Variational: Acting as the counterparty in the entire contract market

Variational does not produce liquidity; it merely acts as a transporter of liquidity.

After a lengthy introduction to the history of Hyperliquid, the details of its capital operations surrounding $HYPE, such as $USDH and DAT/ETF, will be covered later.

Binance's post-crisis public relations are becoming increasingly sophisticated, OKEx has taken the lead in carrying out internal purges, and Hyperliquid's upward trend continues unabated. Even if 1011 slowly wipes out a few market makers or the YBS project team, it is unlikely to harm these mainstream platforms, or even second- or third-tier CEXs/DEXs such as Lighter or Matcha. They have also shown resilience far exceeding that of previous crisis times.

Image caption: HL's revenue share

Image source: @RyanWatkins_

HL's rise after Aster and 1011 is unstoppable. Unless it collapses on its own or is shut down by regulators, it will be difficult for Binance to defeat HL in the same way it did FTX.

The cryptocurrency trading landscape has become solidified. What should Perp DEX, which arrived late to the game, do?

Market-level market maker: OLP handles everything.

Variational's approach is to link all liquidity. Variational predicts that no single company will dominate in the future, and even if one does, there will be third-party market makers on top of it.

As we mentioned earlier, both Binance and HL claim to be open to market makers, and even HL's HLP claims to account for only 1% of the trading volume.

The logic is not complicated. Just as Qualcomm sold its telecom business before being accepted by the entire industry, Visa/Mastercard would not start their own banks, and Stripe's Tempo probably will not issue a stablecoin.

Only with sufficient neutrality will it be actively accepted by all market participants.

If Hyperliquid's Builder Codes are the front end of liquidity, then Variational's OLP is the counterparty of all market makers.

Strictly speaking, Variational is not a traditional Perp DEX. On the one hand, it has a highly centralized nature. Under the RFQ architecture, users actively inquire about prices, and the only market maker, OLP, provides the quotes. The order details are pre-set by Variational, and the final matching price is also determined by OLP.

Note:

CLOB addresses the slippage issue in AMM and reappears in Variational under the RFQ mechanism, but it allows setting limit orders to compensate for this deficiency.

However, there are also advantages. Every order a user places must be accepted by a counterparty, ensuring an absolute balance between long and short positions in the market. Furthermore, every order is insured through an OLP contract, ensuring that profits and losses are shared and independent of others.

Moreover, OLP is the only market maker on Variational, meaning there are no third-party market makers. Every user needs to trade with OLP, which is to ensure the smallest possible balance in the market.

The advantage of doing this is that in the event of extreme liquidation, your profits are only responsible for the losses of the counterparty to your order, and not for the losses of other orders, thus maximizing control over the amount of liquidation on Variational.

However, this does not prevent the spread of liquidation in the overall market, which does not contradict the above. Note that OLP is the only counterparty for users on Variational, but OLP does not exclusively make markets on Variational.

Image caption: OLP operating mechanism

Image source: @variational_io

Besides the common practice of OLPs earning returns and handling clearing, the biggest difference between OLPs and HLPs is that OLPs hedge on DEXs/CEXs in the market.

For example, if Alice opens a long position on OLP but cannot find a corresponding short position to match it, OLP will directly open a corresponding short position on BN/HL to achieve its own balance.

Therefore, Variational is not like a Perp DEX, but rather like a market maker such as WinterMute. What it opens up is not liquidity, but market maker access permissions.

For HLP, users' deposits need to earn market-making revenue, but HLP cannot excessively seize market traffic, otherwise ordinary users and market makers will leave.

However, OLP is the only market maker; users either deposit OLP or become its counterparty, naturally excluding the participation of market makers.

In 1011, market makers have their positions coupled on Binance and on-chain. When a crisis occurs, multiple market makers will create a stampede effect, causing the market crisis to spread indefinitely. OLP does the opposite and will close and liquidate positions according to predetermined conditions.

For Binance and HL, OLP would be a better market maker option, at least reducing the chance of them "running away" during a crisis. OLP is unique on Variational, but for other exchanges, it is a major client.

Remember this: OLP positions are in an absolutely balanced P2P model, and each user's position is only accountable to the counterparty.

Loss rebates are customer acquisition costs

How to participate and consistently profit during a period of intense competition in the Perp DEX market.

Variational targets BN/HL, which allows third-party market makers to exist, and where retail investors are powerless against market makers and super platforms. OLP acts as an open market maker, allowing users to participate in OLP without trading if they want to obtain passive income from Perp DEX.

But is that really the case?

Image source: @TurboFlow_xyz

Lighter's loss rebates haven't stopped, and TurboFlow Perp, an exchange that has transformed into an AMM mechanism, is already offering zero trading fees/no slippage, and the exchange only shares profits when users make a profit.

1011's loss rebate mechanism is very efficient, but Variational's loss subsidies have become the norm, which is the direct reason why it has attracted market attention after the major liquidation.

In a sense, Lighter's loss subsidies, Binance's $200 million compensation and the "Together We Go" program, and the potential Hyperliquid S3 trading credits are all customer acquisition strategies.

However, the loss-making subsidies indicate that the cost of this customer acquisition channel is approaching the edge of marginal benefit. If the project owner has to acquire customers even if they are not profitable, it means danger.

Variational is normalizing this danger and using it as a routine customer acquisition method.

OLP is not only the sole market maker, but also a counterparty that does not charge transaction fees. OLP's profit comes from the market-making spread, meaning that "BN/HL is too powerful and will prioritize liquidating user positions, but OLP uses a black box to ensure the rights of retail investors."

Yes, OLP's market-making mechanism remains opaque, and OLP is still controlled by the project team. Retail investors don't need to believe that OLP won't intentionally cause them to lose money, because OLP will subsidize losses.

OLP will satisfy the interests of OLP depositors while maintaining a neutral market-making strategy.

In addition, OLP is the counterparty of all traders, which can control the interference of whales in the market to a certain extent. Situations such as hijacking HLP arbitrage will occur less often because OLP is less open. In extreme cases, whale positions can be shut down directly.

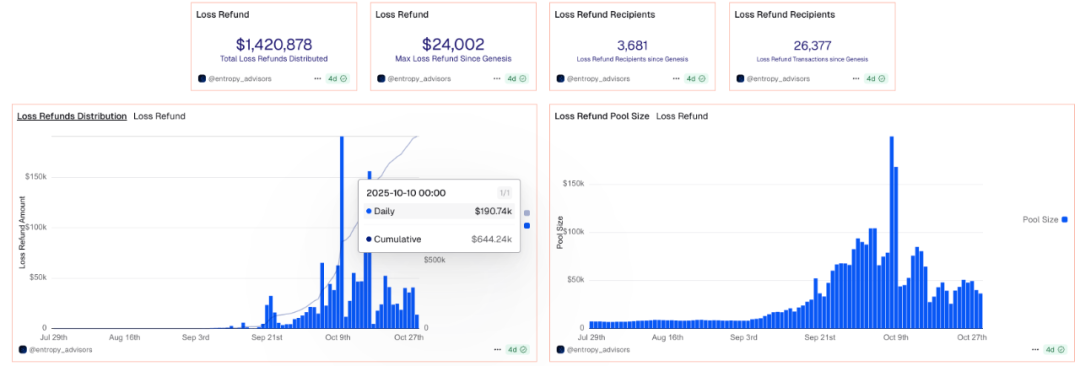

Image caption: Variational loss subsidies peaked in 1011.

Image source: @variational_io

However, it should be noted that the current trading volume of Variational is still relatively small compared to HL/BN, and its ability to ensure subsidies after the increase in market making volume needs to be verified by the market.

Conclusion

The era of decentralization is over.

Before Variational, market liquidity was underground and decentralized, but Variational brought retail investors into the mix, challenging market makers and large trading platforms.

• From the user's perspective: OLP controls the liquidation efforts, but it cannot fundamentally resist overall market changes; at best, it provides some peace of mind.

• From the project team's perspective: They attract user deposits to hedge positions on BN/HL, and increase their trading volume by offering free services and APR.

• BN/HL perspective: Increase institutional-level market makers and serve as a bridging channel to leverage overall market liquidity.

However, Variational exchanges are too opaque, and retail investors are still powerless to resist them. This may be the helplessness of retail investors in this era. Coinbase, representing US-based exchanges, has taken the lead in becoming institutionalized, following in the footsteps of US stocks.

The on-chain and Asian markets are the only remaining retail markets, and it remains to be seen whether they will give rise to Frankenstein or a new cyberpunk concept.