Author: Ignas

Compiled by Luffy, Foresight News

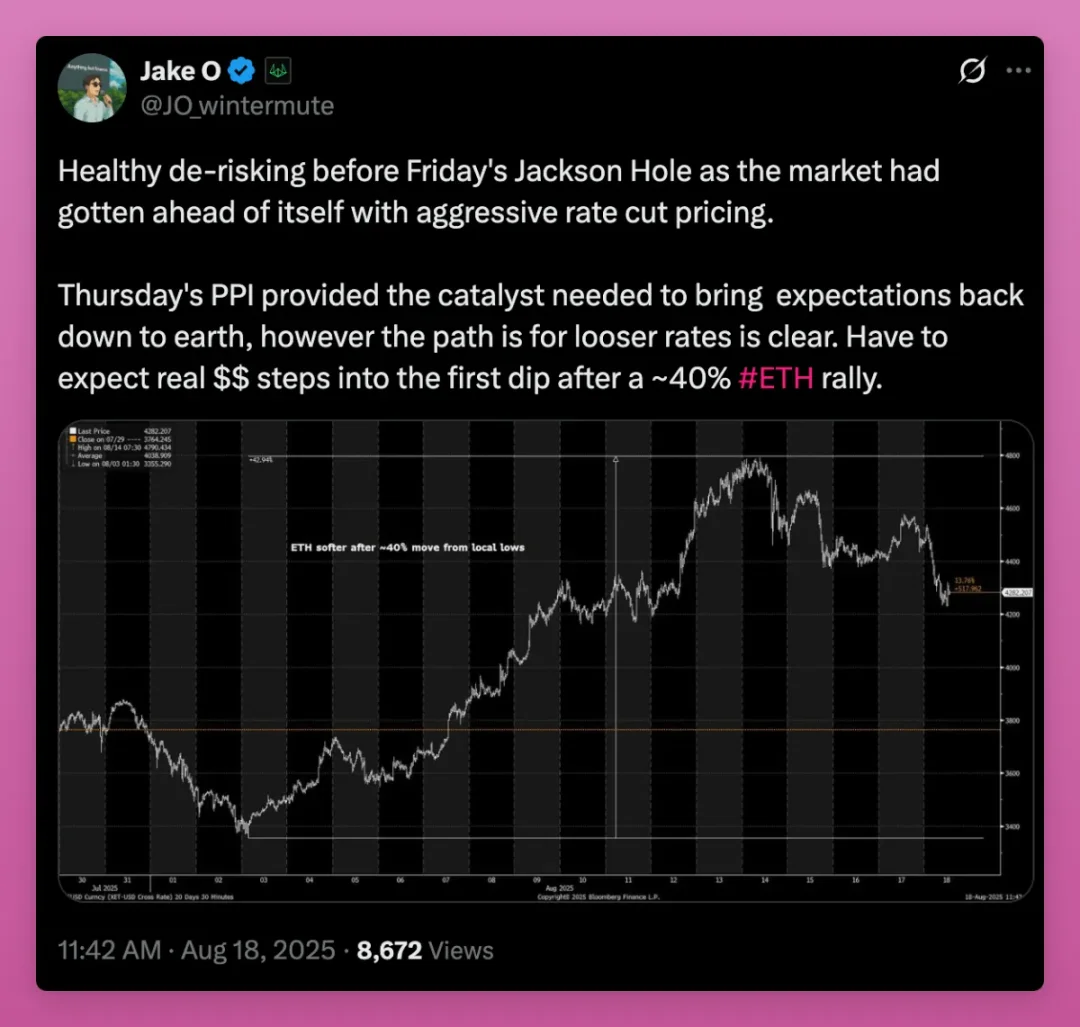

As I write this, the biggest short-term uncertainty for cryptocurrencies is the direction of interest rates. This will hinge on two key factors: first, Powell's comments at the Jackson Hole symposium (Thursday, August 22nd), and second, how the Federal Reserve sets interest rates at the Federal Open Market Committee (FOMC) meeting on September 16-17th.

- If a dovish signal is released → 2-year Treasury yields and the US dollar index fall → Bitcoin/Ethereum rise

- If there is a hawkish rate cut or high interest rates are maintained for a longer period → risk assets are sold off, and altcoins plummet first

This is the conclusion of the ChatGPT 5 thinking model and Deepseek's Deepthink model. Many people on the X platform also hold the same view, which also explains the recent decline in altcoins.

To be honest, cryptocurrencies’ dependence on macro factors is quite frustrating, but the fact that the last cycle peaked due to global interest rate hikes shows that we cannot ignore these factors.

However, as Wintermute trader Jack said, my AI model also paints a bullish picture: interest rate cuts will eventually come. The uncertainty lies in "when, how many times, and how big the cuts will be."

In this case, the situation now is exactly the opposite of the end of the previous cycle: interest rate cuts are coming, so is the peak of the bull market still far away?

I hope so, but everyone I talk to plans to sell. So who is buying to offset the selling pressure?

The retail speculators we relied on in the last cycle have not yet entered the market (as can be seen from the crypto app data in the iOS App Store). The largest buyers at present are:

- Spot ETFs

- Crypto Asset Treasury (DAT)

My concern is: can the buying power of institutions, crypto treasuries, and other large investors offset rounds of retail selling, or will their buying power run out?

Ideally, this is a process that unfolds over several years, with steadily rising prices gradually weeding out less committed investors.

The most interesting outcome could be that cryptocurrencies continue to rise even as most crypto “natives” sell off, triggering further gains.

Regardless, crypto treasury is both a significant risk point and a key bullish factor, and I want to briefly touch on this point.

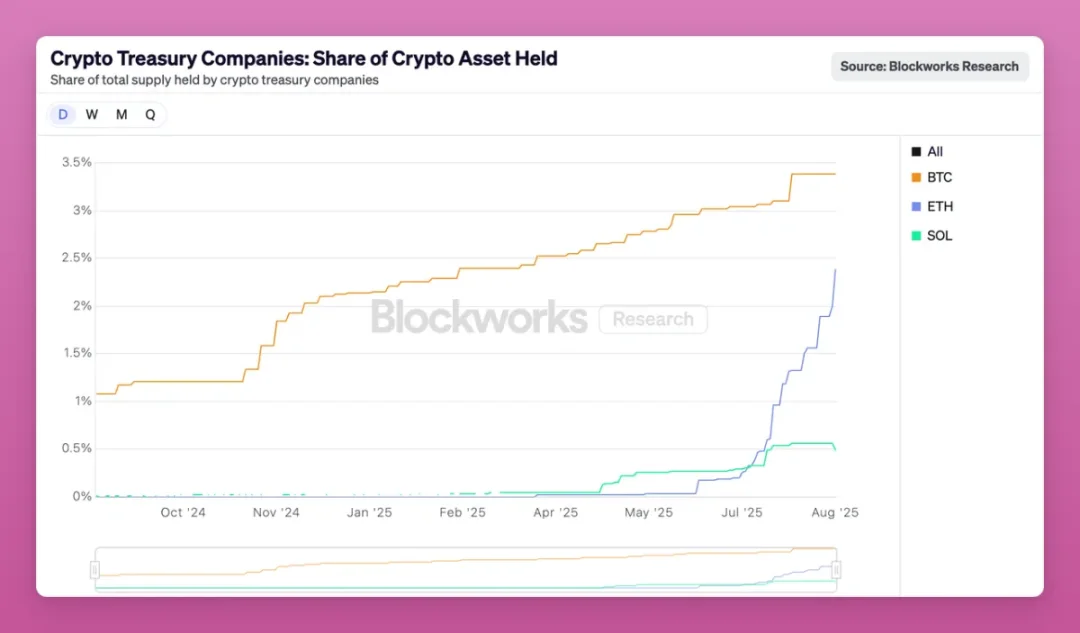

Now it’s all about crypto treasury

Just look at the speed at which crypto asset treasuries are acquiring Ethereum.

It took the Ethereum Crypto Asset Treasury less than three months to acquire 2.4% of the total supply of Ethereum.

Looking at it from another perspective: The holdings of the current largest Ethereum crypto asset treasury (Bitmine) are comparable to those of the crypto exchange Kraken, exceeding exchanges such as OKX, Bitfinex, Gemini, Bybit, Crypto.com, and even exceeding the holdings in the Base chain cross-chain bridge.

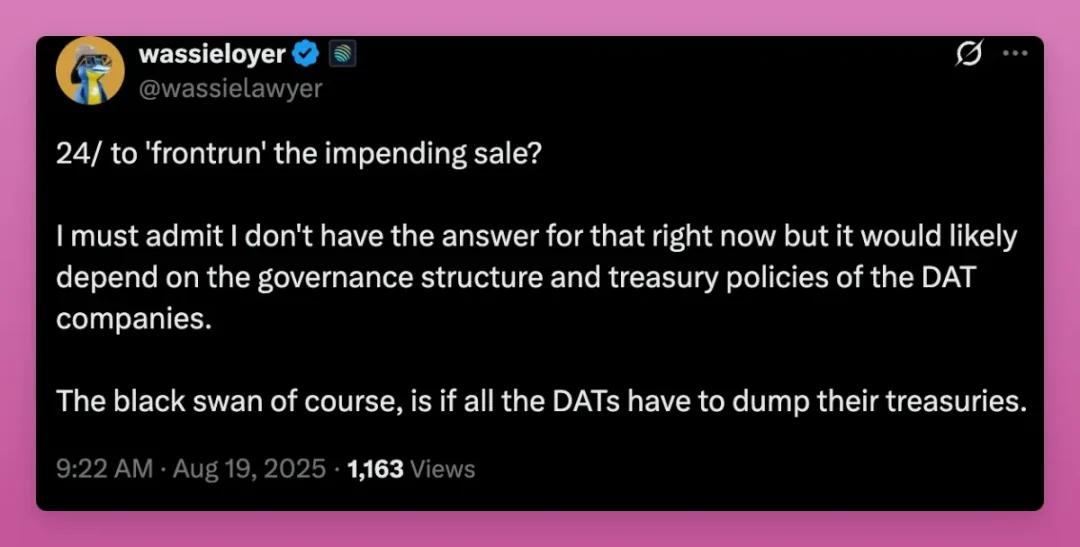

At this rate, within a few months, the proportion of Ethereum held by crypto asset treasuries will exceed that of Bitcoin. This is bullish for Ethereum in the short term, but risks arise once crypto asset treasuries need to liquidate their Ethereum holdings.

But even Wassie acknowledges that it remains unclear what happens to crypto treasuries when adjusted net asset value (mNAV) turns negative.

There’s been a lot of speculation on the X platform, but my advice is to continue tracking the crypto treasury data, paying particular attention to whether the adjusted net asset value is consistently below 1.

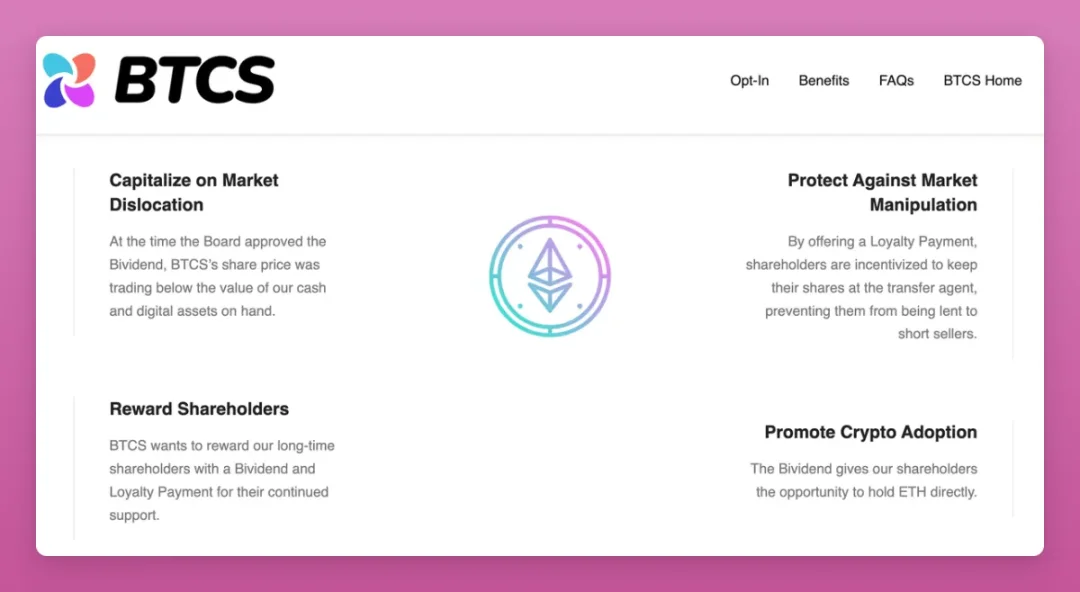

As I write this, SBET and BMNR are trading slightly above their adjusted net asset value of 1, while BTCS is trading below 1.

So what is BTCS doing?

To attract more stock buyers, BTCS announced its first "double dividend": a one-time ETH dividend of $0.05 per share and a cash dividend of $0.35.

On top of that, they are offering… read this carefully… “We will offer a one-time loyalty bonus of $0.35 USD in Ethereum per share to shareholders who transfer their shares to our transfer agent for registration and hold them until January 26, 2026.”

To crypto natives, BTCS's operation resembles a traditional financial "staking mechanism," designed to prevent shareholders from selling their shares. Their motivation for issuing a "double dividend" stems from the adjusted net asset value falling below 1 and as a safeguard against market manipulation—preventing shares from being lent to short sellers.

Also, where do these dividends come from? Actually, they are paid with the Ethereum they acquired.

Doesn't look good, does it?

At least they haven't publicly sold off their Ethereum yet. My guess is that the first treasuries to succumb and sell crypto assets will be smaller companies that can't attract buyers for their stocks. So follow these dashboards to identify crypto treasuries and study how they're handling their crypto holdings.

Crypto Twitter may ignore small crypto treasuries, but their movements can give us an idea of what larger, systemically important crypto treasuries will do.

Here are a few dashboards worth noting:

- Blockworks

- The Block

- Delphi

- Crypto Treasuries 1

- Crypto Treasuries 2

- Crypto Stock Tracker

It’s important to note that different dashboards report slightly different data, which makes analysis more difficult. We’ll need to keep a close eye on the movements of other crypto asset treasuries.

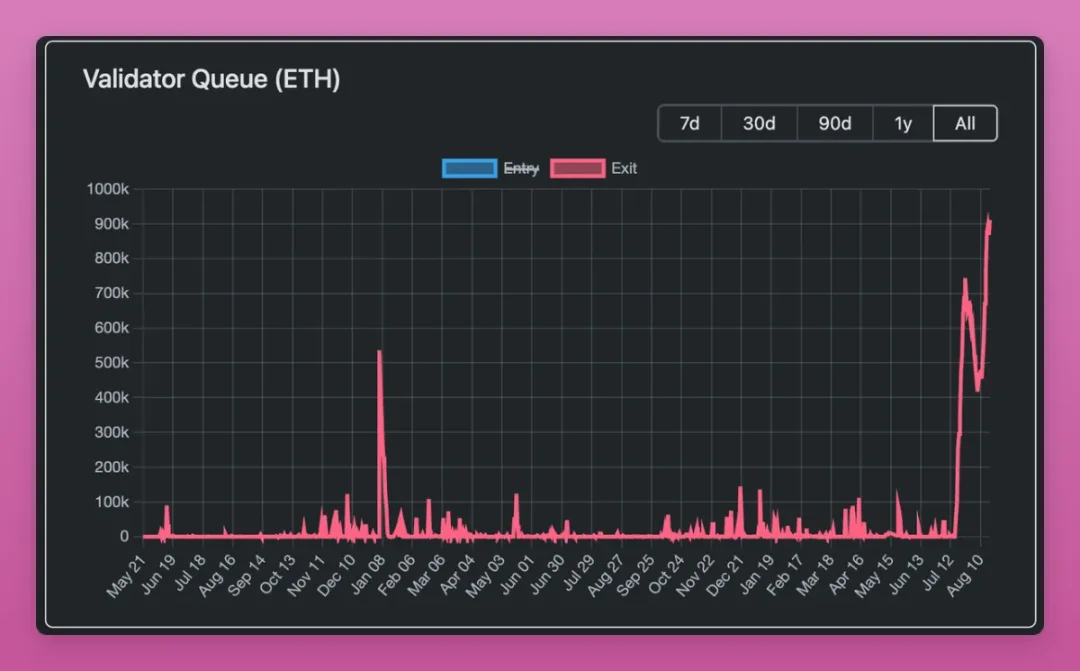

However, given the current low premium to adjusted net asset value and the record number of Ethereum unstacking queues, it would not be surprising if Ethereum's gains could slow down for a few days or even weeks.

Before moving on to other topics, I want to add that I am becoming increasingly optimistic about the altcoin crypto asset treasury.

The bullish logic behind altcoin crypto asset treasuries

This cycle has seen record-breaking issuance of new tokens. While most of these are worthless meme coins, the cost of issuing them has effectively dropped to zero.

Compared to previous cycles: Proof-of-Work forks require mining machines (such as Litecoin and Dogecoin) or building staking infrastructure (such as EOS, SOL, and ETH). Even in the previous cycle, issuing tokens required certain technical knowledge.

Before this cycle, the number of tokens worth paying attention to was "controllable", including several lending protocol tokens, decentralized exchange tokens, several public chain tokens, infrastructure tokens, etc.

Now that the cost of token issuance has dropped to zero, more projects are launching tokens, especially with the rise of Pump.fun, and it is becoming increasingly difficult for altcoins to attract enough attention and capital inflows.

For example: I've listed 11 numbers below, but what if there are thousands? There's no way to find the Schelling point (the point of default consensus among people without communication).

Previously, the only difference between Bitcoin and “other currencies” was Bitcoin. Coupled with MicroStrategy’s continued buying, only Bitcoin could rise.

But the altcoin crypto asset treasury has changed this situation.

First, very few altcoin projects are able to orchestrate the acquisition of crypto treasuries. This requires specialized knowledge and skills that most projects lack.

Secondly, there are only a limited number of altcoins that are “worthy” of having a crypto asset treasury, such as Aave, Ethena, Chainlink, Hype, or DeFi token indices.

Third, and perhaps most importantly, crypto treasuries give ICOs their “IPO moment,” attracting institutional capital that would otherwise be out of reach. As I wrote on Platform X:

I used to think altcoin treasuries were a crazy Ponzi scheme. But on second thought, crypto treasuries allow altcoins to "go public"—moving from ICOs to IPOs. BNB's crypto treasury is like Binance's IPO, which might not have been a proper IPO otherwise. $AAVE's crypto treasury, for example, allows traditional financial capital to invest in the future of lending. More crypto treasuries like this are in order.

Finally, unlike Bitcoin and Ethereum, altcoins do not have ETFs to attract institutional investors.

Therefore, altcoin crypto asset treasuries are an area I would focus on. They offer differentiation, such as over-the-counter sales that can attract venture capital, or token acquisitions at discounted prices.

Ethena is an early example, but I’d also like to see what happens when an altcoin with a high percentage of circulating supply has a crypto treasury.

Is it time to sell?

As I said before, many people around me are planning to sell, but they don't want to sell at the current price.

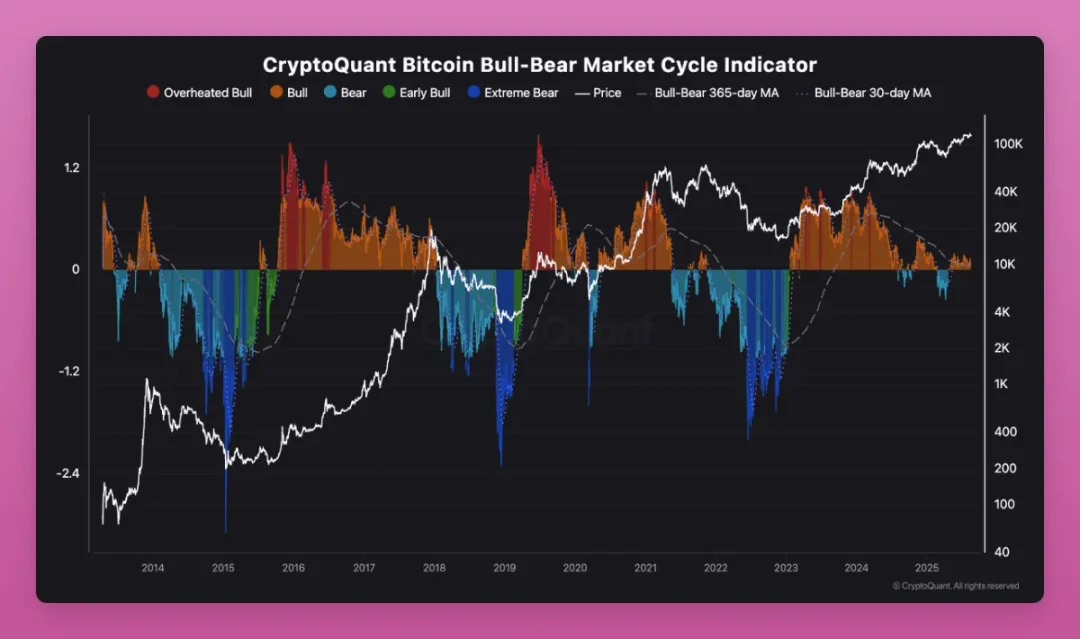

Why? Because all indicators still look surprisingly healthy. CryptoQuant's "All-Around Momentum Indicator" tracks bull and bear cycles using the P&L index.

The core conclusions (not much changed from a few months ago):

- Bitcoin is in the middle of a bull run.

- Holders are taking profits, but there has not yet been extreme enthusiasm.

- Prices can still rise before becoming overvalued.

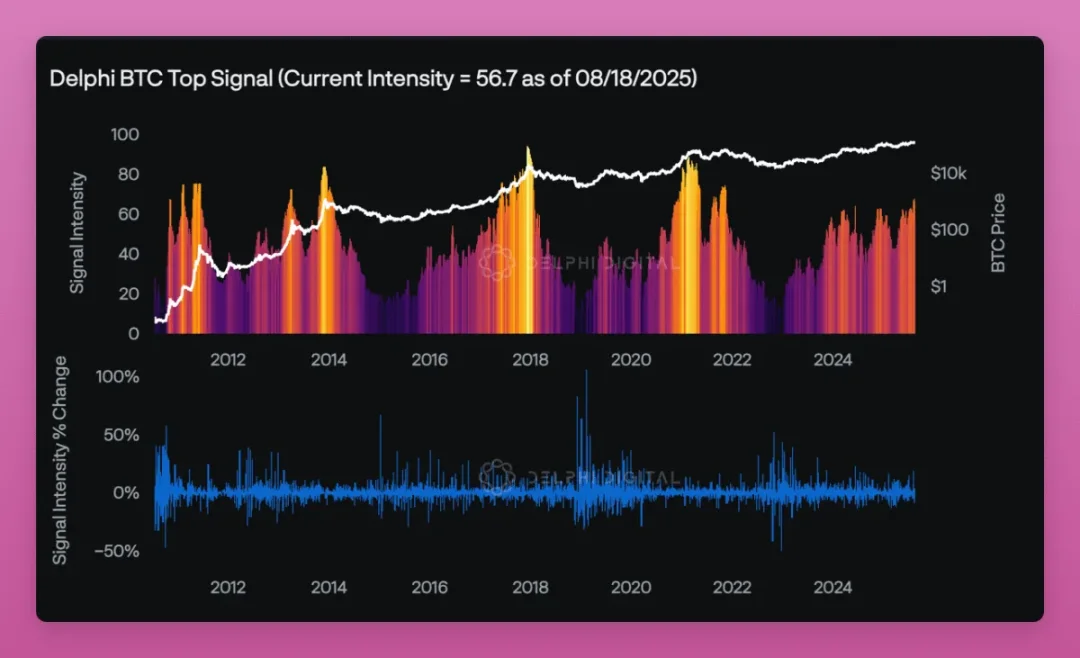

Still, Delphi’s Bitcoin Top Signals dashboard shows the market approaching overheating but still within control: its strength score is 56.7, while tops typically hover around 80.

The Fear and Greed Index has returned to neutral.

Furthermore, none of the 30 indicators tracked by Glassnode suggest a market top.

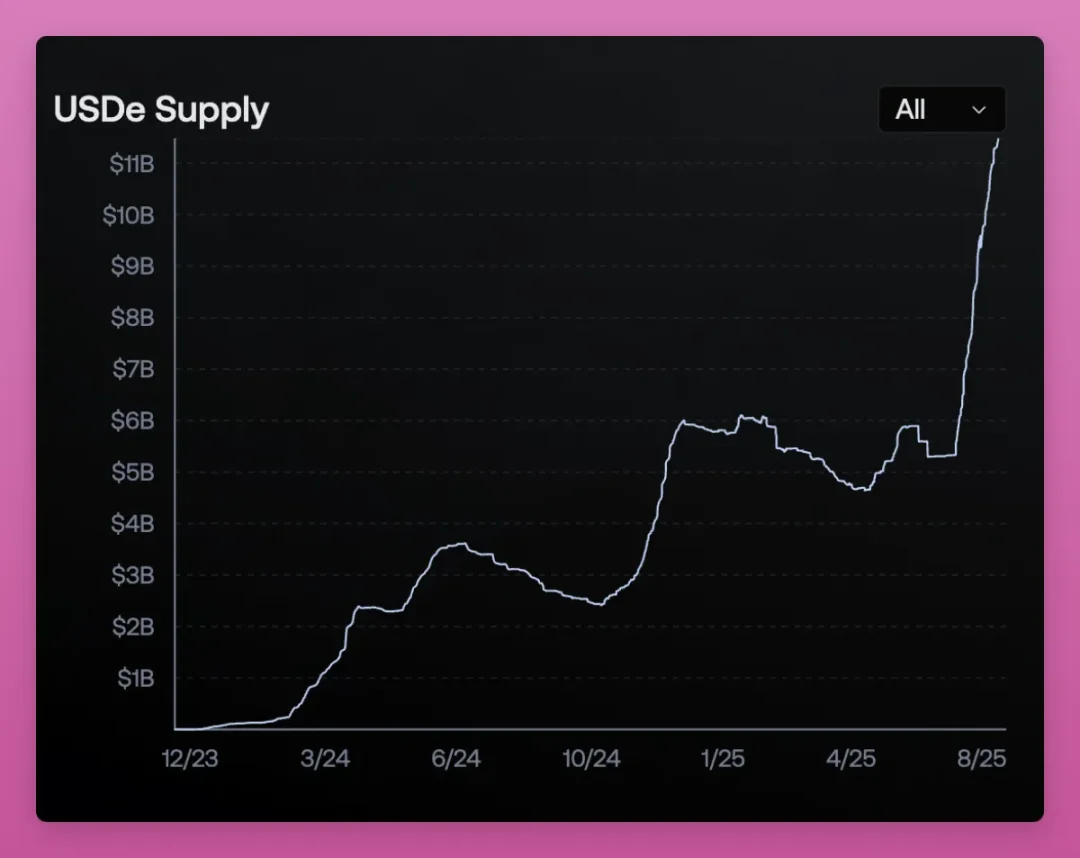

I used to identify market tops by funding rate peaks, but now I wonder if this metric is being distorted by Ethena.

In the past, high funding rates meant too many speculators were long, usually followed by a sharp drop. However, Ethena’s USDe broke this signal.

USDe mints stablecoins by going long on spot contracts and shorting perpetual swaps, earning funding rates as income. When funding rates rise, more USDe is minted, increasing short positions and further driving down funding rates, creating a cycle.

So now the high funding rate no longer means the market is overheated, it may just be that Ethena is issuing more USDe.

So, how about tracking the supply of USDe? Looking at it this way, the market is indeed hot, with USDe supply doubling in just one month.

Overall, I think the market is in good shape. However, since many retail speculators from the third and fourth cycles are holding positions with "life-changing" unrealized gains, every significant rally is met with a sell-off.

Hopefully, crypto treasuries and Ethereum can absorb this selling pressure.

Alternatively, a bear market could unexpectedly arrive again due to macro volatility, which could expose hidden leverage in the crypto space that we have yet to discover.

In the first article in the “State of the Market” series, I mentioned several areas where leverage might exist:

Ethena: USDe’s collateral has shifted from mostly Ethereum to Bitcoin and now to liquid stablecoins.

Restaking: While the narrative has quieted, Liquidity Restaking Protocols (LRTs) are integrating into mainstream DeFi infrastructure.

Circular arbitrage: Speculators leverage mining through circular operations in pursuit of higher returns.

Ethena used to be my biggest concern, but now crypto treasury is the primary focus. What if there's hidden leverage we're completely unaware of? That's something that keeps me up at night.

What to do after selling?

After transferring my tax base to Portugal, my investment strategy towards cryptocurrencies changed.

In Portugal, capital gains tax is 0% if the asset is held for more than 365 days; in addition, transactions between cryptocurrencies are not taxed.

This means I can convert it into stablecoins, hold it for a year, and get tax-free returns.

The question is: where should you store your stablecoins to maximize your returns while sleeping soundly?

Surprisingly, there aren’t many reliable protocols. Chasing high returns requires switching back and forth between different protocols, and one must be wary of vault migrations (such as during contract upgrades), and of course, the risk of hackers.

The vaults of Aave, Sky (Maker), Fluid, Tokemak, and Etherfi are the most withdrawn, but there are many other options such as Harvest Finance, Resolv, Morpho, Maple, etc.

The question is: Which protocol can you safely store your stablecoins for a year? Personally, I probably only trust two.

The first one is Aave. But the growth of USDe and the circular arbitrage of LST ETH/ETH makes me a little worried about large-scale liquidations (although Aave's new "umbrella" mechanism helps).

The second is Sky. However, S&P Global Ratings gave it its first stablecoin system credit rating, and the result is worrying—a rating of B-, which is "risky but not on the verge of collapse."

Weaknesses include:

- Depositor concentration

- Governance is still deeply tied to Rune (MakerDAO founder)

- Weak capital buffers

- Unclear regulation

This means that Sky's stablecoins (USDS, DAI), while considered trustworthy, are vulnerable. They're fine in normal times, but could be severely impacted by stress events like large-scale redemptions or loan defaults.

As PaperImperium put it: “This is a disastrous rating for major stablecoins.”

However, the risk tolerance of traditional finance is much lower than that of crypto natives, but it is certainly not possible to put all stablecoins in one protocol.

This also shows that cryptocurrencies are still in their early stages and there are no real "passive investments" except for Bitcoin and Ethereum.