Author: Ignas

Compiled by: Tim, PANews

The Uniswap Foundation voted to approve a huge investment plan of US$165.5 million. Why?

Because the performance of Uniswap v4 and Unichain after their release was far from market expectations.

In a little over a month:

- Uni v4’s total locked value (TVL) is only $85 million

- Unichain’s TVL is only $8.2 million

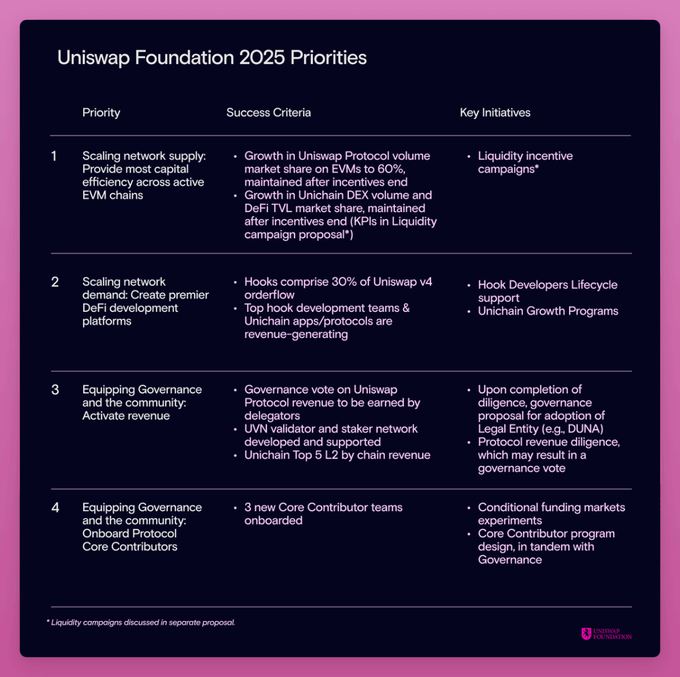

To foster growth, the Uniswap Foundation proposes to allocate $165.5 million to:

- $95.4 million for funding (developer programs, core contributors, validators);

- $25.1 million for operations (team expansion, governance tool development);

- $45 million for liquidity incentives.

As you can see, Uni v4 is not only a DEX, but also a liquidity platform, and Hooks is the application built on it.

Hooks should drive growth in the Uni v4 ecosystem, so this needs to be accelerated through funding programs.

Detailed allocation of funding budget:

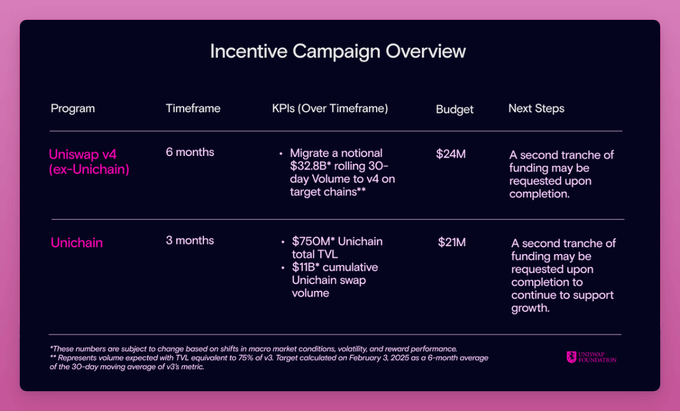

$45 million in liquidity provider (LP) incentives will be used for the following:

- $24 million (disbursed over 6 months): used to incentivize the migration of liquidity from other platforms to Uni v4;

- $21 million (disbursed in 3 months): Push Unichain’s total locked value (TVL) from the current $8.2 million to $750 million.

In comparison, Aerodrome mints approximately $40-50 million worth of AERO tokens per month for liquidity provider (LP) incentives.

The proposal has passed the temperature check stage, but still faces some criticism:

As the industry landscape changes, Aave proposes to repurchase $1 million of AAVE tokens per week, and Maker plans to repurchase $30 million per month. However, UNI holders are like "cows" that are about to be squeezed dry, and the value of their tokens has never been captured.

The UNI token does not have a fee-sharing mechanism enabled, and Uniswap Labs has earned $171 million through front-end fees in two years.

The key to the entire system lies in Uniswap’s organizational structure design:

- Uniswap Labs: Focus on protocol technology development;

- Uniswap Foundation: Promotes ecosystem growth, governance, and funding initiatives (such as grants, liquidity incentives).

What a savvy legal team.

Aave and Maker have established a closer interest binding relationship with token holders, and I don’t understand why Uniswap’s front-end fees cannot be shared with UNI holders.

In summary, other criticisms focus on the high salaries of the core team, Gauntlet’s responsibility for liquidity incentive enforcement, and the establishment of a new centralized DAO legal structure (DUNA).

As a small Uniswap governance representative, I voted in favor of this proposal, but still have significant concerns about the future of UNI holders: the incentive mechanism is not aligned with the interests of holders.

However, I am a big fan of Uniswap and highly recognize its role in promoting the DeFi field. The current growth of Uni v4 and Unichain is very bleak, and they need to introduce incentives to promote development.

The next Uni DAO vote should focus on the value capture mechanism of the UNI token.