By 0xjacobzhao | https://linktr.ee/0xjacobzhao

Pendle is undoubtedly one of the most successful DeFi protocols of this crypto cycle . While many protocols have stagnated due to liquidity depletion and fading narratives, Pendle, with its unique yield splitting and trading mechanism , has successfully become a "price discovery platform" for yield-generating assets. Through its deep integration with yield-generating assets like stablecoins and LST/LRT, Pendle has established its unique position as "DeFi yield infrastructure."

In the research report " The Intelligent Evolution of DeFi: The Evolutionary Path from Automation to AgentFi, " we systematically reviewed and compared the three stages of DeFi's intelligent development: automation tools , intent-centric copilots, and AgentFi (on-chain agents) . Beyond lending and yield farming, two of the most valuable and readily implementable use cases, Pendle's PT/YT yield rights trading is considered a high-priority application that is highly compatible with AgentFi in our high-level vision. Pendle's unique "yield splitting + maturity mechanism + yield rights trading" architecture provides agents with a natural platform for strategic orchestration, enriching the possibilities for automated execution and yield optimization.

1. The basic principle of Pendle

Pendle is the first DeFi protocol focused on yield splitting and trading . Its core innovation lies in tokenizing and separating the future income streams of on-chain yield-generating assets (such as LST, stablecoin certificates of deposit, and loan positions), allowing users to flexibly lock in fixed returns, maximize return expectations, or engage in speculative arbitrage .

In short, Pendle builds a secondary market for the "yield curve" of crypto assets, allowing DeFi users to trade not only "principal" but also "yield." This mechanism is highly similar to the zero-coupon bond + coupon split in traditional finance, improving pricing accuracy and trading flexibility for DeFi assets.

Pendle's revenue splitting mechanism

Pendle splits a Yield-Bearing Asset (YBA) into two tradable tokens:

- PT (Principal Token, similar to a zero-coupon bond) : represents the principal value that can be redeemed at maturity, but no longer enjoys income.

- YT (Yield Token, similar to coupon rights) : represents all the income generated by the asset before maturity, but will be zero after maturity.

- For example, after depositing 1 ETH stETH, it will be split into PT-stETH (1 ETH can be redeemed at maturity, and the principal is locked) and YT-stETH (all staking income before maturity is obtained).

Pendle goes beyond a simple token split; it also provides a liquid market for PT and YT (equivalent to the secondary liquidity pool in the bond market) through a specially designed AMM (Automated Market Maker) . Users can buy and sell PT or YT at any time, flexibly adjusting their return risk exposure. The price of PT is typically below 1, reflecting its "discounted principal value," while the price of YT depends on market expectations of future returns. More importantly, Pendle's AMM is optimized for assets with maturity dates, allowing PT/YT of varying maturities to form a yield curve within the market, highly similar to the bond market in traditional finance.

It's important to note that among Pendle's stablecoin assets, PT (Principal Token, a fixed-income position) is equivalent to an on-chain bond. A fixed interest rate is locked in at a discount upon purchase, and upon maturity, it can be redeemed 1:1 for stablecoins. This offers stable returns with low risk, making it suitable for conservative investors seeking certainty in returns. Stablecoin Pools (liquidity mining positions) are essentially AMM market making. LP income comes from fees and incentives, resulting in highly volatile APYs and the risk of impermanent loss. These positions are more suitable for active investors who can tolerate volatility and pursue higher returns. In markets with active trading volume and generous incentives, Pool returns can potentially be significantly higher than PT fixed income. However, in periods of low trading volume and insufficient incentives, Pool returns are often lower than PT, and may even result in losses due to impermanent loss.

| project | Stablecoin PT | Stablecoin Pools |

| Asset Form | Bond tokens (redeemable to stablecoins upon maturity) | AMM liquidity pool (PT+YT trading market) |

| Sources of Revenue | Fixed interest rate (locked in principal discount) | Transaction fees + mining incentives |

| Risk Level | Lower (close to risk-free fixed income) | Higher (IL risk + liquidity risk) |

| Suitable for people | Want to protect principal and lock in fixed income | LPs who want to earn fees and incentives and can withstand volatility |

Pendle's PT/YT trading strategies primarily cover four main paths : fixed income, yield speculation, inter-period arbitrage, and leveraged returns , catering to investment needs with varying risk appetites. Users can lock in fixed returns by buying PT and holding it to maturity, effectively securing a guaranteed interest rate. Alternatively, they can buy YT, betting on rising yields or increased volatility, thereby speculating on returns. Investors can also exploit price differentials between PT/YT maturities to engage in inter-period arbitrage, or use PT and YT as collateral in multiple lending agreements to maximize their return exposure.

Boros Funding Rate Trading Mechanism

Beyond the profit splitting offered by Pendle V2, the Boros module further assetizes the funding rate , transforming it from a passive cost of holding a perpetual swap into an independently priced and tradable instrument. Through Boros, investors can directional speculate , hedge risk , or capitalize on arbitrage opportunities . This mechanism essentially introduces traditional interest rate derivatives (IRS, basis trading) into DeFi, providing new tools for institutional-level fund management and robust return strategies.

In addition to PT/YT trading and AMM pools and the Boros funding rate trading mechanism , Pendle V2 also provides several extended features. Although not the focus of this article, they still constitute an important supplement to the protocol ecosystem:

- vePENDLE : A governance and incentive model based on the Vote-Escrow mechanism. Users obtain vePENDLE by locking PENDLE, thereby participating in governance voting and increasing their profit distribution weight. It is the core of the protocol's long-term incentives and governance.

- PendleSwap : A one-stop asset exchange portal that helps users efficiently switch between PT/YT and native assets, improving the convenience of fund use and protocol composability. It is essentially a DEX aggregator rather than an independent innovation.

- Points Market : Allows users to trade various project points (Points) in advance in the secondary market, providing liquidity for airdrop capture and point arbitrage. It is more inclined towards speculation and topical scenarios rather than core value.

II. Pendle Strategy Panorama: Market Cycles, Risk Stratification, and Derivative Expansion

In traditional financial markets, retail investors' investment channels are primarily focused on stock trading and fixed-income wealth management products, making it difficult to directly participate in the higher-threshold bond derivatives market. In the crypto market, retail users are similarly more receptive to token trading and DeFi lending. While the emergence of Pendle has significantly lowered the barrier to entry for retail investors in bond derivatives trading, Pendle's strategies still require a high level of expertise, requiring investors to conduct in-depth analysis of yield-generating asset interest rate fluctuations in different market environments. Based on this, we believe that during different market phases—such as the early stages of a bull market, the bull market's euphoria, the bear market's decline, and periods of range-bound trading—investors should tailor their Pendle trading strategies to their risk appetite.

- During a bull market upswing: Market risk appetite gradually recovers, lending demand and interest rates remain low, and YT on Pendle is relatively cheap. Buying YT during this period is like betting on rising future yields. Once the market accelerates upward, lending rates and LST yields will rise, driving up YT's value. This is a typical high-risk, high-reward strategy, suitable for investors willing to invest early and capture the potential gains of a bull market.

- During the bull market's euphoria , surging market sentiment drives a surge in lending demand. Interest rates on DeFi lending protocols often rise from single digits to over 15–30%, driving up the value of YT on Pendle and significantly discounting PT. During this period, investors using stablecoins to buy PT effectively lock in a high interest rate at a discount, redeeming it 1:1 for the underlying asset upon maturity. This effectively hedges against volatility risk through "fixed-income arbitrage" in the late stages of a bull market. This strategy offers the advantages of being robust and rational, ensuring the safety of fixed income and principal during market corrections or bear markets. However, the trade-off is forgoing the potential for greater gains from holding volatile assets.

- During a bear market downturn, market sentiment is depressed, lending demand plummets, and interest rates fall sharply. YT returns approach zero, while PTs perform closer to risk-free assets. During this period, buying PTs and holding them to maturity means locking in a guaranteed return even in a low-interest environment, effectively establishing a defensive position. For conservative investors, this is a key strategy for mitigating return volatility and preserving principal.

- During periods of range-bound volatility, market interest rates lack trending and market expectations diverge significantly, leading to frequent short-term mismatches or pricing discrepancies between Pendle's PT and YT. Investors can generate stable price differentials by engaging in inter-period arbitrage between PT/YT maturities of different maturities or by capitalizing on mispricing of income rights caused by fluctuating market sentiment. These strategies require advanced analytical and execution skills and are expected to generate stable returns in non-trending markets.

Global Perspective: Pendle Strategy Full Market Cycle Comparison Chart

| Market Stage | Market characteristics | PT Strategy | YT Strategy | Stablecoin pool | Arbitrage strategies |

| Deep bear (sideways at low level) | Interest rates are extremely low, asset prices are undervalued, and sentiment is cold. | Little significance (PT has almost no discount) | ✅Best time : YT is extremely cheap, betting on future interest rate recovery, leveraging income streams (especially stETH) | ⚪ Low returns, almost idle positions | ⚪ Limited interest rate spreads and few opportunities |

| Slow Bear (slow decline) | Prices are slowly falling, interest rates are low, and the market is directionless. | ⚪ Fixed income is not high and the attractiveness is average | ❌ YT has no meat, you may lose all your money | ✅Defense first choice : Stable currency pool to protect principal and relax your mind | ⚪ Can do small cross-platform arbitrage, but the space is limited |

| Early stage of bull market (rebound upward) | Borrowing demand rises, and interest rates start to rise | ⚪ PT starts to have discounts, but not big | ✅Strong explosive power : YT low valuation → interest rate rebound → income leverage | ⚪ Stablecoin pools are less interesting than volatile asset pools | ⚪ You can invest in PT fixed income vs floating interest rate differentials |

| Mid-bull market (accelerated rise) | Interest rates have increased significantly, and sentiment has improved. | ✅Lock in fixed income : PT has a large discount, lock in 10-20% annualized return | ✅Double your profits : YT price rises, continue to increase your position to bet on rising interest rates | ⚪ Fixed income opportunities are inferior to PT/YT | ✅Arbitrage opportunity : Pendle fixed income vs Aave floating rate spread is large |

| Bull market excitement period (high point) | Borrowing rates soar, markets frenzy | ✅Best strategy : PT is deeply discounted, lock in 20–30% fixed income | ❌ High risk: YT premium is too high and it is easy to lose money | ⚪ The interest rate of the stablecoin pool is high, but not as attractive as PT | ✅Institutional play : term arbitrage, cross-market arbitrage, low-risk profit locking |

| Bull peak correction period | Market reversal, interest rates fall rapidly | ⚪ PT discount narrows, weakening its appeal | ❌ YT value has shrunk significantly and is likely to return to zero | ✅ Funds shift to defense, stablecoin pools return to the mainstream | ✅ Do hedging arbitrage to reduce volatility risk |

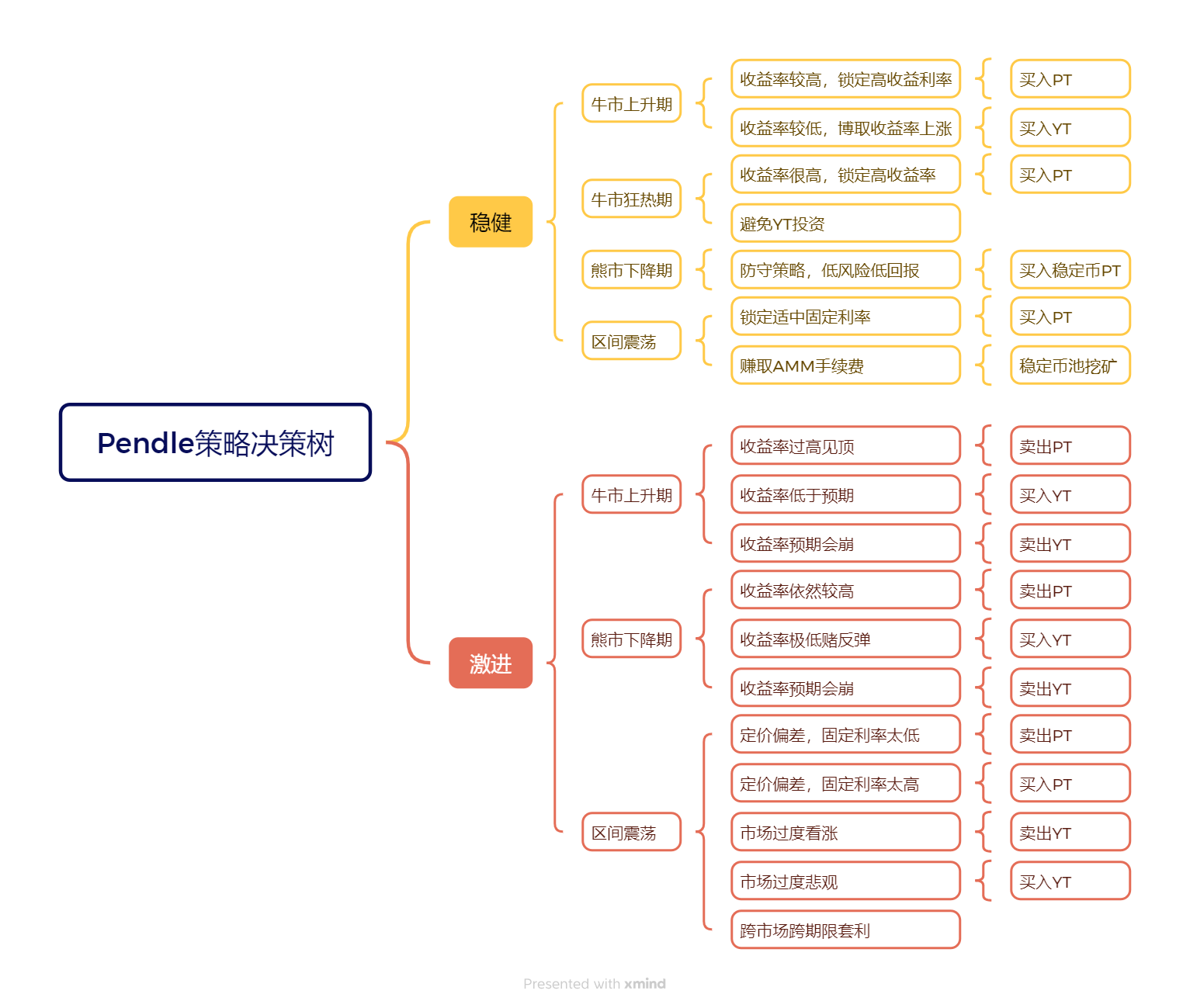

Risk Stratification: Pendle Decision Tree for Conservative vs. Aggressive Strategies

Of course, the above strategies are generally focused on achieving stable returns. Their core principle is to balance risk and reward through buying PT, buying YT, or participating in stablecoin pool mining during different market cycles. For aggressive investors with a higher risk appetite, they can also choose a more aggressive strategy of selling PT or YT to bet on interest rate trends or market mismatches. These strategies require higher levels of professional judgment and execution, and carry greater risk exposure. Therefore, this article will not elaborate on these strategies in detail, but serves only as a reference. For details, please see the decision tree below.

Pendle Coin-Based Strategy: Comparison of stETH, uniBTC, and Stablecoin Pools

Of course, the above analysis of Pendle strategies is based on a U-standard perspective. The strategy focuses on how to achieve excess returns by locking in high interest rates or capturing interest rate fluctuations . In addition, Pendle also offers coin-standard strategies for BTC and ETH.

ETH is widely considered the best target for a coin-based strategy due to its ecosystem status and long-term value certainty. As the native asset of the Ethereum network, ETH not only serves as the settlement basis for most DeFi protocols but also offers a stable source of cash flow through staking yield. In contrast, BTC has no native interest rate, and its returns on Pendle rely primarily on protocol incentives, making its coin-based strategy relatively weak. Stablecoin pools, on the other hand, are more suitable as a defensive investment, fulfilling the role of "preserving value while waiting."

In different market cycles, the strategies of the three asset pools vary significantly:

- Bull market : stETH pool is the most aggressive, YT is the best strategy for leveraging ETH holdings; uniBTC can be used as a supplement, but is more speculative; the attractiveness of the stablecoin pool is relatively declining.

- Bear market : stETH's low price provides a core opportunity to increase ETH holdings; the stablecoin pool assumes the main defensive function; uniBTC is only suitable for small-scale short-term arbitrage.

- In a volatile market : stETH's PT-YT mismatch and AMM fees provide arbitrage opportunities; uniBTC is suitable for short-term speculation; and the stablecoin pool provides a stable supplement.

| assets | Sources of Revenue | risk | Currency standard effect | bull market | bear market | Volatile Market |

| stETH pool | ETH Staking Native Yield (3–5% APY) | ETH price fluctuations | ✅ Increase holdings in ETH (YT can amplify returns) | Buy YT : Bet on higher interest rates and capture leveraged staking returns; Buy discounted PT : Lock in high interest rates | Buy cheap YT : Get leveraged ETH Staking income and achieve ETH standard growth | Cross-period arbitrage/PT-YT mismatch : Suitable for profiting from AMM fees and price fluctuations |

| uniBTC Pool | Lending interest rates/protocol incentives (non-native benefits) | BTC has no native interest rate, and its income depends on the sustainability of incentives. | ⚠️ The logic of the currency standard is weak | Buy YT in the short term when loan demand is strong to earn incentive benefits | Unstable returns, suitable for small position speculation | YT pricing fluctuates , allowing for short-term speculation or cross-market arbitrage |

| Stablecoin pool | Stablecoin lending rates (2–5% APY) | Low interest rates limit the appeal of PT/YT | ❌ Non-currency-based growth | Fixed income is not as volatile as other assets and is suitable for very conservative investors. | Core defense : Lock in stable interest rates and wait for the market to recover | Small interest rate arbitrage provides low volatility supplementary income |

Boros Strategy Panorama: Interest Rate Swaps, Hedging, and Inter-Market Arbitrage

Boros capitalizes the floating variable of the funding rate, essentially introducing interest rate swaps (IRS) and basis trading (carry trade) from traditional finance into DeFi. This transforms the funding rate from an uncontrollable cost item into a configurable investment tool. Its core token, Yield Units (YU), supports three main strategic paths: speculation, hedging, and arbitrage .

- In terms of speculation , investors can bet on rising funding rates through Long YU (paying a fixed rate Implied APR and receiving a floating rate Underlying APR), or bet on falling funding rates through Short YU (receiving a fixed rate Implied APR and paying a floating rate Underlying APR), similar to traditional interest rate derivative trading.

- In terms of hedging , Boros provides institutions holding large perpetual contract positions with a tool to convert floating funding rates into fixed rates;

- Funding Rate Hedging: Long Perp + Long YU, locking the floating funding rate expenditure into a fixed cost.

- Locking the Funding Rate Income Hedging: Short Perp + Short YU → Lock the floating funding rate income into a fixed income.

- In terms of arbitrage , investors can use a Delta-Neutral Enhanced Yield or Arbitrage / Spread Trade to take advantage of cross-market (Futures Premium vs. Implied APR) or cross-term pricing differences to obtain relatively stable interest rate spread returns.

Overall, Boros is suitable for professional funds for risk management and steady gains , but its friendliness to retail users is limited.

| Strategy Type | How to operate | Suitable for people | Analogy to traditional tools |

| Funding Hedge | Funding rate hedging : Go long Perp on CEX/DEX and long YU on Boros; Funding rate income hedging : short Perp on CEX/DEX and short YU on Boros | Large long and short positions, Basis Trader | Interest Rate Swap (Payer/Receiver Swap) |

| Delta-Neutral Fixed Income | Spot staking (e.g. stETH to get 4% base income) + shorting Perp to hedge price risk + locking in fixed funding income in Boros Short YU | Conservative institutions and hedge funds | Cash & Carry + Swap |

| Cross-market/term arbitrage | Cross-market arbitrage : Compare Futures Premium and Boros Implied APR, short the overvalued side and long the undervalued side; Term arbitrage : When there is a pricing difference between YU with different maturities, short the overvalued maturity and long the undervalued maturity | Professional arbitrage funds | Treasury yield curve arbitrage |

3. Pendle Strategy Complexity and AgentFi’s Unique Value

Based on the analysis above, Pendle's trading strategy is essentially a complex bond derivative transaction. Even the simplest purchase of PT to lock in a fixed return requires consideration of multiple factors, including rollover, interest rate fluctuations, opportunity costs, and liquidity depth. This goes without mentioning YT speculation, inter-period arbitrage, leveraged portfolios, and dynamic comparisons with external lending markets. Unlike floating-yield products like lending or staking, which offer a "one-time deposit and continuous interest," Pendle's PT (principal token) must have a specific maturity date (typically weeks to months). Upon maturity, the principal is redeemed at a 1:1 ratio for the underlying asset, requiring a new position to continue earning returns. This "periodic" maturity constraint is a necessary prerequisite for the fixed income market and a fundamental difference between Pendle and perpetual lending protocols.

Currently, Pendle does not have an official built-in automatic renewal mechanism, but some DeFi strategy vaults provide " Auto-Rollover" solutions to strike a balance between user experience and protocol simplicity. Currently, there are three Auto-Rollover modes: passive, smart, and hybrid.

- Passive Auto-Rollover: The logic is simple: upon maturity, the principal of a PT is automatically rolled over into a new PT, providing a smooth user experience. However, this approach lacks flexibility. If the floating interest rates of Aave and Morpho become higher, forced rollovers will incur opportunity costs.

- Smart Auto-Rollover: Vault dynamically compares Pendle's fixed interest rate with the floating interest rate in the lending market, avoiding "blind renewals" and maintaining flexibility while increasing returns, better meeting the need for maximizing returns.

- If Pendle fixed rate > loan floating rate → reinvest in PT to lock in a more certain fixed income;

- If the floating interest rate of the loan is greater than the fixed interest rate of Pendle , transfer to a lending protocol such as Aave/Morpho to obtain a higher floating interest rate.

- Mixed allocation : Part of the funds are locked in the PT fixed interest rate, and part of the funds flow into the lending market, forming a combination that is both stable and flexible, avoiding being "left behind" by a single interest rate environment in extreme situations.

Therefore, AgentFi offers unique value within Pendle trading strategies : it automates complex interest rate speculation. Pendle's fixed-rate lending rate and floating lending rates fluctuate in real time, making it difficult for humans to continuously monitor and switch between them. While standard Auto-Rollover simply rolls over, AgentFi dynamically compares interest rates, automatically adjusts positions, and optimizes position allocation based on user risk preferences. In more complex Boros strategies, AgentFi can also handle funding rate hedging, cross-market arbitrage, and term arbitrage, further unlocking the potential of professional yield management.

4. Pulse: The first AgentFi product based on Pendle’s PT strategy

In our previous AgentFi research report, " A New Paradigm for Stablecoin Yields: From AgentFi to XenoFi ," we introduced ARMA ( https://app.arma.xyz/ ), a stablecoin yield-optimizing agent built on Giza's infrastructure. Deployed on the Base Chain, ARMA automatically switches between lending protocols like AAVE, Morpho, Compound, and Moonwell, maximizing cross-protocol returns and maintaining its position as a top-tier agent within AgentFi.

In September 2025, the Giza team officially launched Pulse Optimizer ( https://app.usepulse.xyz/ ), the industry's first AgentFi automated optimization system based on the Pendle PT fixed income market . Unlike ARMA, which focuses on stablecoin lending, Pulse specializes in the Pendle fixed income scenario. Using a deterministic algorithm (non-LLM), it monitors the multi-chain PT market in real time. It dynamically allocates positions using linear programming, taking into account cross-chain costs, maturity management, and liquidity constraints. It also automates rollovers, cross-chain scheduling, and compounding. Its goal is to maximize portfolio APY while managing risk, abstracting the complex process of "finding/APY/swapping/cross-chain/timing" into a one-click fixed income experience.

Pulse Core Architecture Components

- Data Collection : Capture Pendle multi-chain market data in real time, including active markets, APY, expiration time, liquidity, and cross-chain bridge fees, and model slippage and price impact to provide accurate input for the optimization engine.

- Wallet Manager : Serves as the asset and logic hub, generating portfolio snapshots, managing cross-chain asset standardization, and performing risk control (such as minimum APY improvement thresholds and historical value comparisons).

- Optimization Engine : Based on linear programming modeling, it comprehensively considers fund allocation, cross-chain sources, bridge fee curve, slippage and market maturity, and outputs the optimal configuration plan under risk constraints.

- Execution Planning : Convert optimization results into a trading sequence, including liquidating inefficient positions, planning bridge and swap paths, rebuilding new positions, and triggering a full exit mechanism when necessary to form a complete closed loop.

| Components | Key Mechanisms | Output |

| Data collection | Integrate Pendle API with multi-chain price sources to monitor market and slippage | Real-time market data streaming |

| Wallet Management | Portfolio snapshot, asset standardization, cross-chain conversion, and risk control | Portfolio status and reallocation control |

| Optimize Engine | Fund allocation modeling, cross-chain cost curves, and diminishing returns constraints | Optimal configuration solution |

| Execution Plan | Liquidate old positions → Plan bridge/Swap → Open positions/Exit | Executable cross-chain transaction scripts |

5. Pulse Core Functions and Product Progress

Pulse currently focuses on optimizing ETH-based yields , automating the management of ETH and its liquid staking derivatives (wstETH, weETH, rsETH, uniETH, etc.), and dynamically allocating them across multiple Pendle PT markets. Using ETH as the underlying asset, the system automatically converts tokens across multiple chains to achieve optimal allocation. Currently live on the Arbitrum mainnet, Pulse plans to expand to Ethereum mainnet, Base, Mantle, Sonic, and others, achieving multi-chain interoperability through the Stargate bridge.

Pulse user experience throughout the entire process

Agent Activation and Fund Management: Users can activate Pulse Agent with a single click on the official website ( www.usepulse.xyz ). The process includes connecting to a wallet, network authentication, whitelist verification, and a minimum deposit of 0.13 ETH (approximately $500). Upon activation, funds are automatically deployed to the optimal PT market and enter a continuous optimization cycle. Users can add funds at any time, and the system will automatically rebalance and reallocate funds. There is no minimum deposit requirement for subsequent deposits, and larger deposits can enhance portfolio diversification and optimization.

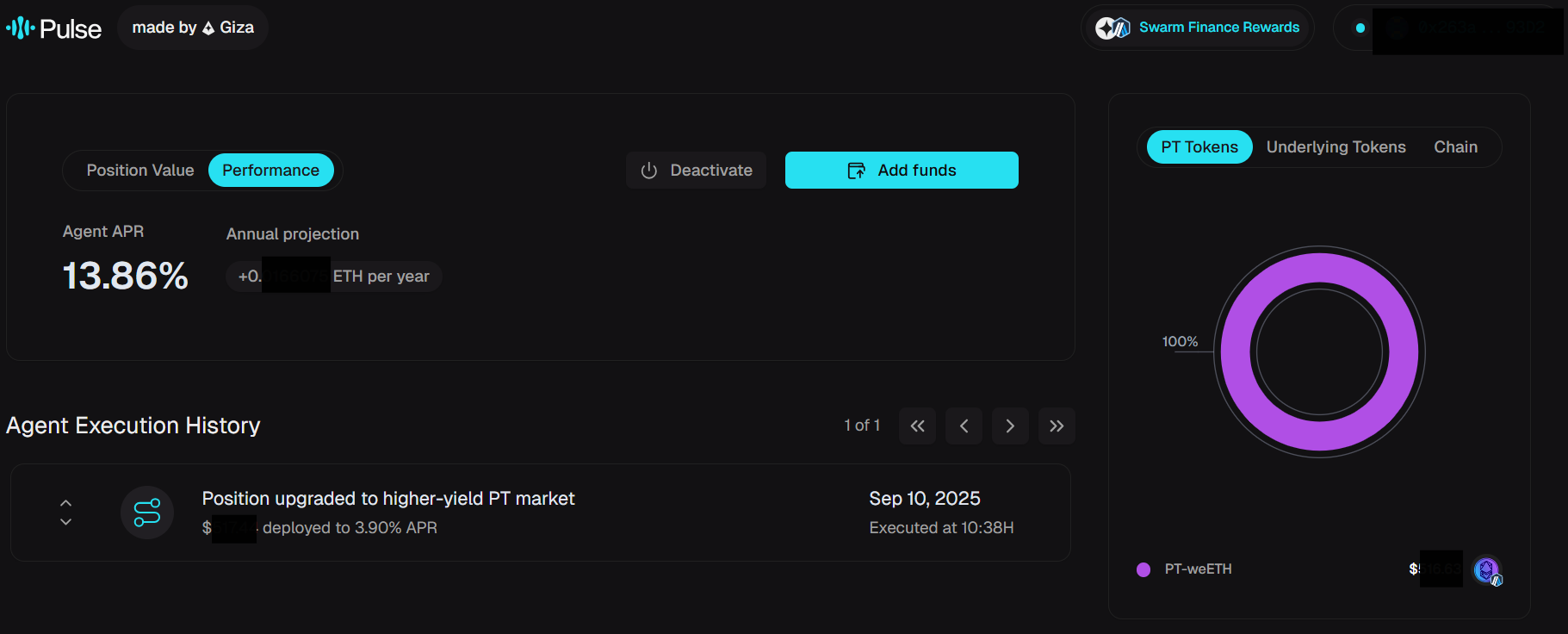

Data dashboard and performance monitoring

Pulse provides a visual data dashboard to track and evaluate investment performance in real time:

- Key indicators : total asset balance, cumulative investment, principal and return growth rate, position distribution of different PT tokens and cross-chain positions.

- Return and Risk Analysis : Supports trend tracking on a daily/weekly/monthly/yearly basis, combined with real-time APR monitoring, annual forecasts, and market comparisons to help measure excess returns from automated optimization.

- Multi-dimensional analysis : Displayed by PT Token (such as PT-rETH, PT-weETH), Underlying Token (LST/LRT protocol) and cross-chain distribution.

- Execution transparency : Complete operation logs are retained, including rebalancing time, operation type, fund size, return impact, and on-chain hash to ensure verifiability.

- Optimization Results : Provides information on rebalancing frequency, APR improvement, diversification, and market responsiveness, and compares it with static holdings or market benchmarks to assess risk-adjusted returns.

Exit and Asset Withdrawal: Users can terminate their Agent at any time. Pulse will automatically liquidate PT tokens and convert them back to ETH, charging a 10% success fee on any profits. Principal will be fully returned. The system will transparently display a detailed breakdown of earnings and fees before exiting, and withdrawals are typically completed within minutes. Users can reactivate their Agent at any time, and their historical earnings records will be fully preserved.

6. Swarm Finance: Active Liquidity Incentive Layer

In September 2025, Giza officially launched Swarm Finance , an incentive distribution layer designed specifically for active capital . Its core mission is to connect protocol incentives directly to the network of agents through standardized APR feeds (sAPR) , making capital truly "smart."

- For users : Funds can be optimally allocated across multiple chains and protocols in real time and automatically , without the need for manual monitoring or reinvestment, to capture the highest return opportunities.

- For the protocol : Swarm Finance solves the pain point of TVL loss due to maturity redemption in projects such as Pendle, bringing more stable and sticky liquidity while significantly reducing the governance costs of liquidity management.

- For the ecosystem : capital can complete cross-chain and cross-protocol migration in a shorter time, improving market efficiency, price discovery capabilities and capital utilization.

- For Giza itself : All incentive traffic routed through Swarm Finance will partially flow back to $GIZA , starting the Tokenomics flywheel through the fee capture → buyback mechanism.

According to official Giza data, Pulse achieved an APR of approximately 13% when Arbitrum launched the ETH PT market. More importantly, Pulse's automatic rollover mechanism addressed the TVL loss caused by redemptions at maturity on Pendle, establishing a more robust capital accumulation and growth curve for Pendle. As the first implementation of the Swarm Finance incentive network , Pulse not only demonstrates the potential of intelligent agents but also officially marks the beginning of a new paradigm for active liquidity in DeFi.

VII. Summary and Outlook

As the industry's first AgentFi product based on the Pendle PT strategy, Pulse , launched by the Giza team, is undoubtedly a milestone. It abstracts the complex PT fixed-income trading process into a one-click intelligent agent experience, fully automating cross-chain configuration, maturity management, and automatic compounding. This significantly reduces the user experience and improves capital utilization and liquidity in the Pendle market.

Pulse is currently still primarily focused on ETH PT strategies . Looking ahead, with the continuous iteration of the product and the addition of more AgentFi teams, we expect to see:

- Stablecoin PT strategy products - providing matching solutions for investors with more stable risk appetite;

- Intelligent Auto-Rollover – Dynamically compares Pendle fixed rates with floating rates in the lending market, increasing returns while maintaining flexibility;

- Comprehensive strategy coverage based on market cycles - modularize Pendle's trading strategies in different bull and bear phases, covering YT, stablecoin pools, and even more advanced strategies such as short selling and arbitrage;

- Boros's strategic AgentFi product - achieves Delta-Neutral fixed income and cross-market/maturity arbitrage that is smarter than Ethena, promoting further professionalization and intelligence of the DeFi fixed income market.

Of course, Pulse faces the same risks as any DeFi product, including protocol and contract security (potential vulnerabilities in Pendle or cross-chain bridges), strategy execution risk (rollover or cross-chain rebalancing failures), and market risk (interest rate fluctuations, insufficient liquidity, and incentive erosion). Furthermore, Pulse's revenue relies on ETH and its LST/LRT markets. If the price of ETH drops significantly, even if the amount of ETH base increases, losses may still occur in USD terms.

Overall, the birth of Pulse not only expands AgentFi's product boundaries, but also opens up new imagination space for the automation and large-scale application of Pendle strategies in different market cycles, representing an important step in the intelligent development of DeFi fixed income.

Disclaimer: This article was created with the assistance of the AI tool ChatGPT-5. While the author has made every effort to proofread and ensure the accuracy of the information, some omissions are inevitable and we apologize for any inaccuracies. It is important to note that divergences between project fundamentals and secondary market price performance are common in the cryptoasset market. This article is intended solely for information aggregation and academic/research exchange and does not constitute investment advice or a recommendation to buy or sell any token.