Author: Stacy Muur

Compiled by: Chopper, Foresight News

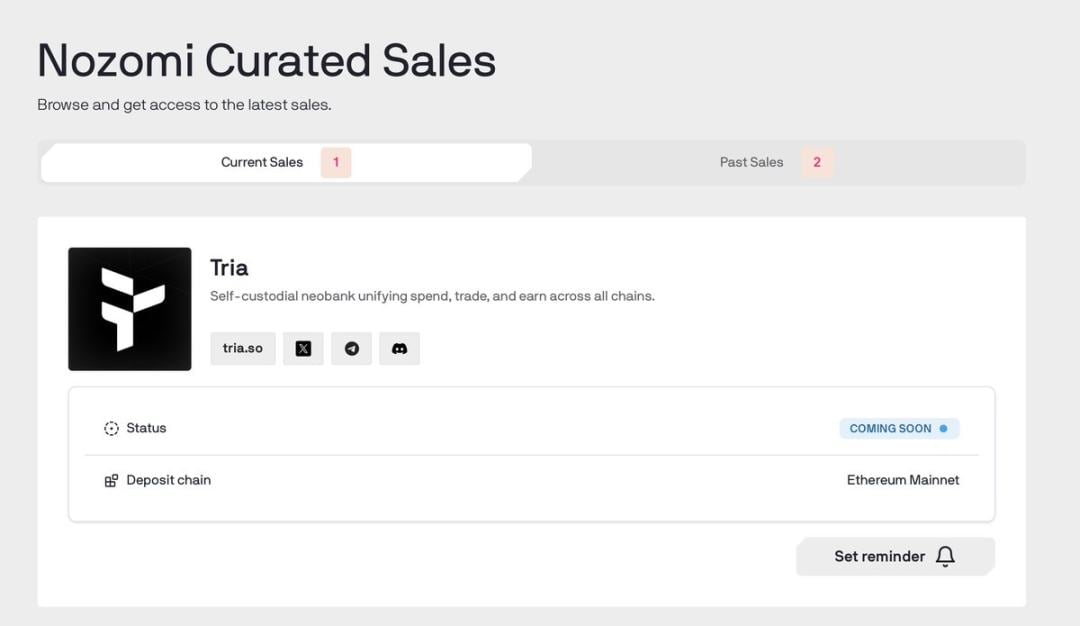

Tria is a non-custodial new banking application that allows users to spend, trade, and earn rewards across more than 100 blockchains, all without gas fees and without the need for mnemonic phrases. It will launch its "contribution-based offering round" on Legion's Nozomi blockchain on November 3rd.

Tria Investment Logic

Tria's core logic is simple. It is projected that by 2030, on-chain transaction volume will approach $100 trillion, but the bottleneck in the industry is not profitability or liquidity, but ease of use.

Stablecoins have surpassed $1.1 trillion in monthly settlement volume, exceeding Visa and Mastercard, but most people still cannot use cryptocurrencies in everyday scenarios. Tria addresses this issue with a new banking solution that abstracts away the complexities of cryptocurrencies through cross-chain mechanisms: it hides the technical complexities of cryptocurrencies while retaining their non-custodial nature.

Tria's product highlights are:

- Spending: Supports Visa card payments in over 150 countries, with cash back up to 6%, and zero transaction fees for deposits, withdrawals, payments, and foreign exchange transactions;

- Returns: Idle assets can yield up to 15% annualized return, which can be used to automatically pay off bills;

- Transactions: A single interface covering over 100 chains, with built-in AI narrative tracking capabilities—powered by BestPath AVS.

- After 11 weeks of closed beta testing: $1.2 million in revenue, $15 million in transaction volume, 20,000 users, and 4,400 affiliate members; average revenue per user was $105 (approximately twice that of Phantom). BestPath has been adopted by more than 70 protocols (such as Arbitrum, Polygon, Injective, and Sentient) and has reached more than 250,000 users through integration.

Tria enables cryptocurrency to be "use and go," demonstrating innovation in the following aspects.

- BestPath AVS (Intent Market): Solver, repeater, liquidity router, and fast finality layer compete with each other to match the optimal execution path for each transaction. The system scores transactions based on cost, speed, and security to ensure optimal settlement without the need for cross-chain bridges.

- Unchained (AVS Layer 2 → Layer 1): A consumer-oriented execution environment compatible with EVM, which will be upgraded to a Layer 1 network in the future—optimized for payment and agent interaction scenarios;

- Multi-virtual machine support: compatible with EVM, SVM, IBC, Move, and BTC, providing a single software development kit (SDK) to achieve a "chain-less" user experience.

Tria's ultimate goal is to build a "chain-agnostic" financial operating system that retains non-custodial characteristics, simplifies the usage process, and enables large-scale adoption by mainstream users.

Nozomi support

Tria is not just a product launch, but also a prime example of Nozomi's "fair, compliant, contribution-based" model.

Unlike traditional offerings that are "only for venture capitalists and have inflated valuations," Nozomi uses a "Legion scoring" mechanism to allocate participation eligibility based on on-chain activities, community contributions, influence, and expertise.

How should the sales quota be allocated?

- Purchase any Tria card using the discount code (enjoy a 20% discount) and unlock your credit limit.

- Complete KYC verification at Legion;

- Submit the priority quota form;

- Actively using the cards can unlock airdrops. (Note: There is already over $30 million in interest, and the release is highly likely to be oversubscribed.)

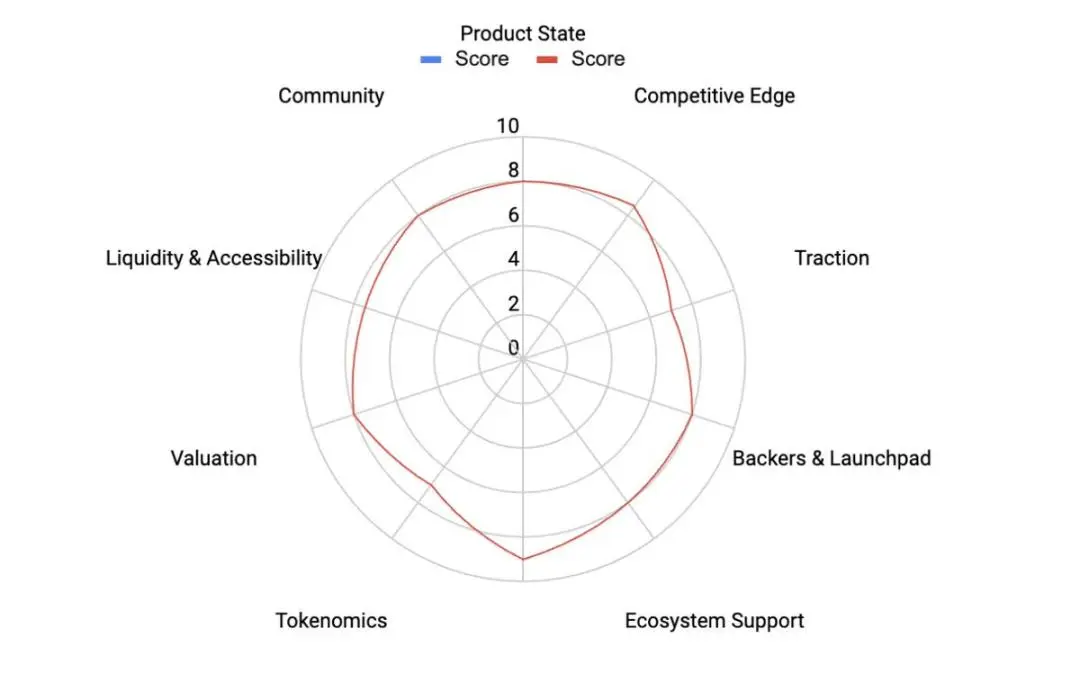

My evaluation framework

The Muur Score framework focuses on the core dimensions of a project: product, token design, user growth, investors, and market environment, and scores them by importance.

For Tria, the evaluation dimensions include:

- Products: Seamless new banking experience, BestPath AVS + Unchained infrastructure, closed test data;

- Token economics: functionality and use, allocation/unlocking mechanisms, and issuance valuation;

- Community and Narrative: Affiliate Marketing Networks, Organic Spread Popularity, and Trends in the New Bank/Intent Layer Track;

- Distribution model: Legion's contribution-based issuance mechanism and card-locked quota channel.

Overall rating: 8.21/10. Tria has real revenue, clear differentiated advantages, and a collaborative distribution model, but uncertainties remain in execution aspects such as scalability compliance, liquidity management, and multi-virtual machine routing.

Token Economics

Tria will launch its community sale on the Legion platform on November 3rd. The fully diluted valuation (FDV) for this sale is divided into two tranches: $100 million (30% unlocked) or $200 million (60% unlocked). The unlocking mechanism is a 2-month lock-up period followed by a 6-month linear unlock.

The uses of TRIA tokens include:

- Used for settlement between BestPath and the new banking ecosystem;

- Discounts on payment processing fees (Gas fees/transaction fees/card fees);

- Staking makes you a "Pathfinder";

- Ecological reward allocation and governance voting;

- Structured buyback and destruction of revenue from the agreement.

The token launch date (TGE) is planned for the fourth quarter of 2025.

Token Economics Assessment

- Functionality and Usage: 9/10 — It provides indispensable support for both consumer and infrastructure needs;

- Structural design: 7/10 — The lock-up period and unlocking pace are balanced, but a complete unlocking curve and audit report are still pending.

- Valuation level: 8/10 - $100-200 million FDV is undervalued compared to similar payment/infrastructure projects.

- Liquidity: No rating given for TGE yet; trading is expected to begin after Legion launch, with market makers providing deep liquidity.

Risk Warning

Tria's business prospects face the following challenges:

- Compliance risks: Compliance registration for card/deposit channels needs to be completed in more than 150 countries, which is quite difficult;

- Execution risks: Simultaneously advancing consumer-grade banking services and multi-virtual machine infrastructure leads to high business complexity;

- Competition risk: New custodian banks may quickly imitate its functions, requiring continuous maintenance of user experience and fee advantages;

- Liquidity risk: Short-term liquidity after launch depends on the Legion offering and allocation, unlocking pace, and market maker depth.

Valuation Reference

The FDV of similar payment/consumer infrastructure projects after launch is typically between $350 million and $1 billion, and most of them have weak revenue before launch.

Tria is priced at $100-200 million FDV. Although it is benchmarked against high-potential TGE infrastructure projects, it already has real revenue and users, and the token has dual uses in the consumer and infrastructure sectors, making its valuation highly cost-effective.

Even if only a tiny fraction of Revolut's scale (e.g., 1% of its $4 trillion annual transaction volume) is used, it would mean billions of dollars in on-chain transactions being routed through BestPath/Unchained, representing a huge potential for growth.

Summarize

Catalyst: Legion launched on November 3rd, having already garnered over $30 million in funding before its release;

Core mechanisms: BestPath AVS provides the lowest cost and fastest cross-chain execution; Unchained gradually upgrades from an AVS Layer 2 network to a Layer 1 network;

Release Rules: Purchase a Tria card to lock in your spending limit (card tiers: $20/$90/$225); active use will earn you an airdrop; a priority form must be submitted.

Risk warning: Compliance pressure in more than 150 countries, token liquidity after launch, and the complexity of simultaneously advancing consumer and infrastructure businesses.

My rating: 8.21/10. If Tria can maintain its revenue growth momentum during the public beta phase and successfully complete global compliance filings, it may become a "Revolut moment" in the crypto world, while adding another benchmark case to Legion's contribution-based sales model.