Author: Gu Yu, ChainCatcher

An indisputable and obvious fact is that crypto VC has been declining in the market cycle of recent years. The return rate, voice and influence of almost all VC institutions have decreased to varying degrees, and even VC coins have been "sneered" by many investors.

There are many reasons for this. For example, since most VCs are accustomed to selling tokens and there are too many capital-funded projects, users have begun to dislike VC coins. More funds have flowed into narratives with low VC content, such as memes and AI agents, resulting in a lack of liquidity for VC coins. For example, the token unlocking cycle of VCs is getting longer and longer, resulting in a slower exit cycle and a disadvantageous position.

Several seasoned investors also offered their explanations. Jocy Lin, founder of IOSG Ventures, believes that during the 2021 bull market cycle, the primary market had extremely abundant liquidity, allowing VCs to raise a large amount of capital in a short period. This capital surplus led to generally inflated project valuations and inadvertently amplified the "narrative-driven" investment model. Many VCs are still stuck in the easy money model of the previous two cycles, believing that products and tokens are unrelated. They excessively pursue grand narratives and potential sectors, while ignoring the project's true product-market fit (PMF) and sustainable revenue model.

Jocy Lin further explained that the dilemma of cryptocurrency VCs is essentially a mismatch between their value capture capabilities and risk-taking. They bear the longest lock-up periods and the highest risks, yet they are in the weakest position in the ecosystem, squeezed at every level by exchanges, market makers, and KOLs. When the narrative-driven model collapses, native VCs lacking industry resources lose their foundation for existence—money is no longer a scarce resource; liquidity and certainty are.

According to Will, a partner at Generative Ventures, exchanges and market makers have become the ones truly exploiting all liquidity and premiums in this cycle. Most projects using VC money essentially do two things: first, marketing and hype; second, pay listing fees to exchanges. These projects are essentially marketing companies, needing to pay large sums to exchanges and market makers. Moreover, nowadays, VC-backed tokens are locked up for 2-3 years after listing, longer than in traditional securities markets, resulting in very poor liquidity expectations for unlocking and exiting, making it difficult to profit.

Anthony Zhu, founding partner of Enlight Capital, believes that Asian VCs primarily employing token strategies are caught in a death spiral in the current sluggish altcoin market. The rapid profit-making effect of the previous bull market created a strong path dependency at both the LP and GP levels. When this path is prolonged or even disappears, VCs are squeezed from both sides by LPs' short-term profit expectations and projects deviating from fundamentals, ultimately leading to distorted actions. The current situation is essentially a mismatch between some LPs, GPs, and market opportunities.

However, besides the overall decline in the VC landscape, a more noteworthy phenomenon and issue is that the overall activity and influence of Asian VC firms seem to have declined more significantly during this period. In RootData's 2025 Top 50 VCs list, compiled this month based on activity and exit performance, only 2-3 Asian VCs, including OKX Venture, made the cut. Furthermore, in the recent year's IPO boom and major M&A exits (Circle, Gemini, Bridge, Deribit, etc.), only IDG Capital achieved significant gains from its early-stage investment in Circle; other Asian VCs were largely absent.

Looking further, once very active and well-performing Asian VC institutions such as Foresight Ventures, SevenX Ventures, Fenbushi Capital, and NGC Ventures have made no more than 10 or even 5 investments this year, and have made very little progress in fundraising.

From once wielding immense influence to now falling into silence, why have Asian venture capital firms reached such a predicament?

1. Why can’t Asian VCs compete with European and American VCs?

Under the same environment, Asian VCs cannot compete with European and American VCs. According to some interviewees, this is mainly due to many reasons such as fund structure, LP type, and internal ecology.

Jocy Lin, founder of IOSG Ventures, believes this is partly due to the lack of a mature LP (Limited Partner) base in Asia. Consequently, many Asian VC funds primarily raise capital from high-net-worth individuals and entrepreneurs in traditional industries, as well as some idealistic OGs (Original Guru) in the crypto sector. Compared to the US and West, the lack of long-term institutional LPs and endowments means that Asian VCs, under pressure to exit their LPs, tend to favor thematic speculative investments rather than systematic risk management and exit strategies. Individual funds have shorter lifespans, making them more vulnerable to market contractions.

"In contrast, most European and American funds have a cycle of more than 10 years, and their overall systems in terms of fund governance, post-investment empowerment, and risk hedging are more mature, enabling them to maintain a more stable performance during downturns." In response, Jocy Lin also tweeted on X, calling on various exchanges to provide hundreds of millions of dollars in bailout funds. If she cannot participate herself, she can do so by investing in VCs to enable them to play the role of capital supporting entrepreneurs.

Jocy Lin also said that Western funds tend to pursue people-oriented investment values. Founders who can operate projects in the crypto industry for a long time and maintain the fundamentals of a project through cycles are very entrepreneurial and resilient. Such founders are also a minority in the industry. Some Western investors have succeeded, but the success rate of their investment model in the crypto industry is very limited.

Moreover, the way US funds subsequently inflated project valuations dragged down many participating Asian funds. Asian funds, with their shorter investment horizons and pursuit of short-term cash returns, began to diverge. Some funds invested in higher-risk sectors like gaming and social media, while others aggressively entered the secondary market. However, both approaches struggled to achieve above-average returns in the volatile altcoin market, and some even suffered significant losses. "Asian funds are a very loyal and committed group, but the industry has relatively let them down during this period," Jocy Lin lamented.

Anthony Zhu holds a similar view. He said that European and American funds are generally larger in size and have deeper pockets, so their investment strategies are more flexible and they perform better in a market environment that is not one-sidedly rising.

Another key factor is that European and American projects offer more exit strategies and opportunities, rather than solely relying on listing on a single exchange. In the recent year-long M&A boom, the main acquirers have been leading European and American crypto companies and financial institutions. Due to geographical, cultural, and other reasons, Asian crypto projects have not yet become high-priority targets for these acquirers. Furthermore, most current IPO projects are also from European and American backgrounds.

Source: RootData

Due to smoother equity exit channels, European and American VCs tend to have more diversified investment targets. However, many Asian VCs are limited by factors such as team background, fund structure and exit channels, and usually stay away from equity investments. As a result, they miss out on many project opportunities with returns of ten or even a hundred times the original investment.

However, Anthony also emphasized that while Asian crypto VCs primarily focused on token investments have generally underperformed since the last cycle, some Asian dollar VC firms investing in equity projects have performed exceptionally well. "Mainstream institutional VC investors are more patient, and their performance only becomes apparent over a longer period. Asia has some of the world's best crypto entrepreneurs dedicated to developing innovative products, and in the future, more and more Asian projects will enter mainstream exit channels in Europe and America. Asia also needs more long-term funding to support excellent early-stage projects."

Will offered another unconventional perspective. In his view, the poor performance of Asian VCs stemmed from their close proximity to Chinese exchanges. The closer they were, the worse it actually was, because they all pinned their exit hopes on listing on these exchanges, but in this cycle, exchanges were the biggest exploiters of liquidity. "If these VCs had understood the situation before, they should have bought exchange tokens, such as BNB, OKB, and BGB, instead of investing in so many small projects and becoming overly reliant on exchange listings, only to end up locked up themselves."

2. VC and Industry Transformation

Crisis breeds change, and a major reshuffle of the crypto VC landscape is inevitable. If 2016-2018 marked the rise of the first generation of crypto VCs, and 2020-2021 marked the rise of the second, then we are likely entering the third generation of crypto VC cycles.

In this cycle, in addition to the aforementioned renewed focus on US dollar equity investments, some VCs are shifting their strategies to focus more on the more liquid secondary market and related OTC sectors. For example, LD Capital has fully pivoted to the secondary market over the past year, acquiring significant positions in tokens like ETH and UNI, generating significant discussion and attention, and establishing itself as one of the most active players in the Asian secondary market.

Jocy Lin said that IOSG will not only pay more attention to primary market equity and agreement investments, but will also expand on its past basic investment research capabilities. In the future, it will consider various strategies such as OTC or passive investment opportunities and structured products to better balance risks and returns.

However, IOSG will remain active in the primary market. "In terms of investment preferences, we will pay more attention to projects with real income, stable cash flow and clear user needs in the future, rather than relying solely on narrative-driven projects. We hope to invest in products and sustainable business models that can still have endogenous growth momentum in an environment lacking macro liquidity," said Jocy Lin.

When discussing cash flow and revenue, Hyperliquid is arguably the most noteworthy project this cycle, with over $100 million in revenue in the past 30 days, according to DeFillama data. However, Hyperliquid has never received VC investment, and this community-driven, VC-independent development model has set a new path for many projects. Will more and more high-quality projects emulate Hyperliquid, further diminishing the role of crypto VCs? Furthermore, with the increasing number of KOL-led and community-based funding rounds, to what extent will they replace the role of VCs?

Anthony believes that for some DeFi projects, such as Perp, a model similar to Hyperliquid may persist due to the small team size required and strong monetization potential, but this may not be the case for other projects. In the long run, VC will remain a key force in driving large-scale development in the crypto industry and connecting institutional funding with early-stage projects.

“Hyperliquid’s success largely stems from the self-sustaining nature of its product—as a perpetual contract protocol, it naturally possesses the ability to generate revenue and a market-driven effect. However, this does not mean that the ‘no-VC’ model can be universally replicated. For most projects, VC remains a key source of product development funding, compliance advisors, and long-term capital in the early stages,” said Jocy Lin. She added that in any segment or industry within the traditional TMT sector (such as AI or healthcare), no sector exists without VC and capital participation; an industry without VC is absolutely unhealthy. VC’s competitive advantage hasn’t disappeared; rather, it has shifted from providing money to providing resources and patience.

Jocy Lin also shared a statistic: For projects backed by top VCs, the three-year survival rate is 40%. For projects driven entirely by the community, the three-year survival rate is less than 10%.

Discussing KOL and community funding rounds, Jocy Lin believes their rise is indeed changing the structure of early-stage financing. They can help build consensus and community momentum in the early stages of a project, offering advantages particularly in marketing and GTM. However, this model's capabilities are primarily limited to narrative communication and short-term user mobilization, with limited support for a project's long-term governance, compliance, product strategy, and institutional expansion.

Today, Asian crypto VCs are facing their lowest point in years. Rapid changes in internal and external ecosystems and narrative logic have led VCs to different trajectories. Some VCs' names have fallen into the dust of history, some VCs are still hesitating, and some VCs are already making drastic adjustments to explore how to form a healthier and more lasting relationship with projects.

However, the bloodsucking behavior of market makers and exchanges continues, and Binance Alpha's high frequency of listings has even exacerbated this situation. How to break free from this negative ecological relationship and find breakthroughs in exit paths and investment strategies will remain one of the biggest challenges for the new generation of VC models.

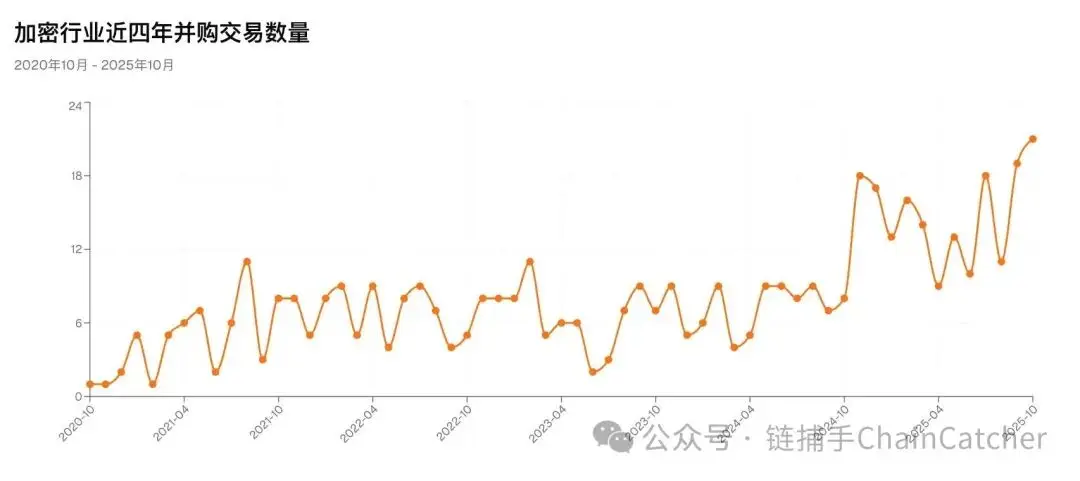

Recently, crypto industry giants like Coinbase have significantly accelerated their mergers and acquisitions. According to RootData, there have been over 130 mergers and acquisitions in the first 10 months of this year, at least 7 crypto companies have gone public, and the total funds raised by crypto-related listed companies (including DAT) have exceeded $16.4 billion, all setting new records. Reliable sources indicate that a well-known traditional Asian VC firm has established an independent fund primarily focused on equity investment, with a duration of approximately 10 years. More and more VCs are moving towards the "old rules" of the equity investment market.

This is probably one of the strongest signals that the market is sending to VCs about a new cycle: there are still many opportunities in the primary crypto market, and the golden period for equity investment may have arrived.