By Joey @IOSG

Hyperliquid has been getting a lot of attention over the past few months. This post aims to keep everyone up to date on the latest developments and what to expect in the future. It serves as both a beginner's guide to Hyperliquid and some nuanced insights into the ecosystem as a whole.

TL;DR

For those who just want to get the gist of this article and its key takeaways:

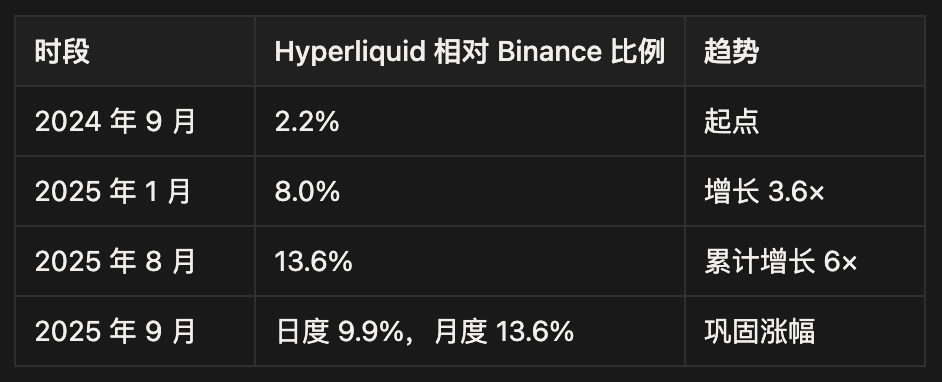

Hyperliquid quietly captures 13.6% of Binance’s monthly perpetual swap volume, generating $116 million in monthly revenue — but most analysis overlooks the subtle risk/reward dynamics that will determine whether it becomes a breakthrough infrastructure project in crypto or another casualty of DeFi.

Market position

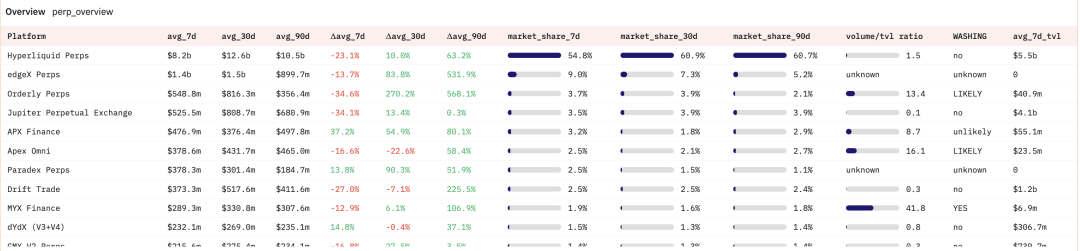

- Accounts for 70% of the total trading volume of decentralized perpetual contracts, and accounts for 9.9% of Binance’s daily trading volume

- 665,000 traders generating $300,000 USD per month (65 times the trading density of Binance retail users)

- The $4.4 billion USDC on the platform accounts for 71% of the USDC locked in the Arbitrum network.

Fundamentals

- Monthly revenue is $116 million, of which 97% is returned to ecosystem participants

- 38% of the total token supply (388 million HYPE) remains reserved for future growth incentives

- 24 validating nodes maintain network security vs Ethereum's 1 million+ (centralization vs. performance trade-off)

Competitive landscape

- Expect 15-25% wash trading (better than industry standards but still a concern)

- The market share of Binance perpetual contracts increased from 2.2% to 13.6% in 12 months.

- Jupiter platform's $32 billion in 60 days. Perpetual contract trading volume shows intensified competition on the chain.

While most people focus on token price appreciation, I analyze its underlying business sustainability through multiple market cycles (including bear market stress tests and competitive pressures).

- The 238 million tokens unlocked at the end of the year will create an average daily selling pressure of $17 million - equivalent to 8 times the current buyback capacity. Most bulls ignore this structural resistance.

- The $600 million allocation to Nasdaq-listed Treasury bonds and VanEck endorsement indicates non-retail demand that could absorb the unlocking pressure, but the timeline for institutional adoption remains uncertain.

- Zero gas fee transactions + 0.2 second latency + built-in order book form switching costs, but technical debt and consensus mechanism limitations may erode advantages

Hyperliquid may face user loss due to token depreciation and revenue compression, but its 97% fee rebate model and sustainable revenue generation capabilities make it a potential multi-cycle infrastructure project.

- Unlike traditional DeFi protocols that rely on token emissions or subsidized returns, Hyperliquid generates revenue from real economic activity and returns it almost entirely - demonstrating resilience when unsustainable revenue models collapse.

- It is expected to experience a 60-80% drop during the unlocking period from 2025 to 2027, but its business acumen and infrastructure advantages make it likely to rise strongly amid industry consolidation.

This article directly addresses the key factors that truly determine Hyperliquid's long-term success: a sustainable business model, competitive positioning, and the ability to survive multiple cycles of industry-wide existential crises.

Wat Happen?

Hyperliquid, as we all know, is a leading decentralized perpetual swap exchange (DEX) and is pursuing vertical expansion. It commands 60% of the decentralized perpetual swap market's trading volume, primarily driven by regulatory arbitrage opportunities, airdrops, an excellent user interface/user experience (UI/UX), deep liquidity, and strong community consensus.

Initial growth

Users can now use a perpetual contract exchange with a seamless UI/UX without undergoing KYC (but still needing to comply with regulations in different regions). This is due to:

#Zero Gas Fee and Low Transaction Costs

Unique order cancellation and post-only priority mechanisms outperform other order types (such as instant or cancel orders), significantly reducing the harmful effects of high-frequency trading (HFT) order grabbing by more than 10 times. For more technical details on how this is achieved, read the description of precompiles:

x.com/emaverick90/status/1919727174426284488

#Intuitive interface

One-click DeFi operation

#Superfast trading experience

0.2 second block time, achieving 20,000 TPS on the chain through a unique consensus model

#Excellent market maker and liquidity provider

Initially, it was launched by the Hyperliquid core team

In a cryptocurrency world where everyone is desperately seeking convenient leverage channels (such as meme coins, prediction markets, derivatives, altcoin beta, etc.) during a bull market, perpetual contracts have found a foothold with their simplest leverage access method and achieved product-market fit (PMF).

airdrop

Subsequently, their airdrop began to be distributed - this airdrop covered nearly 94,000 wallets, and each participant received an average of $45,000 to $50,000 worth of HYPE tokens:

- No selling pressure from insiders

- Widespread user ownership fosters loyalty and alignment of interests

It is worth noting that the Hypios community also provided extremely generous airdrops to its holders, and even meme coins on Hyperliquid (such as $BUDDY and $PURR) maintained low selling pressure and firm holders.

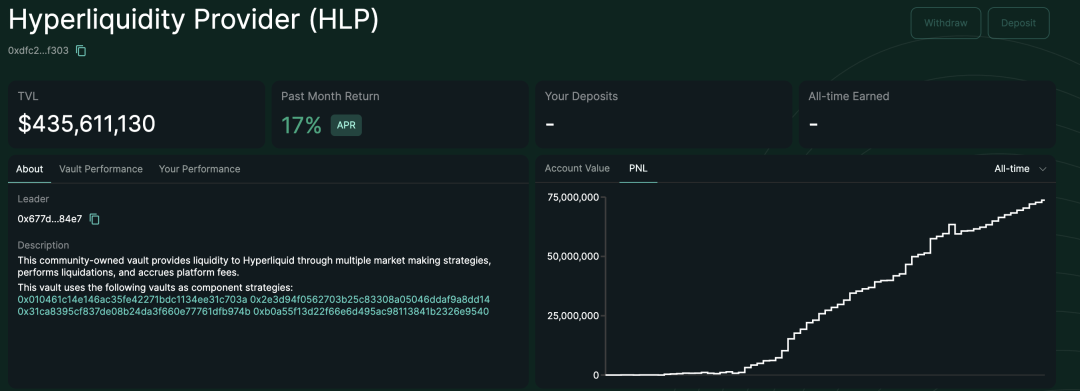

As traders/DeFi deep participants received tokens, many chose to stake (to reduce transaction fees) and deposit them into HLP vaults (https://hyperliquid.gitbook.io/hyperliquid-docs/hypercore/vaults/protocol-vaults), thereby improving the trading experience and starting a strong flywheel effect.

Heavy users continue to actively use the platform with their newfound wealth - fee income is used to repurchase tokens - strengthening product and market influence - Hyperliquid attracts more users and trading volume.

As a result, this massive distribution prevented HYPE from experiencing the price drop that typically follows an airdrop. In fact, over the following months, HYPE’s price surged 1,179%—rising from $3.90 at launch in November 2024 to $47 in August 2025.

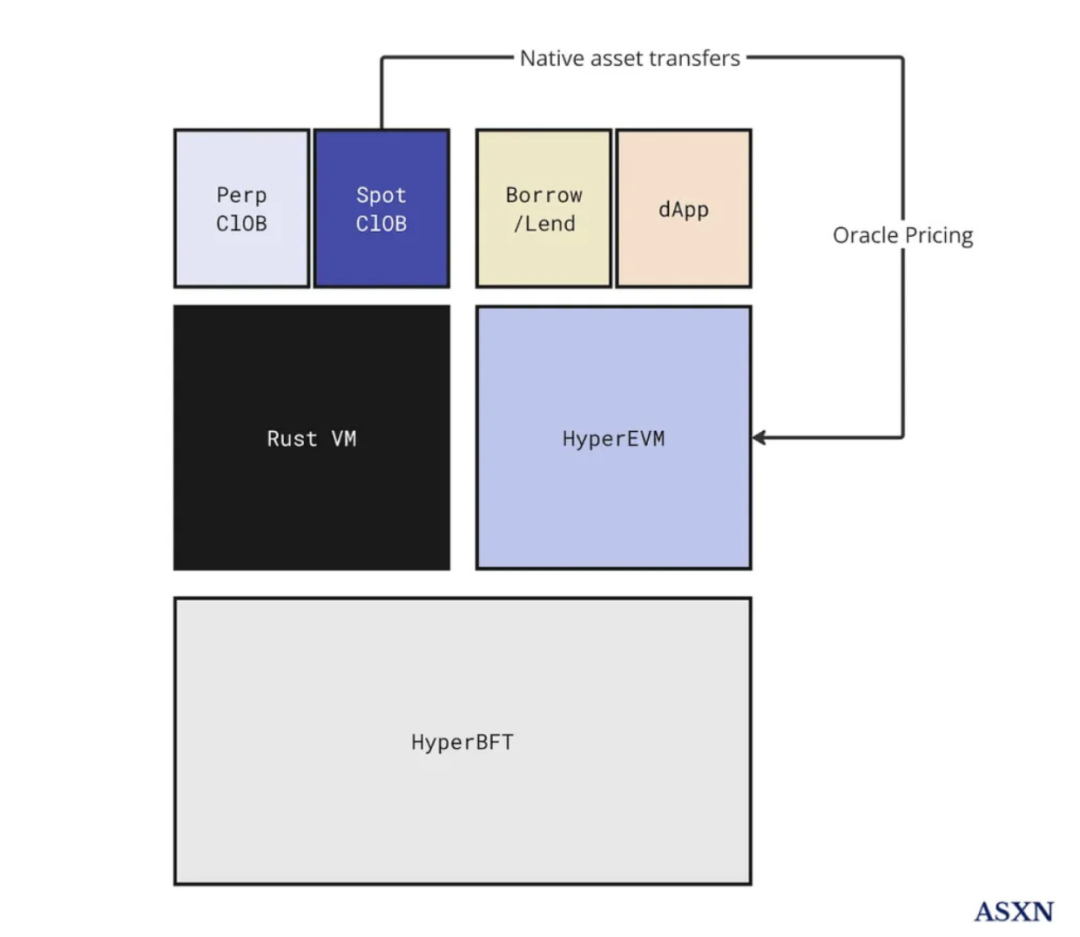

The HyperEVM

On February 18, HyperEVM was officially unveiled.

▲ Source: ASXN

It is not a separate chain, but is secured by the same HyperBFT consensus mechanism as HyperCore. The two share state and essentially use a Blob-free version of the Cancun hard fork.

Developers now have access to mature, liquid, and high-performance on-chain order books. For example, a project can deploy an ERC20 contract on HyperEVM using standard EVM development tools and permissionlessly deploy the corresponding spot asset in the HyperCore spot auction. Once linked, users can use the token in their HyperEVM applications and trade on the same order book.

This empowers developers and the community by supporting a wider range of use cases. It allows the broad user base and liquidity aligned with Hyperliquid to further make their mark on the ecosystem. It also creates another avenue for Hyperliquid usage to flow back to participants by providing a composable, programmable layer to improve liquidity.

Notably, this also provides a path for projects outside the Hyperliquid ecosystem to join. For example, Pendle has now integrated with HyperBeat, as well as Kinetiq's LST and LoopedHYPE's WHLP & LHYPE (https://x.com/looping_col/status/1955645499970560311). EtherFi and HyperBeat are launching preHYPE (https://thedefiant.io/news/defi/etherfi-expands-to-hyperliquid-ecosystem-through-collaboration-with-hyperbeat). Morpho offers a vault on HyperBeat, with top curators including MEV Capital, Gauntlet, Re7 labs, and many others.

HyperEVM's network effect isn't about cloning or EVM compatibility; it's about creating a programmable financial operating system where code, liquidity, and incentives are natively aligned and instantly accessible. Liquidity won't fragment; instead, it will grow exponentially as more use cases, revenue streams, and protocols are integrated. As the entire tech stack grows, users and developers alike benefit, making the Hyperliquid ecosystem the center of gravity for the future of DeFi.

Wat Now?

Hyperliquid already has all the liquidity and infrastructure it needs within an ecosystem of financialized individuals—farmers, quants, developers, traders, and more. So, how does it scale out from there?

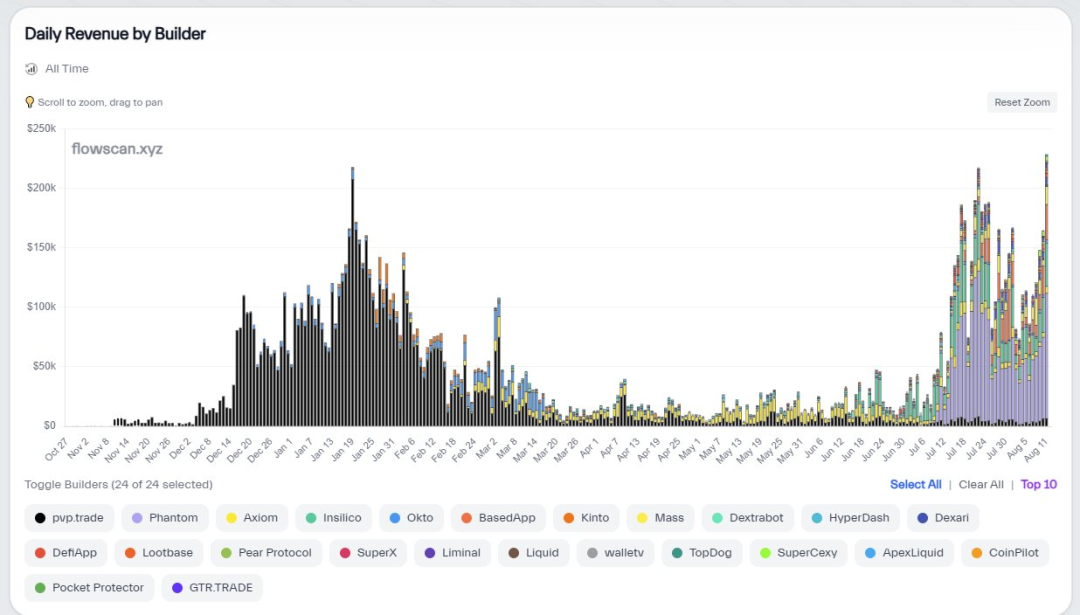

Builder Codes

Hyperliquid has released developer code (learn more: https://hyperliquid.gitbook.io/hyperliquid-docs/trading/builder-codes), allowing the platform to be integrated into any distribution channel and allowing those who do so to earn a share of the fees. For Phantom Wallet, which has 17 million users, this is undoubtedly a great opportunity to expand its wallet's use cases and increase revenue.

HIP Proposal Overview

Not only that, the Hyperliquid Improvement Proposal (HIP1, 2, 3) further promoted the vertical deepening of the technology stack.

- HIP-1 is a standard for deploying native tokens and on-chain spot order books.

Learn more: https://hyperliquid.gitbook.io/hyperliquid-docs/hyperliquid-improvement-proposals-hips/hip-1-native-token-standard

- HIP-2 aims to permanently inject liquidity into the spot order book of HIP-1 tokens.

Learn more: https://hyperliquid.gitbook.io/hyperliquid-docs/hyperliquid-improvement-proposals-hips/hip-2-hyperliquidity

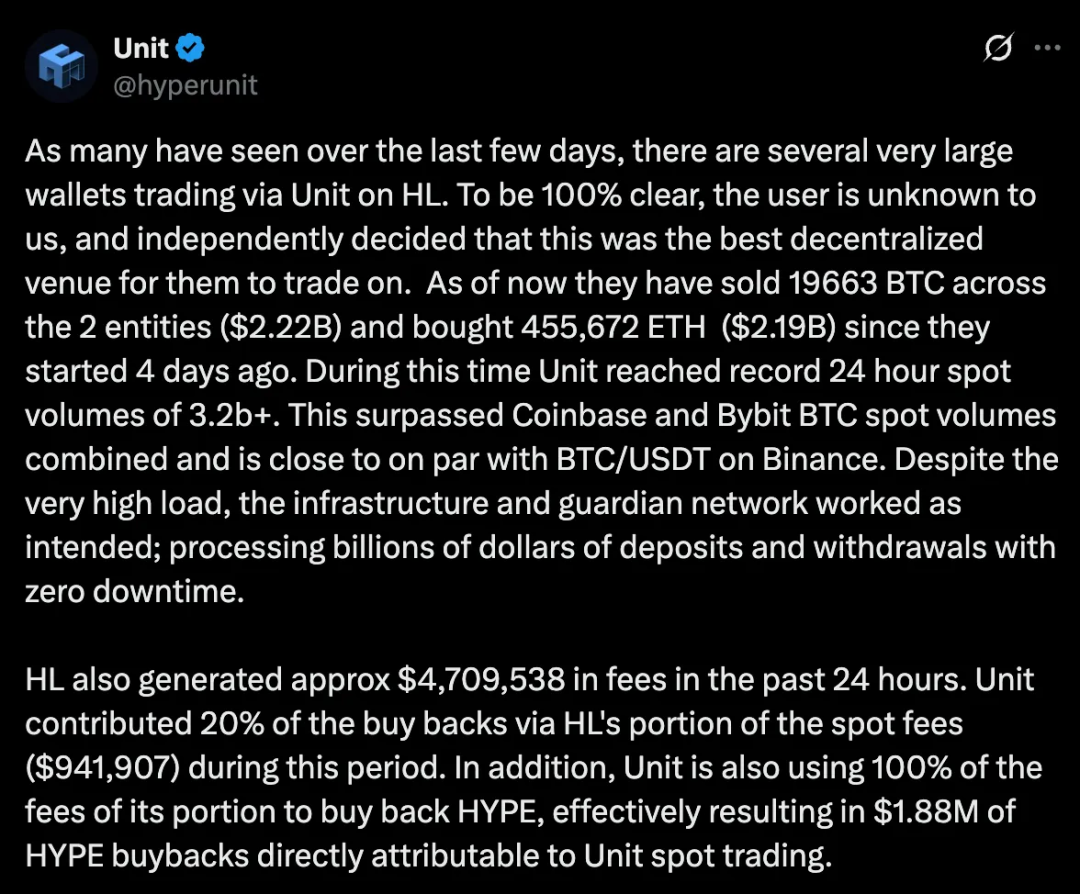

The Unit project is driving HIP-2 adoption by providing a more native spot trading experience. Essentially, Unit is a multi-sig wallet that allows traders to index native chains and conduct permissionless transactions on Hyperliquid. (Learn more: https://docs.hyperunit.xyz/)

But arguably the update that has caused the biggest buzz is HIP-3: https://hyperliquid.gitbook.io/hyperliquid-docs/hyperliquid-improvement-proposals-hips/hip-3-builder-deployed-perpetuals

HIP-3 introduces permissionless, developer-deployed perpetual contract markets on the core infrastructure. Before HIP-3, only the core team could launch perpetual contract markets, but now anyone who stakes 1 million HYPE can deploy their own market directly on-chain.

The process is as follows:

- Pledge 1 million HYPE

- Define market details: market name and ticker (still needs to be purchased via auction, similar to spot), select collateral type, oracle source and fallback logic, leverage and margin parameters, contract specifications, and funding mechanism.

- Set the fee structure (set the base transaction fee and any additional custom fees) and decide the fee share (up to 50%) for market deployers. Similar to the revenue sharing relationship between Binance and Circle.

- Deployment Market

Market operators are responsible for bootstrapping their own liquidity, while Hyperliquid receives the remaining 50% of the fees (which are then funneled back into the HYPE token). It's important to note that these markets don't appear directly on the Hyperliquid interface, but anyone can choose which markets to connect to. This makes Hyperliquid's role more like an asset provider than just a launchpad.

To date, Hyperliquid has successfully conquered the following core areas:

- High-performance trading engine: Provides a trading experience for spot and perpetual contracts that effectively mimics the performance of centralized exchanges.

- This includes leveraged trading and spot transfer capabilities.

- A consumer-grade user experience combined with distribution channels.

- EVM as a programmable execution layer: A programmable layer (HyperEVM) is built on top of it that is closely connected to the user experience and liquidity center.

- Stablecoin Infrastructure: Successfully attracted USDH worth $5.6 billion into its ecosystem.

There are still vast opportunities to explore for Hyperliquid itself or other projects in its ecosystem (based on HyperEVM):

- Native fiat currency deposit and withdrawal channels: Building a more convenient and low-cost bridge for fiat currency and cryptocurrency conversion.

- Payment Solutions: Leverage its high-speed, low-cost network to develop new payment applications.

- Web2-scale consumer applications: Develop sophisticated decentralized products that offer an experience comparable to traditional Web2 applications to attract a wider user base.

- Risk Management Engine: Creating better risk management and hedging tools for institutions and advanced traders.

Current state of tokens/liquidity

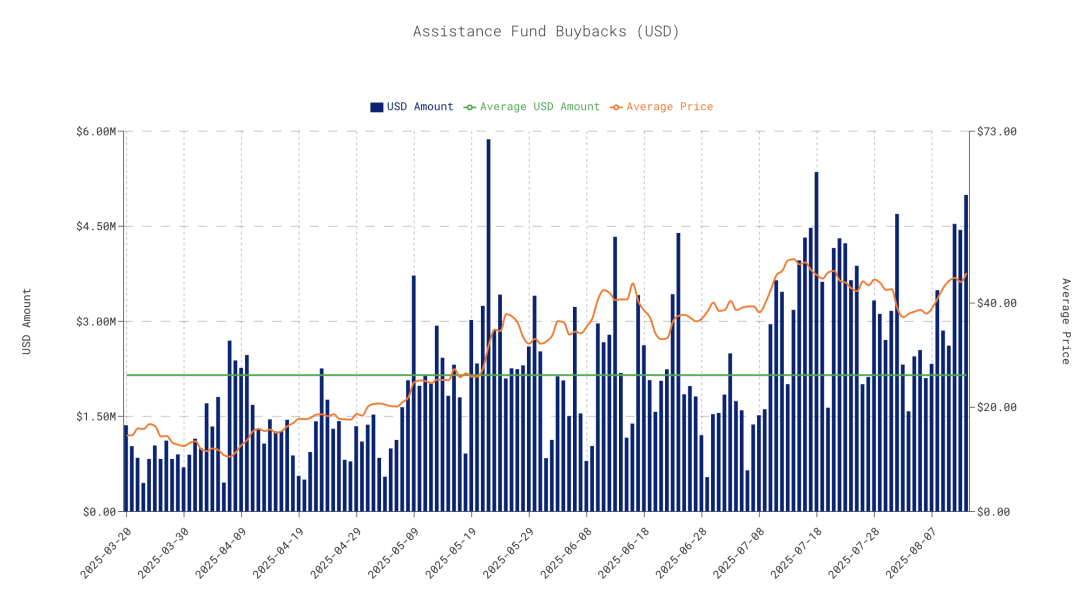

The repurchase plan led by the Assistance Fund shows that a total of 28 million HYPEs have been repurchased so far, with funds coming from 54% of the total revenue (46% of the perpetual contract fees are allocated to HLP depositors, which means that 92-97% of the total revenue is returned to users), with an average daily repurchase amount of US$2.15 million.

Currently, 38% of the total HYPE supply of 1 billion remains dedicated to airdrops and incentives, which has the potential to further drive ecosystem usage. However, this is a double-edged sword, as such a significant increase in circulating supply could generate significant selling pressure that far exceeds current buyback capacity.

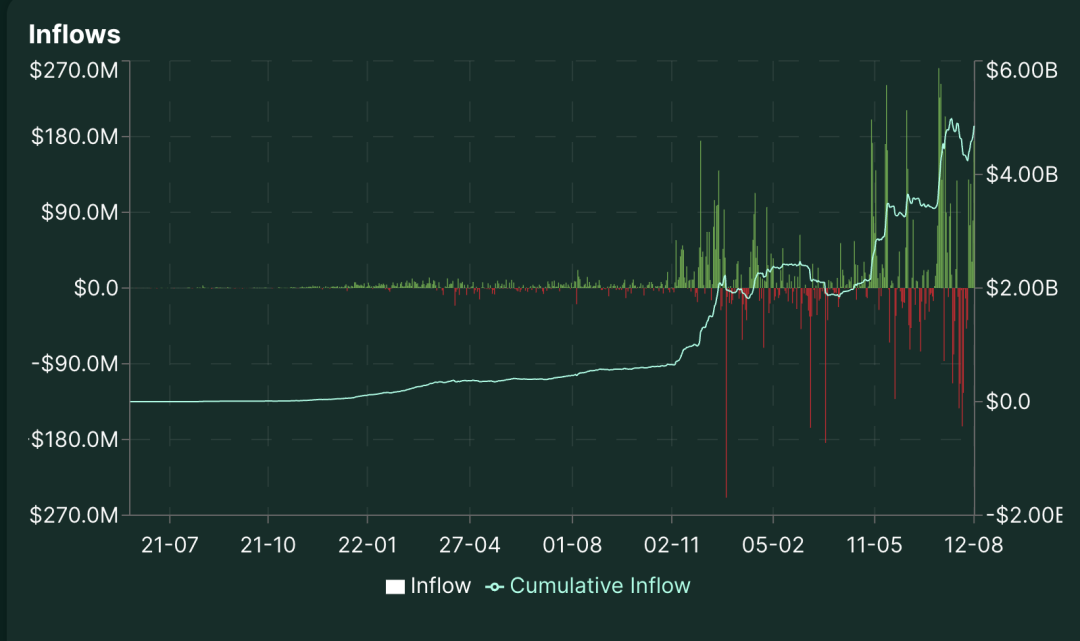

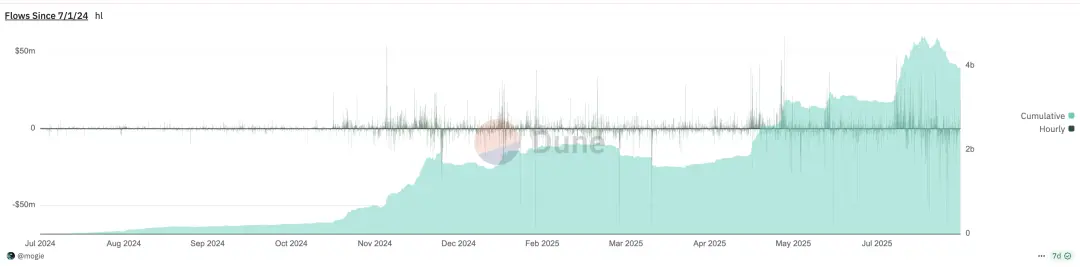

Hyperliquid continues to see growth in USDC inflows, currently holding approximately $4.4 billion. Surprisingly, this represents 71.11% of the total USDC locked on the Arbitrum network, with these funds being used to fund the Hyperliquid ecosystem.

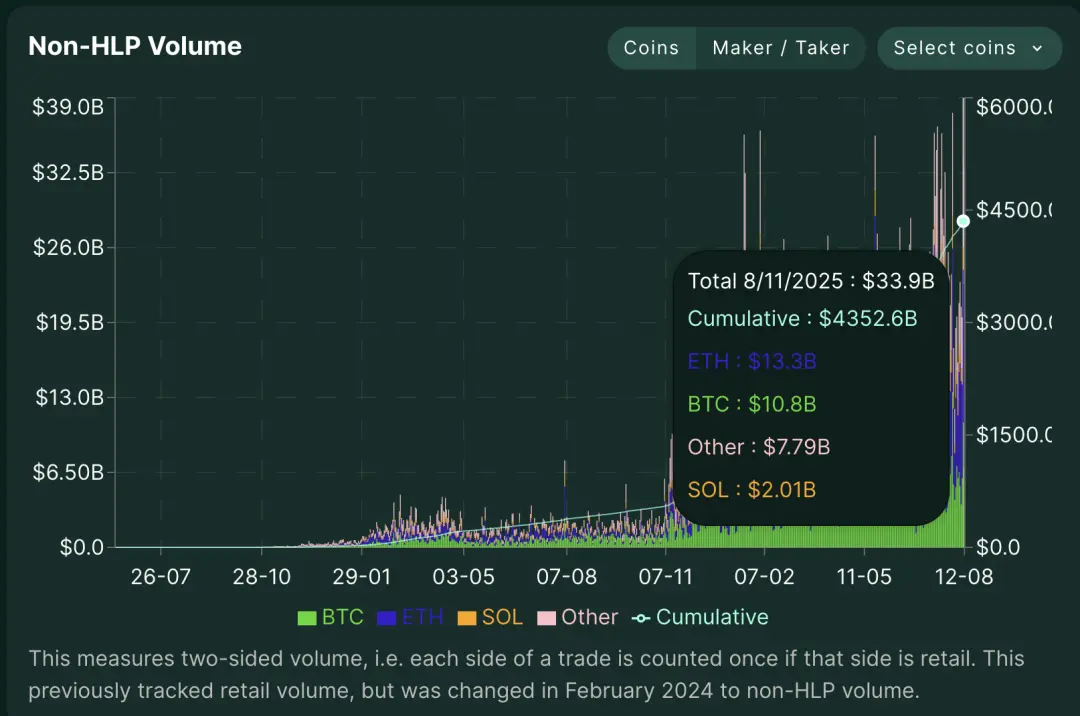

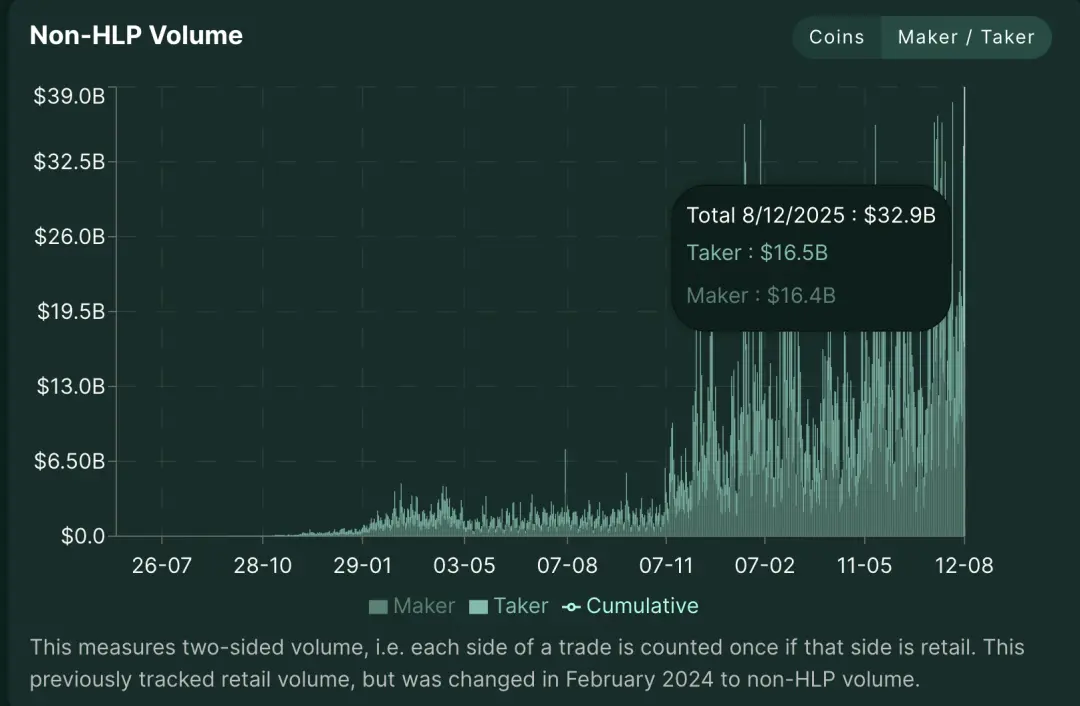

Using non-HLP trading volume (cumulatively $4.3 trillion) for analysis, since HLPs are passive liquidity providers/platform funding pools responsible for internalizing bookings and hedging risk, non-HLP trading volume represents peer-to-peer trading flows. It's important to note that this inter-peer trading flow also includes:

- Market Maker

- About 20% of accounts are regular transaction mining accounts and vaults using systematic strategies (see Appendix)

For an exchange, the increase in market makers is a “sweet problem.” In fact, Jeff once mentioned that there are already “too many” market makers.

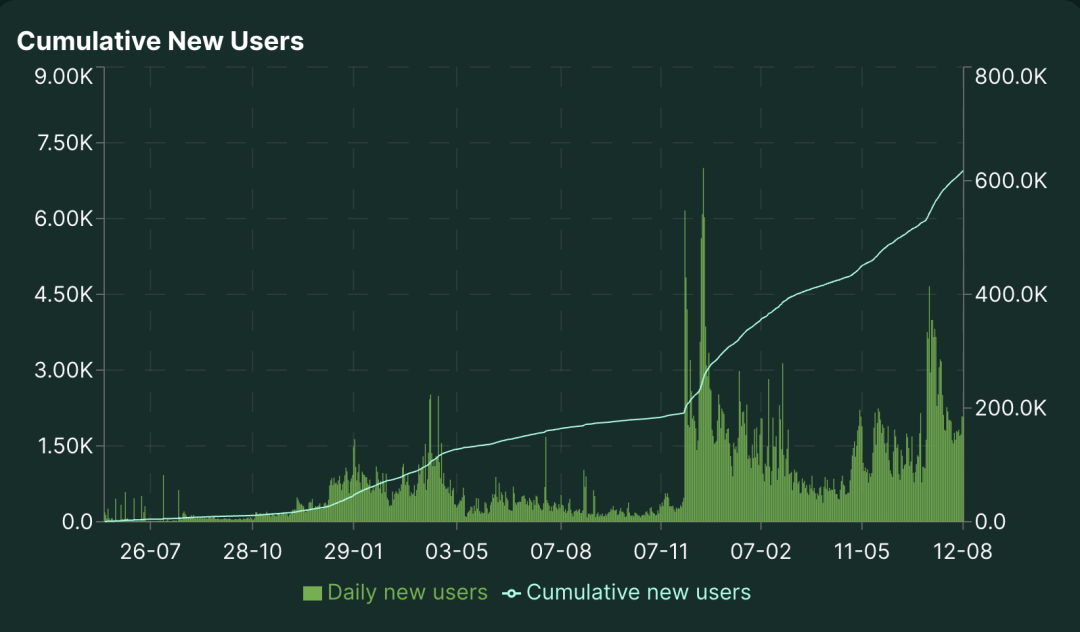

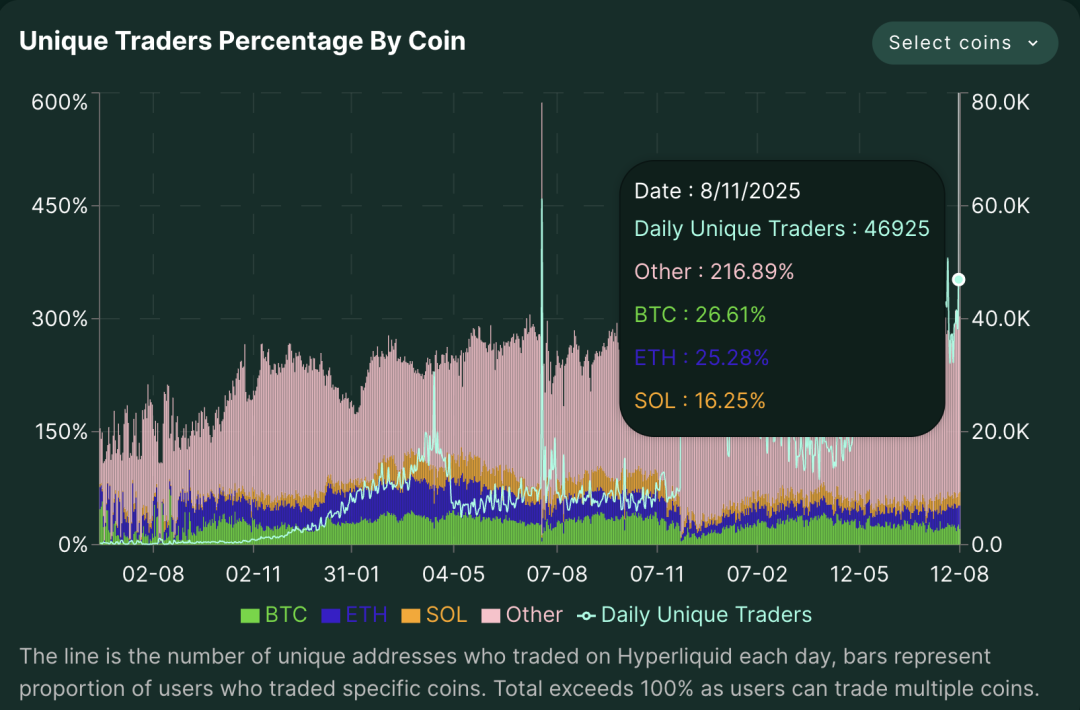

As of the analysis date, the number of daily unique traders reached 46,925. Statistics show that the percentage of currencies traded by users totals over 100%, as a single address trades multiple assets. This overlapping multi-currency trading suggests that Hyperliquid is more than just a single-asset trading venue—traders are exposed to multiple assets per session, demonstrating extremely high platform stickiness and cross-currency speculation. Meanwhile, the number of traders on Hyperliquid is growing fairly steadily.

So, what does this mean?

For now, everything seems heavily reliant on bringing users onto the HyperCore infrastructure and then returning value to the ecosystem in some way:

- HyperEVM will bring more transaction volume + a stable financialization layer to hyperliquid.

- Builder Codes help expand hyperliquid’s distribution channels, bringing fees back into HYPE tokens.

- HIP-3 will enable permissionless market creation and share fees with the HYPE token.

- Inflation of the HYPE token will benefit stakers and generally lead to higher returns for HyperEVM.

With the HYPE token serving as a perfect marketing tool and the best way to coordinate community development, Hyperliquid has fostered its own close-knit, cult-like community. Ultimately, if leveraged trading is a valuable experience for consumers, the flywheel effect will continue to grow.

Wat Next?

Bearish Case

#Possibility of tightening regulations

Perpetual contracts provide end users with access to leveraged markets. However, without robust Know Your Customer (KYC) and Anti-Money Laundering (AML) measures, this presents a risk of money laundering. Platforms may be forced to implement stricter compliance systems and report large trading activity. As with Polymarket, US users may eventually be required to undergo KYC before using the platform.

#Token Unlock

If not handled properly, the locked-up airdrop supply could trigger significant selling pressure.

- 238 million Core Contributor Tokens (23.8% of the total supply) will vest linearly starting November 29, 2025.

- Based on current prices, it is estimated that approximately $17.3 million in equivalent selling pressure will be generated per day between 2027 and 2028.

- Insider ownership will surge from the current 15.9% to 45.8% on a fully diluted basis.

Why it matters:

- The current repurchase capacity of the aid fund is only about $2 million per day.

- Forming a selling pressure 8.6 times the repurchase capacity

- The timing overlaps with the 2027-2028 Bitcoin halving down cycle

- Just to maintain price equilibrium, fee income needs to increase by 6-7 times

#Liquidity diversion risk

With the emergence of numerous new forms of distribution within Hyperliquid L1 (such as Builder Codes and the marketplace created by HIP-3), there is a risk that trading volume will shift to other markets. This risk exists even though fees will ultimately flow back into the HYPE token (although the share may be discounted) and Hyperliquid controls the core marketplace and distribution channels.

#The marginal decline of the buyback effect and the risk of flywheel rupture

Buybacks have diminishing returns on price. If Hyperliquid's adoption and product revenue don't match market demand for growth or the opportunity cost of holding other tokens, the growth flywheel could be broken (macro trends could also depress prices, as seen in April 2025). The mitigating factor lies in economic game theory: if the price falls back to a sufficiently low market capitalization, buybacks will consolidate and drive the price back up. However, the core risk lies in how many users are solely using the platform for the HYPE token.

#Security vs. Trust

While retail users appreciate Hyperliquid's user experience, they still prefer Ethereum as a storage option due to its larger validator set (800,000 vs. HL's mere 16), longer security record, and more severe penalty mechanisms (HL's consensus design is secure, but more centralized, with more concentrated penalty risks). Incidents like the $JELLYJELLY token have also raised questions about security and governance within the community.

#Lack of development funds

97% of fees go to buybacks, meaning zero funds are allocated for growth, marketing, or security incentives. Any attempt to divert funds to fund development through governance proposals would be doubly detrimental to token holders. While competitors actively fund ecosystem development, Hyperliquid is starving itself.

Bullish Case

#GrowthMomentum

- Attracting significant capital inflows through EVM integration and better interoperability

- The HIP3 market brings in traditional financial funds from institutions and retailers

- The number of perpetual contract markets on the main site continues to increase

- 38.8% of tokens are reserved for airdrops to provide growth opportunities

#USDH Earning Potential

The platform holds approximately $5 billion in USD deposits. The introduction of USDH, calculated at current US Treasury bond rates, could generate $150-200 million in annual revenue. If this revenue, previously retained by Circle, could be redirected to HYPE buybacks, it would be extremely beneficial to the ecosystem.

#Crosschain Expansion

Through LayerZero, you can deposit funds from any LayerZero chain with one click. Initial assets include USDT0, USDe, PLUME, and COOK. Breaking the single-chain barrier, we are the first to capture L2 order flow.

#Cost Advantage

- The current fee rate is about 2.8 basis points, while competitors' are about 1 basis point.

- Zero Gas Order + On-chain Matching Provides Sustainable Profit Model

- Remaining profitable even if fees are halved

#CEX Trust Crisis Opportunity

Centralized exchanges (such as FTX) have suffered from incidents that have damaged their image. As a semi-trusted, neutral infrastructure, Hyperliquid promotes blockchain concepts with a CEX-like experience, narrowing the gap in decentralized custody, operating costs, and regulatory arbitrage.

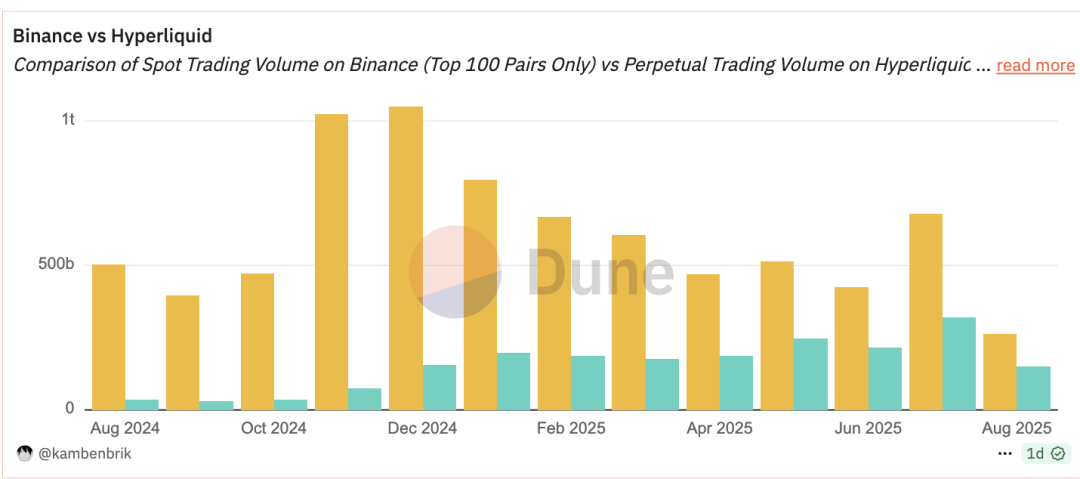

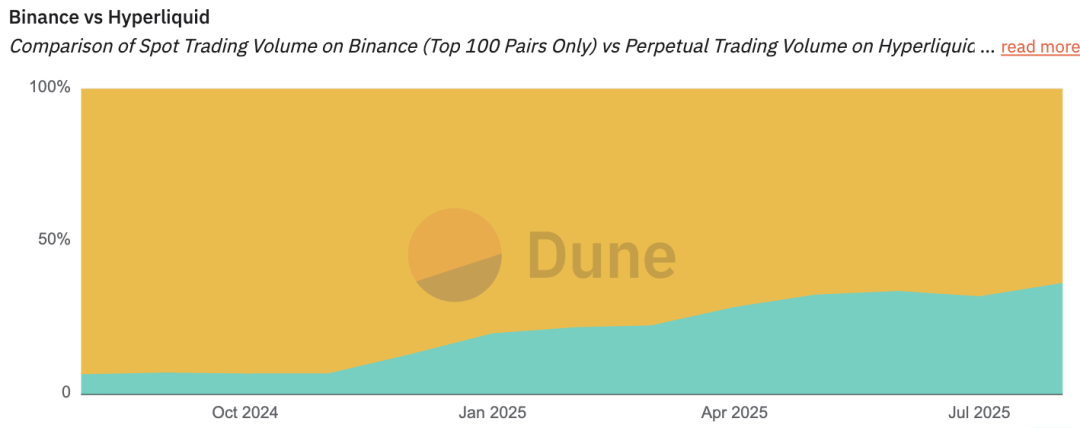

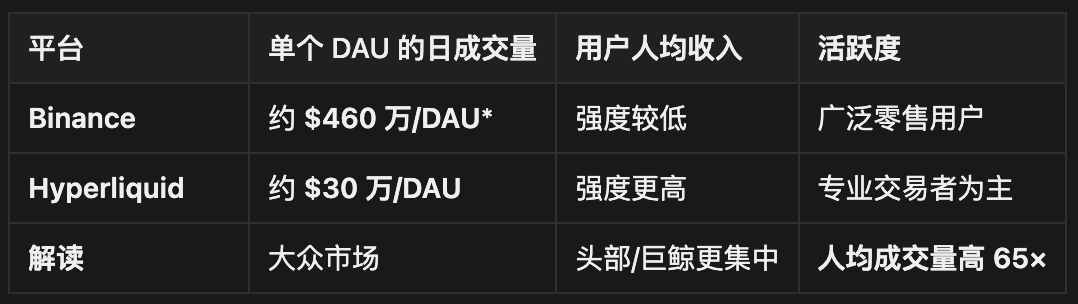

However, directly comparing spot trading volume to perpetual swaps trading volume is like comparing apples and oranges. If we want to clearly distinguish the actual market share of Binance and Hyperliquid (HL) in the spot and perpetual swaps markets, we can see the following:

#Daily Trading Volume (September 9, 2025)

#30-Day Volume

Estimated based on $730 billion in monthly trading volume and daily ratio provided by Messari

The two have completely different market positioning. One primarily serves off-chain users, while the other targets on-chain users. The figure below illustrates their dominance in their respective fields.

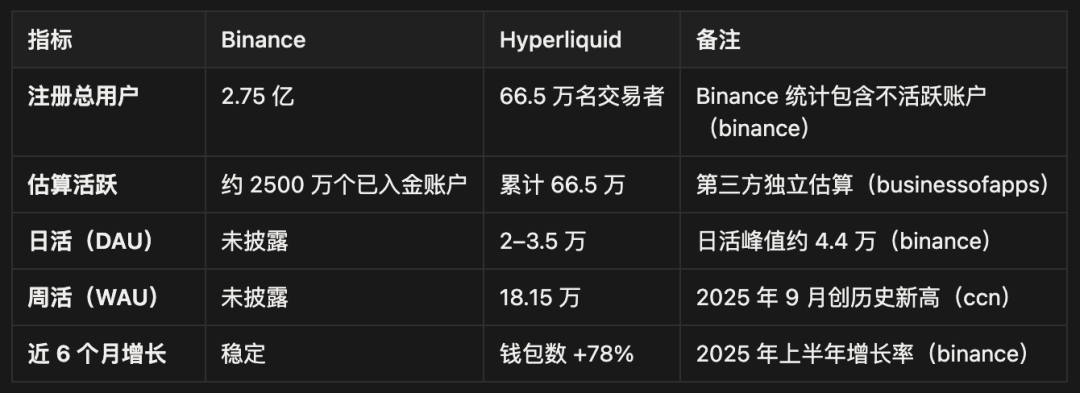

#User Base Analysis

Trading Intensity

Based on a rough estimate of 25 million active users

#Market Share

The many builders I've interacted with within the Hyperliquid ecosystem so far have all been dedicated, community-driven teams that create value. This atmosphere is largely due to the way the ecosystem has been guided, from product to airdrops and everything in between.

To bring cryptocurrency to the masses, the space needs to create new value and a better experience for potential new retail users. Fundamentally, I believe Hyperliquid can provide a lot of these products.

For example:

- An excellent trading interface (on-chain Robinhood): It can access on-chain liquidity while providing a seamless financial experience. If the crypto market wants to create a better financial structure, we also need a better interactive portal to abstract away confusing UI/UX.

- Pre-IPO Products: Following the $PUMP ICO/TGE (token generation event), we saw facilitated pre-markets on perpetual swap exchanges, allowing users to speculate on the asset while also providing better price discovery for the underlying asset. If replicated for pre-IPO assets, this would be a straightforward way to provide true value arbitrage (this tweet explains it well: https://x.com/j0hnwang/status/1947330391590752532).

- Addressing fragmentation: With the emergence of many new markets (HIP3, other CLOBs, etc.), we see the potential for liquidity and user experience to become increasingly fragmented. Projects like https://superstack.xyz offer a great solution, much like 1inch did for DEXs, Jumper did for cross-bridges, and Beefy did for yield farming.

- Real World Assets (RWAs): HIP3 provides a way for off-chain assets like SPX to be accounted for on-chain. Other forms of RWAs will provide more sustainable, income-backed returns and financial activities that will help drive the development of the ecosystem.

In short, Hyperliquid has taken a user-centric approach. From the core team's product decisions to the thousands of builders aligned with its vision, the entire ecosystem is designed so that the ultimate winners will be those who create value, not extract it. Newcomers now have an equal opportunity to prove their insights without the hassle of bad actors and access a rich and mature ecosystem. Whether any product can survive a bear market cycle is a mystery to anyone, but personally, I'm very optimistic about their ability to rebound and continue to attract more builders.

This isn't a bet that HYPE's price will rise or that earnings will remain high - it's a bet that building a real business with real users and real revenue will ultimately win, even if the path includes significant volatility and user churn.

The market will likely give you multiple opportunities to accumulate this thematic asset at distressed prices. The question is whether you believe that business acumen and sustainable revenue models are ultimately more important than short-term token plays in the long-term evolution of cryptocurrencies.

There is a lot of room for growth, but like any venture, I believe it is in the right hands.