Author: imToken

Yiwu and USDT, these two seemingly unrelated terms, are now being put in the same context.

As the "World Small Commodity Capital," Yiwu merchants used to need to go through layers of bank transfer agents if they wanted to sell their products to the Middle East, Latin America, and Africa. This process was not only time-consuming and costly, but also often faced the risk of capital stagnation.

However, the situation has been quietly changing in recent years. According to a research report by Huatai Securities, in Yiwu, stablecoins have become one of the important tools for cross-border payments. Buyers only need to complete the transfer on their mobile phones, and the funds will be credited within a few minutes. Chainalysis even estimates that as early as 2023, the flow of stablecoins on the Yiwu market chain will exceed 10 billion US dollars.

Although a subsequent survey by 21st Century Business Herald pointed out that most merchants in Yiwu have not heard of and do not understand stablecoins, and only a few merchants support stablecoin payments, this just shows that it is still in its early stages, but it has shown a trend of spreading.

In other words, stablecoins are becoming the "new dollar" for small and micro traders around the world to receive cross-border payments. Payment is not only the starting point of stablecoins, but also the most direct entry point for them to enter the global financial system.

01 From "payment" to "global payment"

Stablecoins have evolved to encompass diverse application scenarios: some use them to participate in DeFi mining, others to earn interest, and others to use them as collateral. However, behind these uses, payment remains the core function.

Especially in the cross-border payment scenario of "global payment", stablecoins are in sharp contrast with traditional finance.

As we all know, the Society for Worldwide Interbank Financial Telecommunication (SWIFT) system has long been the core pillar of cross-border transactions. However, under the needs of modern finance, its inefficiency is no longer sustainable. A cross-border remittance often has to go through multiple agent banks, with cumbersome procedures and slow settlement, which may take several days to complete. During this period, the layers of added fees keep transaction costs high.

For businesses that rely on cash flow, or individuals who need to send money home, these delays and costs are almost unbearable. To put it bluntly, although SWIFT still has global influence, it was not designed for the high efficiency needs of the digital economy.

Against this backdrop, stablecoins offer a fast, low-cost, and borderless alternative. They inherently offer low-cost, borderless, and real-time transactions. Cross-border transfers can be completed in minutes without multiple intermediaries, and fees are significantly reduced due to network differences.

For example, the cost of transferring stablecoins such as USDT/USDC on the mainstream Ethereum L2 network has dropped to a few cents per transaction, which is almost negligible. This makes stablecoins a natural option for "global payments", especially in Southeast Asia and Latin America, where cross-border funds are active and traditional channels are not smooth. It has gradually become the mainstream choice for small payments.

More importantly, for underdeveloped or even countries with turbulent economic and social development, stablecoins are not just "payment tools", they also have the function of short-term value storage - in the eyes of these users who are at risk of currency depreciation, holding stablecoins means more stable purchasing power protection.

This dual role of "payment + hedging" is precisely why "global payment stablecoin" deserves separate discussion.

Source: imToken Web (web.token.im)’s “Global Payment” (Remittance) Stablecoin

From the perspective of imToken, stablecoins are no longer a tool that can be summarized by a single narrative, but rather a multi-dimensional "asset complex" - different users and different needs will correspond to different stablecoin choices.

In this classification, "global payment stablecoins" (USDT, USDC, FDUSD, TUSD, EURC, etc.) are an independent category specifically for cross-border transfers and value circulation. Their roles are becoming increasingly clear: they are both the fast lane for global capital flows and the "new dollar" for users in turbulent markets.

02 Why can’t the global system avoid stablecoins?

If “payment” is the original purpose of stablecoins, then “global payment” is their most competitive application scenario. The reason is simple: stablecoins almost naturally fit the three major pain points of cross-border payments: cost, efficiency, and acceptability.

First of all, for payment scenarios, cost and efficiency are the core.

As mentioned above, traditional cross-border remittances often require multiple correspondent banks, taking days and costing tens of dollars. In comparison, the advantages of stablecoins are clear. The transaction fee for a single Ethereum L2 network is typically less than $1, making them a common tool for small cross-border payments in Southeast Asia, Latin America, and other regions.

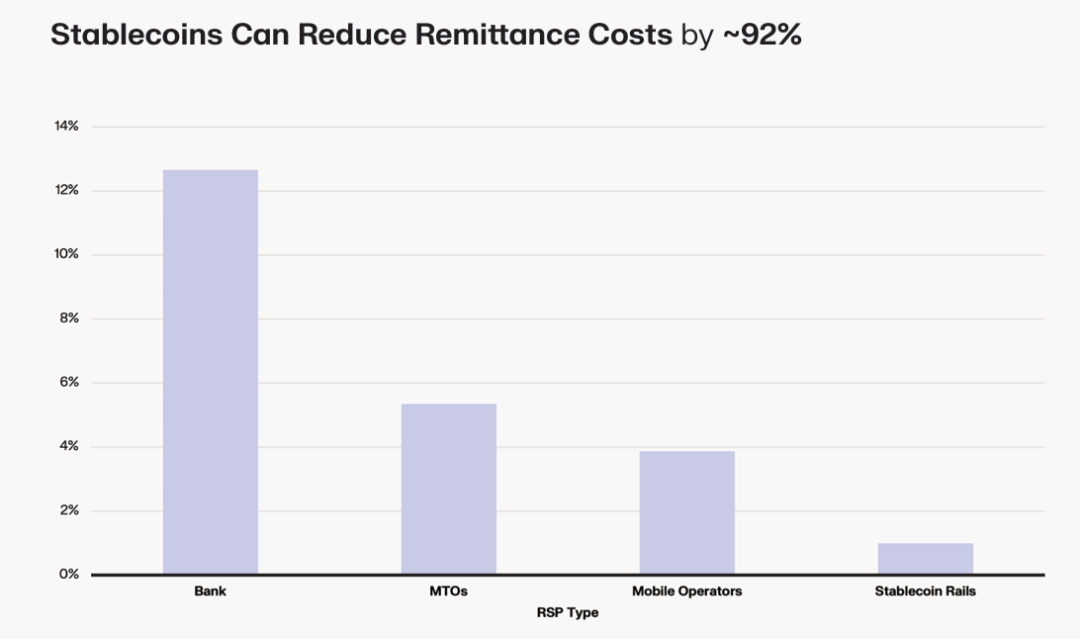

According to a Keyrock report, the cost of a traditional bank's cross-border remittance of $200 is approximately 12.66%, MTOs (remittance operators) is approximately 5.35%, and mobile operators are approximately 3.87%. Stablecoin platforms can reduce the cost of similar transfers to below 1%, significantly improving the efficiency of capital circulation. A stablecoin transfer usually only takes a few seconds to confirm on the Ethereum mainnet, and even shorter settlement times can be achieved on some L2 or emerging public chains. This experience is completely different from the T+N of the SWIFT system.

Secondly, in addition to efficiency and cost, whether payment can be widely adopted also depends on whether the other party is willing to accept it.

This is due to the mutual support between the crypto market and stablecoins over the years. USDT, as the world's largest stablecoin, has a market value that has long been stable at the level of hundreds of billions of US dollars and is the most widely accepted payment medium. USDC is favored by institutions due to its compliance and transparency, and has a high penetration rate in the European and American financial systems.

With continued penetration, USDT has almost become a de facto "savings currency" in countries such as Turkey, Argentina, and Nigeria where the local currencies have depreciated severely; USDC attracts institutions with its transparent reserves and compliance, and has a high penetration in the European and American markets; although EURC is smaller in scale, it plays an irreplaceable role in cross-border settlement in Europe.

Finally, for payments, speed and cost are important, but "whether the funds are truly safe" is even more critical.

With the implementation of the GENIUS Act in the United States, the implementation of the Stablecoin Ordinance in Hong Kong, and the successive pilot programs in markets such as Japan and South Korea, compliant issuance has gradually become the "pass" for stablecoins.

In the future, stablecoins that can enter the global payment system will most likely be "white-listed players" on the compliance path.

To sum up, it is no coincidence that stablecoins are becoming the infrastructure for "global payments". Rather, it is because they have formed an alternative advantage over traditional cross-border payments in terms of efficiency, cost, acceptance and transparency.

03 Payment is the starting point and also the bigger future

For this reason, stablecoins, which have gradually expanded their “global payment” attributes, are facing far more than just the transaction needs of native Crypto users, but have extended to a wider range of groups:

- Individuals and businesses with cross-border remittance or payment needs;

- Crypto traders who need to quickly transfer funds between different exchanges;

- Users facing devaluation of their own currencies and seeking safe havens in stable assets such as the US dollar or the euro;

From this perspective, "global payment" is both the original intention of stablecoins and their most realistic and urgent application scenario. They are not intended to overthrow the traditional banking system, but to provide a more efficient, lower-cost, and more inclusive supplementary solution, allowing cross-border settlements that used to require crossing multiple agent banks and taking several days to arrive to be completed in "a few minutes and a few cents."

The future trend is becoming increasingly clear. With the implementation of the US "GENIUS Act", the entry into force of the Hong Kong "Stablecoin Ordinance", and the launch of pilot programs in markets such as Japan and South Korea, global payment stablecoins will become an indispensable part of the financial system, whether for cross-border payments, corporate treasury, or personal risk hedging.

When we look back at Yiwu merchants' experimental attempts to accept USDT, we may find that this is not the story of a city, but a global microcosm - stablecoins are moving from the margins to the mainstream, from the chain to reality, and eventually becoming the new infrastructure for global value flow.

From this perspective, payment is the starting point for stablecoins and also their greater future towards global financial infrastructure.