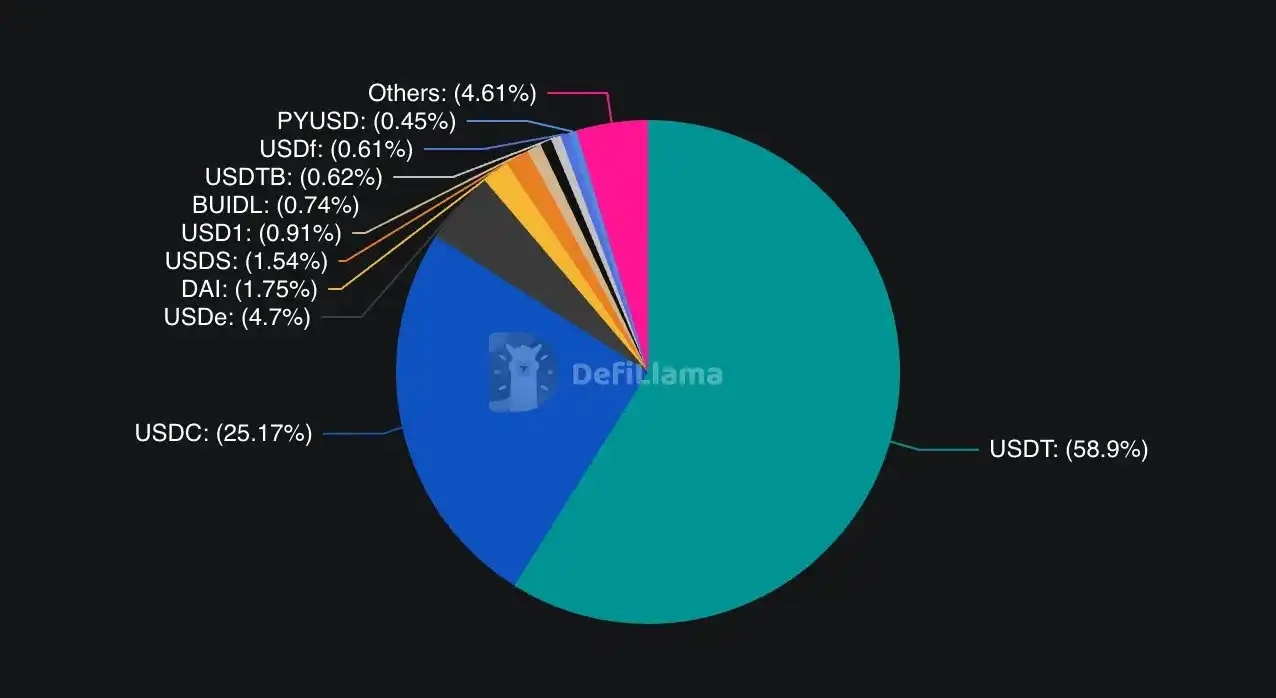

USDC controls approximately 25% of the global stablecoin market but dominates the regulated U.S. market. USDT holds 58% of the global market share but is largely excluded from the regulated U.S. market.

The company is betting that institutional users need alternatives to avoid the risks of concentration. If Circle or USDC stumble, institutional users might seek other fully regulated options. Additionally, Tether can leverage its existing relationships, such as its partnership with Cantor Fitzgerald, to offer better terms or services.

Circle's recent moves highlight the intensity of the competition. In June 2025, Circle successfully went public, launched Arc, a blockchain specifically for stablecoin finance, and continued to expand its global payment channels. Circle's regulatory-first strategy is clearly paying off in terms of institutional adoption.

But USAT also offers certain advantages that USDC lacks. According to CEO Paul Ardoino, Tether's global distribution network includes "hundreds of thousands of physical distribution points," as well as digital partnerships like its $775 million investment in Rumble. This infrastructure, built over more than a decade, is difficult to replicate.

Tether's strength lies in its global relationships and financial strength. In the first half of 2025, the company generated $5.7 billion in profits, providing ample resources for market creation, liquidity incentives, and partnership development. Unlike competitors who must "rent" distribution channels, Tether owns its own infrastructure.

USAT's biggest advantage may be compatibility. If it works with existing USDT infrastructure, users won't have to completely overhaul their systems. For developers who have already spent months integrating USDT, switching to another Tether token is a much better option than starting from scratch with an entirely different provider.

Some institutions or risk-conscious users may simply want to hold multiple regulated stablecoins for diversification and reduce counterparty risk between Circle (USDC) and Tether (USAT).

Timeline is crucial here. USAT's planned launch date of late 2025 means Tether has limited time to build liquidity, secure exchange listings, and establish market maker relationships. In financial markets, first-mover advantage can be crucial, with users often preferring established and liquid options over newcomers.

The timeline here is crucial. USAT is scheduled to launch by the end of 2025, leaving Tether with limited time to build liquidity, secure exchange listings, and establish market maker relationships. In financial markets, first-mover advantage is crucial—users generally gravitate toward established and liquid options over newcomers.

Critics argue that USAT is essentially a “compliance show”—a way for Tether to enter the U.S. market without addressing transparency and operational issues in its core business.

This criticism has some merit. Tether’s decision to launch USAT rather than fully comply with USDT regulations suggests that the company prioritizes immediate operational flexibility over comprehensive regulatory legitimacy.

On the other hand, some might argue that this is exactly how the market should work. Different customer segments have different needs and risk appetites. US institutions demand regulatory compliance and transparency, while emerging market users prioritize accessibility and low fees. Why can't a single company cater to both segments through different products?

in conclusion

Tether’s dual stablecoin strategy reflects the broader tensions in the crypto industry regarding regulation, decentralization, and institutional adoption. The industry is increasingly challenged to balance the original permissionless spirit of cryptocurrencies with the need for regulatory frameworks to foster mainstream adoption.

USAT represents Tether’s bet that it can secure regulatory legitimacy for institutional users while maintaining flexibility for global retail investors. The success of this strategy will depend on execution, market acceptance, and the stability of the evolving regulatory framework.

The regulatory landscape remains fluid. While the GENIUS Act provides some clarity, the specifics of its implementation and enforcement remain uncertain. Changes in administration or shifting regulatory priorities could significantly impact the strategies of stablecoin issuers.

More fundamentally, USAT raises crucial questions about the nature of Tether’s initial success. Is USDT’s dominance built on regulatory arbitrage that may no longer be sustainable? Or does it reflect genuine innovation in global financial infrastructure, which regulatory compliance can facilitate rather than constrain?

The answer to this question may ultimately determine whether USAT represents Tether’s evolution into a mature financial institution or an acknowledgment of the fundamental limitations of its original model. Regardless, the launch of USAT marks a new chapter in stablecoin competition and regulation.

The king is establishing a second kingdom. Whether he can rule both simultaneously remains to be seen.