Written by: kkk

On July 31st, Paul Atkins, Chairman of the U.S. Securities and Exchange Commission (SEC), announced a far-reaching new policy initiative: "Project Crypto." This blockchain-based reform initiative, led by the SEC, has a clear goal: to completely rewrite U.S. regulatory oversight in the era of crypto assets, move financial markets onto blockchain, and realize the Trump administration's ambitious vision of making the United States the "crypto capital of the world."

The past model of "using law enforcement instead of regulation" not only drove innovative cryptocurrency companies to Singapore and Dubai, but also missed the opportunity for the United States to lead the next generation of financial infrastructure. The launch of "Project Crypto" departs from the regulatory repression of the past few years and undoubtedly sends a strong signal to the entire industry: America's on-chain era begins now.

With the relaxation of regulations, DeFi protocols such as Uniswap and Aave have entered a golden window

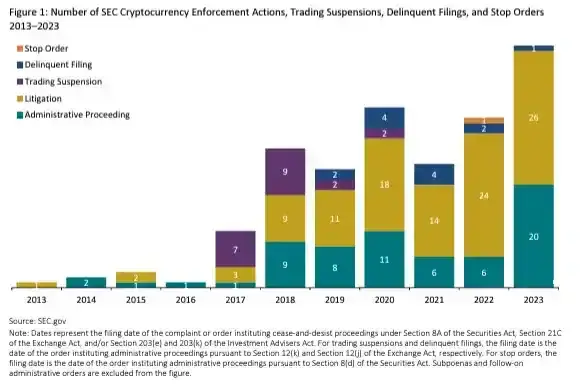

The attitudes of successive chairmen of the U.S. Securities and Exchange Commission (SEC) toward crypto assets and their derivatives—particularly DeFi (decentralized finance)—often determine the temperature and activity of the U.S. market. During Gary Gensler's tenure, the SEC's regulatory strategy centered on a "securities definition first" and "enforcement-first" approach, emphasizing the full integration of token trading into the traditional securities framework. During his tenure, he facilitated over 125 crypto-related enforcement actions involving numerous DeFi projects, including a subpoena against Uniswap and a lawsuit against Coinbase, pushing the compliance threshold for on-chain products to a near-record high.

After the new chairman Paul Atkins took office in April 2025, the SEC's regulatory style underwent a fundamental change. He quickly launched a special roundtable entitled "DeFi and the American Spirit" to relax DeFi regulations.

In Project Crypto, Atkins explicitly stated that the original purpose of US federal securities laws is to protect investors and ensure market integrity, not to curb technological architectures that eliminate the need for intermediaries. He believes that decentralized financial systems such as automated market makers (AMMs) inherently enable disintermediated financial market activities and deserve their proper institutional status. Developers who "just write code" should be provided with clear protections and exemptions, while intermediaries that wish to provide services based on these protocols should have clear and enforceable compliance paths.

This shift in policy thinking undoubtedly sends a positive signal for the entire DeFi ecosystem. In particular, protocols like Lido, Uniswap, and Aave, which have already established on-chain network effects and boast highly autonomous designs, will gain institutional recognition and development space under the decentralized regulatory framework. Protocol tokens, long plagued by the "securities shadow," are also expected to reshape their valuation logic amidst easing policies and the return of market participation, reclaiming their place as mainstream assets in the eyes of investors.

Building the Next Generation of Financial Portals: Super-Apps Will Reshape the Competitive Landscape of Trading Platforms

In his speech, Paul Atkins proposed the "Super-App," a highly realistic and transformative concept. Atkins argued that current securities intermediaries face complex compliance structures and overlapping licensing barriers when offering traditional securities, crypto assets, and on-chain services, which directly hinder product innovation and user experience upgrades. He proposed that future trading platforms should be able to integrate a variety of services under a single license, including non-securities crypto assets (such as $DOGE), securities crypto assets (such as tokenized stocks), traditional securities (such as US stocks), and staking, lending, and other services. This is not only a compliance innovation that streamlines processes but also lies at the core of the competitiveness of future trading platform companies.

Regulators will drive the true implementation of this super-app architecture. Atkins has explicitly instructed the SEC to draft a regulatory framework that will allow crypto assets, regardless of whether they constitute securities, to coexist and trade on SEC-registered platforms. The SEC is also evaluating how to leverage its existing authority to relax listing requirements for certain assets on unregistered exchanges (such as those with only state licenses). Even derivatives platforms regulated by the CFTC are expected to incorporate some leverage functionality to unlock greater trading liquidity. The overall direction of regulatory reform is to break down the binary distinction between securities and non-securities, allowing platforms to flexibly allocate assets based on the nature of their products and user needs, rather than being constrained by compliance structures.

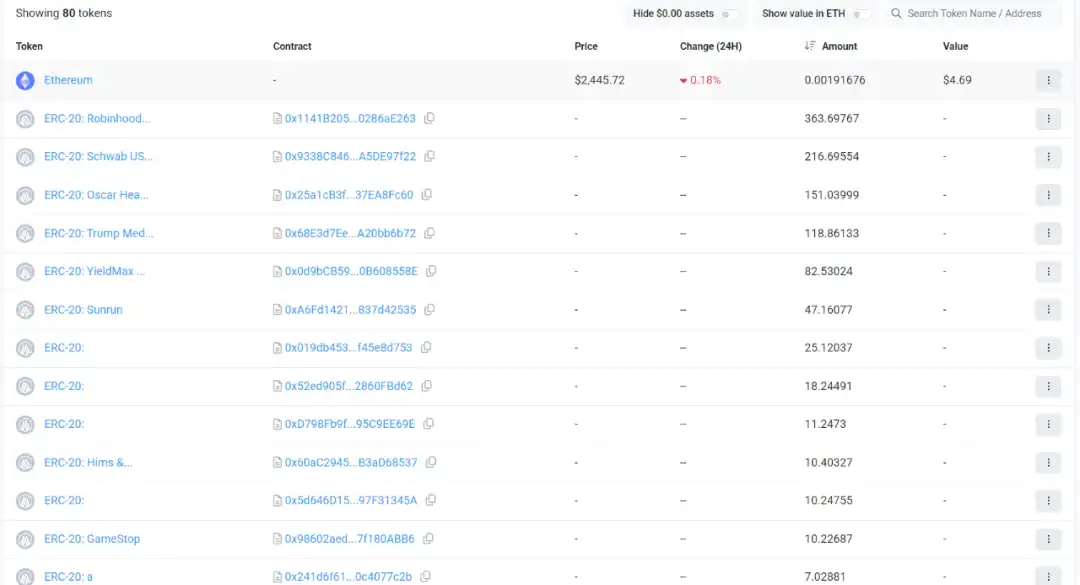

The most direct beneficiaries of this change are undoubtedly Coinbase and Robinhood. These two companies have already established a diversified trading structure, covering mainstream crypto assets, operating traditional securities exchanges, and providing lending and wallet services. Encouraged by Project Crypto, they are expected to be the first platforms to reap the benefits of this policy—providing a one-stop service and connecting on-chain products with traditional user bases. Notably, Robinhood completed its acquisition of Bitstamp this year and officially launched tokenized equity trading, listing US stocks such as Apple, Nvidia, and Tesla in ERC-20 format. This move is a preview of the Super-App model: using on-chain protocols to provide a traditional stock trading experience without disrupting familiar user experiences.

Coinbase, for its part, is promoting a developer ecosystem through the Base Chain, attempting to integrate exchange, wallet, social, and application-layer services. If Coinbase can integrate traditional securities with on-chain assets at the compliance level, it has the potential to become a "Charles Schwab on-chain" or a "next-generation Morgan Stanley"—not just an asset gateway, but a complete financial instrument distribution and operations platform.

It's foreseeable that once the Super-App architecture is fully implemented, it will become a core battleground for trading platforms. Whoever can first achieve compliant "multi-asset aggregate trading" will be at the forefront of the next round of financial infrastructure upgrades. As regulatory stances become increasingly clear, platforms are accelerating their entry into the market. For users, this means a smoother trading experience, a richer product selection, and a financial world that's closer to the future.

ERC-3643: From technical protocol to policy template, a compliance bridge for the RWA track

Regarding RWA, Paul Atkins explicitly stated in his speech that he would promote the tokenization of traditional assets and singled out ERC-3643 as a token standard worthy of reference in regulatory frameworks. This was the only token standard publicly mentioned throughout the speech, signifying that ERC-3643 has leapt from a technical protocol to a policy-level reference model, and its importance is self-evident.

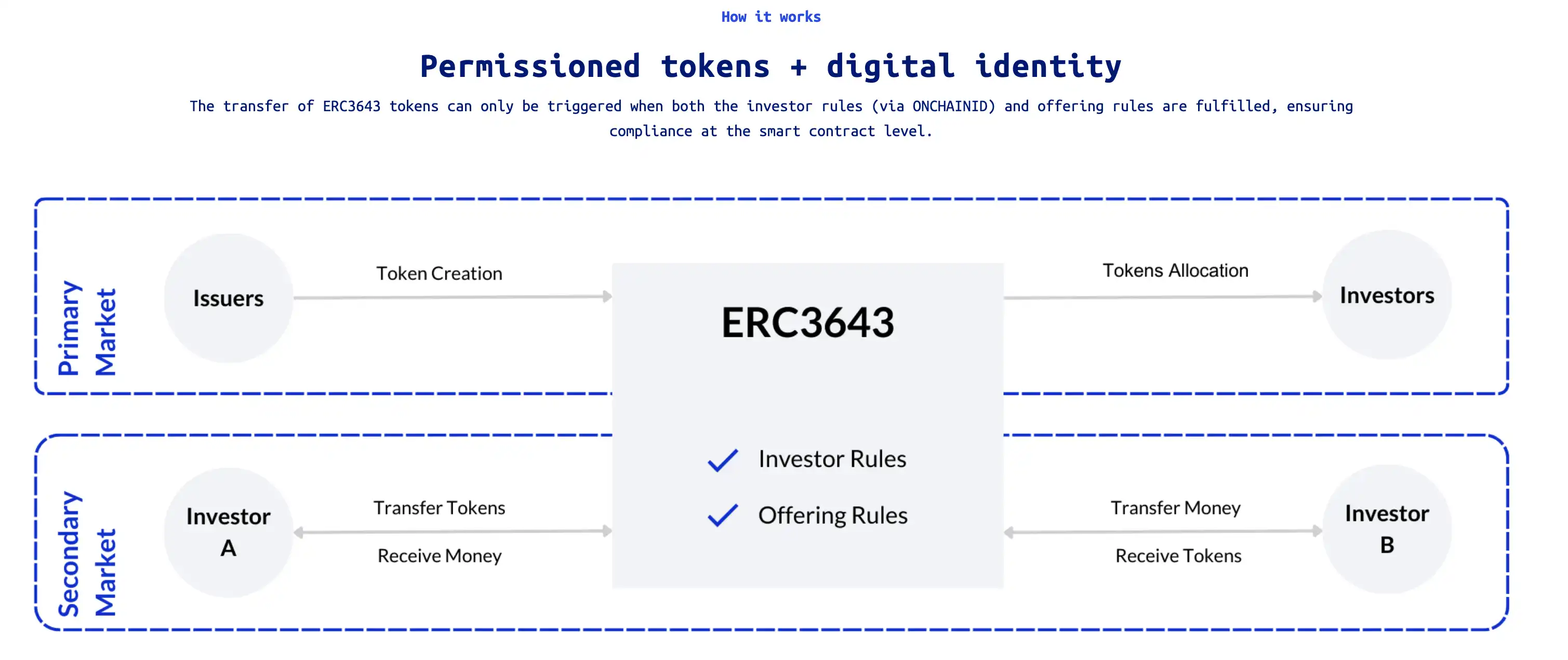

Paul emphasized that when designing the innovative exemption framework, the SEC will give priority to token systems with "built-in compliance capabilities." The ERC-3643 smart contract integrates mechanisms such as permission control, identity verification, and transaction restrictions, which can directly meet the current securities regulations on KYC, AML, and qualified investors.

The most significant feature of ERC-3643 lies in its "Compliance as Code" design. It incorporates a decentralized identity framework called ONCHAINID. All token holders must undergo identity verification and meet pre-defined rules before they can hold or transfer tokens. Regardless of the public chain on which the token is deployed, only users who meet KYC or accredited investor standards can truly own these assets. Compliance determination is performed at the smart contract level, eliminating the need for centralized audits, manual recordkeeping, or off-chain protocols.

The biggest difference between this and ERC-20 lies in the introduction of the dimension of "permissions." ERC-20 was born in a completely open, permissionless, on-chain native context. Any wallet address can freely receive and transfer funds, making it a completely "fungible tool." ERC-3643, on the other hand, targets high-value, heavily regulated asset classes like securities, funds, and bonds. It emphasizes "who can hold" and "compliance," making it a "permissioned token standard." In other words, ERC-20 is the free currency of the crypto world, while ERC-3643 is the compliant container for on-chain finance.

ERC-3643 has been adopted by numerous countries and financial institutions worldwide. In recent years, European digital securities platform Tokeny has been expanding the ERC-3643 standard to include private market securitization. In June of this year, Tokeny announced a partnership with digital securities platform Kerdo to build a blockchain-based private investment infrastructure using ERC-3643, covering asset classes such as real estate, private equity, hedge funds, and private debt.

From real estate to art collections, from private equity to supply chain instruments, ERC-3643 provides the underlying support for the fragmentation, digitization, and globalization of various assets. It is the only public blockchain token standard that combines programmable compliance, on-chain identity verification, cross-border legal compatibility, and integration with existing financial infrastructure.

As Paul Atkins stated in his speech, the future securities market must not only operate on-chain but also comply with regulations. In this new era, ERC-3643 may become a key bridge connecting the SEC and Ethereum, and between TradFi and DeFi.

Entrepreneurs return to the United States, and the primary market will take off again from the chain

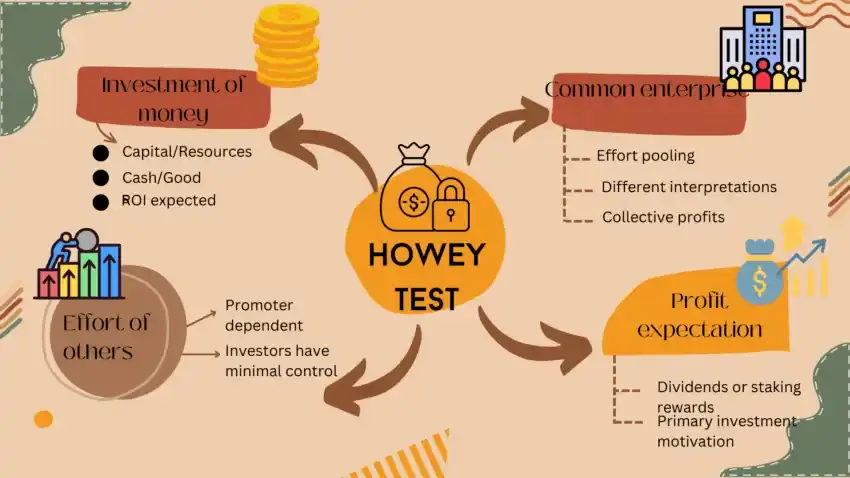

The Howey Test has long been the primary basis for the U.S. Securities and Exchange Commission (SEC) to determine whether an asset constitutes a security. Specifically, it includes four elements: whether there is an investment of money, whether the investment is made in a common enterprise, whether the income is generated by the efforts of others, and whether there is an expectation of profit. If a project meets these four criteria, it is considered a security and is subject to the securities law framework, including pre-issuance prospectuses, information disclosure, and regulatory filings.

It is precisely because of the vague testing standards and inconsistent enforcement that a large number of projects in the past few years would rather sacrifice the US market to avoid possible regulatory risks, and even deliberately "block" US users and not open airdrops and incentives.

In the recently released Project Crypto policy, SEC Chairman Paul Atkins explicitly proposed for the first time the development of a new classification standard for crypto assets, providing clear disclosure requirements, exemptions, and safe harbor mechanisms for common on-chain economic activities such as airdrops, ICOs, and staking. The SEC will no longer assume that "coin issuance equals securities." Instead, it will rationally classify assets based on their economic attributes into categories such as digital commodities (such as Bitcoin), digital collectibles (such as NFTs), stablecoins, or security tokens, and provide appropriate legal pathways.

This represents a key turning point: project parties will no longer need to "pretend not to issue coins", nor will they need to conceal incentive mechanisms through roundabout structures such as foundations and DAOs, nor will they need to register projects in the Cayman Islands. Instead, teams that truly focus on code and use technology as their core driving force will receive positive institutional recognition.

With emerging sectors like AI, DePin, and SocialFi rapidly emerging and demand for early-stage financing surging, this regulatory framework, based on substantive classification and encouraging innovation, is expected to spark a wave of projects returning to the US. The US is no longer a market that crypto entrepreneurs avoid, but may once again become their top choice for coin offerings and fundraising.

Summarize

"Project Crypto" isn't a single bill, but a comprehensive set of systemic reforms. It envisions a future where decentralized software, the token economy, and capital market compliance converge. Paul Atkins' stance is clear: "Regulation should no longer stifle innovation; it should make way for it."

For the market, this is also a clear signal of a policy shift. From DeFi to RWA, from Super Apps to coin offerings, who will take off in this round of policy dividends depends on who can first respond to this US-led "on-chain capital market revolution."