Author: Zuoye Waiboshan

Hyperliquid's fluidity can always surprise or shock people.

On August 27, just as Hyperliquid announced that its BTC spot trading volume was second only to Binance and that its trading volume last month had surpassed Robinhood, a super whale address related to Sun Ge placed orders to "attack" the $XPL pre-market contract market, causing users to lose tens of millions of dollars.

Unlike mainstream trading markets such as BTC/ETH, the Hyperliquid pre-market contract market has a low trading volume, and whales can exploit trading rules without permission, ultimately causing human tragedy.

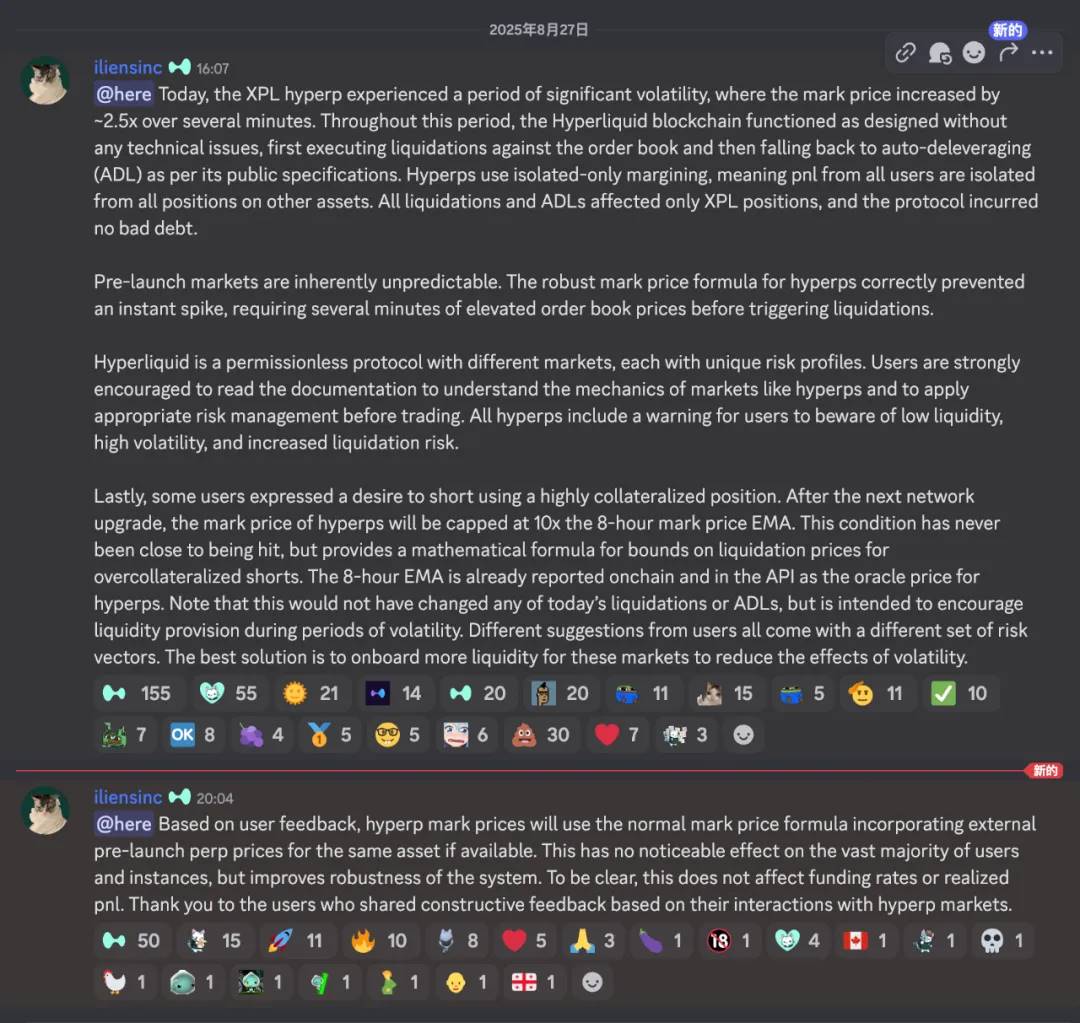

If it were a CEX like Binance, the whale would have been manually banned long ago, and even the possibility of placing a sniping order would be very small. Afterwards, the Hyperliquid team responded on Discord that they deeply understood the situation, had learned lessons, were determined to make improvements, and would not provide compensation for the time being.

Image Caption: HL team responds

Image credit: @hyperliquidx

Let’s recall the security incidents that occurred at HL and the results of their handling:

1. In November 2024, BitMEX founder Arthur Hayes and others accused Hyperliquid of a centralized architecture.

2. In early 2025, the 50x whale breached the HLP vault, and the HL team subsequently adjusted the leverage ratios of multiple currencies;

3. On March 26, 2025, facing the malicious sniping by $JELLYJELLY, the HL team directly unplugged the network cable to protect themselves.

4. On August 27, 2025, a whale attacked the pre-market contract market $XPL. The official said that the risk was borne by the investor.

It can be found that the HL team takes completely different measures in response to different security incidents. If it does not involve HL's own treasury or interests, it is decentralized governance. If it really endangers the protocol itself, the super-management authority will be directly used.

I have no intention of making a moral judgment on this matter. I can only say that any place where trading liquidity is concentrated will inevitably face the "accident" of protecting the liquidity of retail investors or giant whales. From Binance's opaque listing standards to Robinhood's retail investors fighting Wall Street, there is no exception.

Spacetime is a circle, and fluidity is the source of gravity

In 2022, the Perp DEX craze emerged. After the collapse of FTX, a gap appeared in the perpetual contract market. Binance followed the idea of listing coins and encountered PumpFun's reshaping of its pricing strategy.

Hyperliquid is not special. It imitates the $BNB = Binance main site + BNB Chain strategy, migrating all liquidity to the no KYC chain. Binance's regulatory arbitrage is growing rapidly, and HL's no-entry arbitrage attracts retail investors.

Back in 2022, everything in the cryptocurrency world originated from the collapse of FTX. Backpack took away Solana's legitimacy, Polymarket took away the prediction of political events, and Perp DEX was still enduring the dominance of GMX and dYdX, as well as the intrusion of Bybit and Bitget.

There was a brief blank period in the market, and Binance was caught in the threat of investigation. At that time, Biden was in office. The Democratic president did not like cryptocurrencies. SBF, which donated tens of millions of dollars to Biden, had to go to jail. Gary was in the Sand Dollar circle as the chairman of the SEC, and Jump Trading had to stop.

When all horses are silent, there is opportunity in crisis.

Binance was censored, FTX collapsed, BitMEX was old, OK/Bybit/Bitget were all fighting off-chain. At that time, CEX did not deny the trend of on-chain migration, but the chosen path was wallets.

Hyperliquid chose to embrace CLOBs (Central Limit Order Books), using the off-chain matching + on-chain settlement method, and borrowed the LP Token mechanism from GMX, and the Incentive Game was officially launched.

Image Caption: Perp DEX Panorama

Image credit: @OAK_Res

However, this mechanism was not even new in 2023-2024. At the critical moment, Pump Fun broke through Binance's pricing system, and the Meme craze allowed HL Liquidity to truly gain the first batch of loyal users.

Before Pump Fun, NFT or Meme existed, and even BNB Chain was the main battlefield in 2021, so I don’t understand that Meme is purely marketing, but Pump Fun chose the internal and external market mechanism and Solana ecosystem.

• The internal and external market mechanism gives small amounts of funds the opportunity to test any possibility on a large scale;

• The Solana ecosystem maximizes the rapid growth and decline of Meme transactions.

All of this has disrupted the rhythm of VC financing - project establishment - Binance exit - > empowering BNB. The collapse of the overvalued system is a precursor to Binance's liquidity crisis. It can be said that BNB is now Binance's debt, and Binance Alpha is full of helplessness in passive defense.

The meme craze was the first time HL verified itself. Liquidity is available everywhere. After the small-batch and small-currency trials, big funds and mainstream currencies will come. In terms of publicity and promotion, it is all reverse marketing. First, it is said that there are big investors, and then retail investors dare to enter the market. But in fact, without the losses of retail investors, there will never be profits for MM (market makers), whales and protocols.

Hyperliquid cannot operate without external capital injection and relies entirely on its own funds to maintain super liquidity, but the lack of VC does not conflict with this. In November 2024, Paradigm has entered the $HYPE system. According to @mlmabc's estimate, the purchase volume may be 16 million.

Image Caption: Paradigm Buys $HYPE

Image source: @matthuang

VCs can directly buy in, which is hard to be considered a traditional investment model. Similarly, MMs (market makers) may also participate in this way, but logically speaking, they are all airdropping and buying in the same way as ordinary retail investors.

From a narrative logic perspective, the project's token issuance and sell-off is a typical game theory crisis. There is mutual distrust among the project owner, multiple VCs, and exchanges. Although selling immediately after unlocking will result in a loss of future profits, the existing profits will be retained. Therefore, all stakeholders choose to sell immediately, and a world is created where only the exchanges and project owners are hurt.

Hyperliquid airdrops $HYPE while retaining control of the project, and trades spot $HYPE on its own exchange. This dual control stabilizes the initial momentum of the flywheel. Bybit will not list $HYPE spot until mid-2025. It is likely that it is a direct purchase to increase the trading pair, and it is unlikely that HL will promote the listing of the coin.

HL is not mysterious. When Pump Fun launched Hyperliquid, its wealth-creating effect was stronger than that of Binance. Binance simply won back another game today. Such events will continue for a long time. When $JELLYJELLY came, Binance and OK could put aside their past grudges and join forces to snipe Hyperliquid.

The business world is like a battlefield, the competition is long but there are few match points.

Retail investors trade meme coins, while big investors flock to HL

In an era when retail investors refuse to trade, what exactly are the big investors making money from?

Meme went bankrupt, and among Pump Fun, Berachain and Story Protocol, you can guess which protocol has the highest revenue. It turned out to be Pump Fun, where retail investors are leaving, and Berachain, which is designed natively for DeFi, has become a bygone era.

However, retail investors will no longer touch altcoins. The current rise is due to the spillover of liquidity from the U.S. stock market. Unfortunately, DAT has already started selling coins. The coin-stock-bond flywheel strategy (MSTR) looks good but is difficult to learn. Even ETH is far less resistant to growth than BTC.

In an era when retail investors refuse to trade, everyone is targeting large investors and institutions. Their thinking is interesting. They believe that as long as large investors become trading counterparts, they can earn agency fees and handling fees. This is no longer lazy thinking, but an insult to Hyperliquid.

Liquidity will always be the most common infrastructure in the crypto industry, and Hyperliquid has succeeded by establishing direct connections with retail investors.

If the 500,000 no KYC users are all big players and whales, then cryptocurrencies would have replaced the existing financial system long ago. Even Trump's $5 million gold card couldn't sell that many. Similar to USDT, the no-KYC policy has a huge appeal to funds. You can say that there are many practitioners in the black and gray industries, but this is by no means a financial miracle that can be created by a few people.

In this attack, Twitter (X) claimed that the victims were real users, and in the pre-market contract market with less trading volume, this proves Hyperliquid's appeal and user base. The only problem is that HL messed up this time and used liquidity to hit its own governance system.

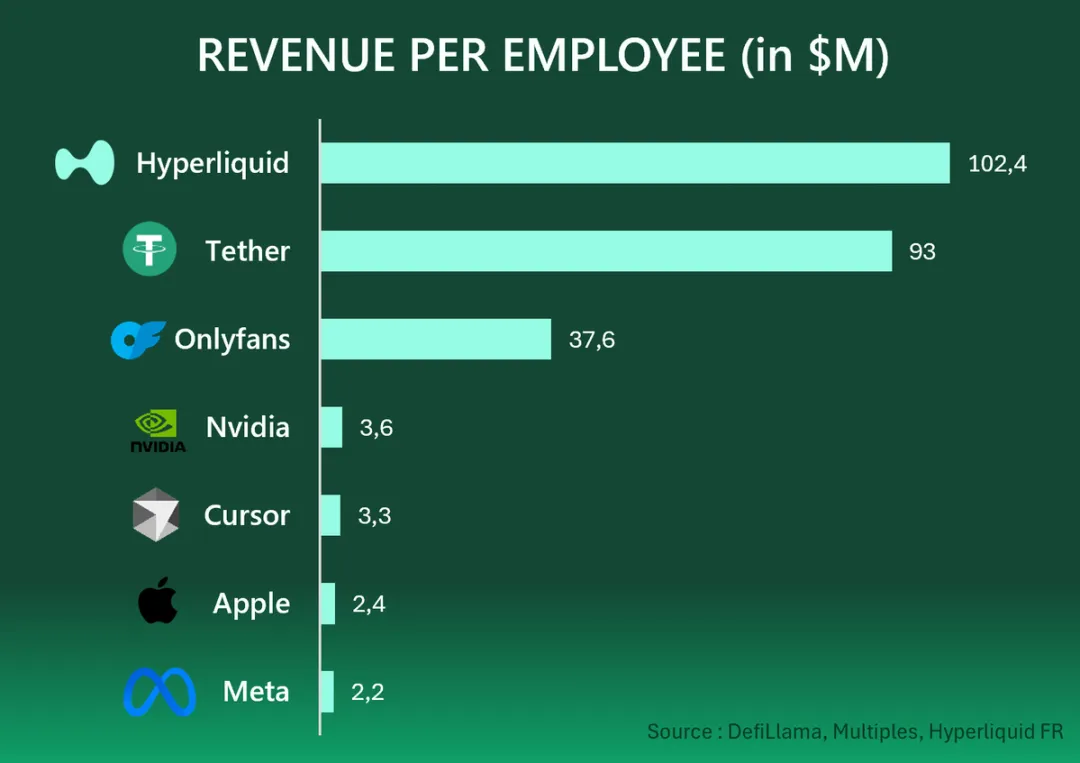

11 people created an annual revenue of $1.167 billion, with an average benefit of $106 million per person. Tether was followed by $93 million per person, and then Onlyfans' $37.6 million. The scale effect of the Internet, coupled with the most primitive desires of mankind, has created an extremely brilliant underground and on-chain world between the characteristic industries of Asia, Africa, Latin America and the first world.

Image caption: Web2&3 enterprise average profit

Image credit: @HyperliquidFR

If you think Hyperliquid is all about whales trading against each other, then does that mean Tether is all about big players swapping? Or that Onlyfans is all about big players going into the market?

In an era when retail investors refuse to trade altcoins and memes, the high leverage of BTC and ETH is one of the few "opportunities" and is fatally tempting to everyone. Of course, being short squeezed is also a fatal loss.

One cannot deviate from the path of success a second time.

Binance will only continue to optimize its listing logic until it falls into an endless loop of overfitting.

CEX will only increase rebates based on liquidity until it breaks through its own meager profit margins;

CLOB DEX will only learn to become Binance, and after issuing tokens, it will become a GMX copycat.

Maverick pigs are rare, and there are many people who provide asset management services for large investors. If you still assume that CEX has the largest liquidity today, it can only be said that you are not suitable for participating in the next crypto market.

Retail investors have entered the permissionless free market, large investors have gained liquidity exit opportunities, Paradigm has gained from the increase and holding of $HYPE, and retail investors have the opportunity to make a small profit with a big investment, provided that they do not touch small currency assets.

Everyone sets a price for their own destiny, and then All in Crypto is the eternal theme.

Conclusion

Human intervention is a traditional feature of Hyperliquid, and the entire Perp DEX track is heavily influenced by human rule.

It’s not that the HL airdrop and profit distribution are in place, nor that the technical architecture built by Jeff is better, but rather that after the collapse of FTX and the market gap of Binance being regulated, Hyperliquid actually has limited competitors, and timing is always the best entry point to break the existing structure.

FTX collapsed—-> Binance was restricted by regulation, and Binance management was obsessed with listing ideas. PumpFun pierced Binance's listing mechanism and pricing logic, leaving Perp DEX with a huge market opportunity. Bybit benefited from this existing mindset, while Hyperliquid built the $HYPE flywheel.