Author: Thejaswini, Source: Token Dispatch

Exchange-traded funds (ETFs) were born in the midst of crisis.

On Black Monday in 1987, when the Dow Jones Industrial Average plummeted more than 20% in a single day, regulators and market participants realized they needed better tools. Mutual funds could only be traded at the end of the trading day, leaving investors powerless during market panics.

ETFs emerged as a solution. ETFs are baskets of securities that trade like individual stocks, providing immediate liquidity when market conditions deteriorate.

ETFs simplify index investing, providing broad market exposure with low fees and tax efficiency. They are designed to be transparent and require no active management—they simply track the index, not try to outperform it. The first successful ETF, the SPDR S&P 500 Index (SPY), launched in 1993 and became the world's largest fund by strictly following the S&P 500 Index.

At first, it seems like a good idea. You want to buy "stocks," but you don't want to research individual companies or pay a fund manager to do it for you.

In September 2025, Wall Street crossed a new threshold: packaging memecoins into regulated investment products and charging a 1.5% annual fee for it.

Are we witnessing a fundamental shift in the nature of ETFs?

ETFs have evolved from simple tools that streamline investing to complex instruments capable of integrating any imaginable strategy. While there are endless ways to combine, hedge, time, or structure your investments, there are only a limited number of companies you can actually invest in.

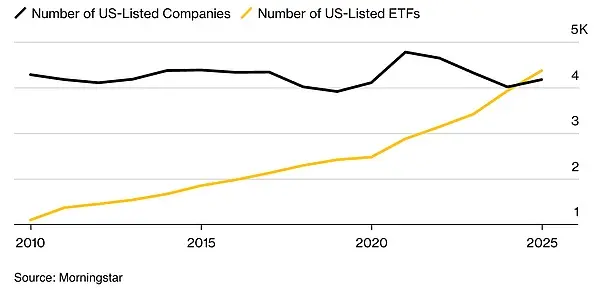

There are now more than 4,300 exchange-traded funds, compared to about 4,200 publicly traded companies. ETFs now account for about 25% of all investment vehicles, up from 9% a decade ago. For the first time in market history, there are more funds than actual stocks.

In my view, this creates a fundamental problem—an overabundance of choice that overwhelms investors, rather than empowers them. Today, we have funds covering every conceivable theme, trend, or political viewpoint. The line between serious long-term investing and entertainment has completely blurred. It's almost impossible to distinguish between products designed to build wealth and those designed to capitalize on social media trends.

Stop. This anxiety completely misses the point. A Dogecoin ETF doesn’t distort the mission of cryptocurrency.

For fifteen years, cryptocurrencies have been dismissed as worthless cybercurrencies. The traditional financial world called us degenerate speculators playing with worthless tokens. They said we would never create anything real, never gain institutional adoption, and never deserve serious regulatory attention.

Now they are trying to extract value from an asset we created as a joke.

The cryptocurrency industry has created a whole new value category that traditional finance cannot ignore, cannot eliminate, and ultimately cannot resist monetizing. Dogecoin's acquisition of an ETF before half of the Fortune 500 companies have developed comprehensive crypto strategies is a stark testament to the dominance of cryptocurrency culture.

Okay, now that we’ve celebrated the win, let’s look at what exactly we’re celebrating.

Why would anyone pay 1.5% for something that is available for free?

A memecoin ETF makes no economic sense to investors, but it makes perfect sense to Wall Street.

You can buy Dogecoin directly on Coinbase in under five minutes, with zero ongoing fees. The REX-Osprey Dogecoin ETF charges 1.5% annually for the same exposure—on a $10,000 investment, that's $150 annually. Bitcoin ETFs charge 0.25%. So why would anyone pay six times more for a memecoin than for digital gold?

The answer reveals the true target audience for these products. Bitcoin ETFs serve institutional investors who demand regulatory compliance and savvy wealth managers who understand cryptocurrencies. They compete on fees because their clients have alternatives and know how to use them.

Memecoin ETFs target retail investors who saw Dogecoin trending on TikTok but don't know how to buy it directly. They pay for simplicity and legitimacy, not market exposure. These investors don't shop around—they just want to click "buy" on the Robinhood app and get exposure to the meme they keep hearing about.

The issuers know this is ridiculous. They know customers can buy Dogecoin cheaper elsewhere. They're betting most people won't discover this or won't want to deal with crypto exchanges and wallets. The 1.5% fee is essentially a tax on financial ignorance, packaged as institutional legitimacy.

What makes an asset worthy of inclusion in an ETF?

Traditional ETF definition: A regulated investment fund that holds a diversified basket of securities and trades on an exchange like stocks, providing investors with broad market exposure while maintaining professional oversight, custody standards, and transparent reporting.

Classic models track indices like the S&P 500, holding hundreds of companies across multiple industries. Even single-sector ETFs, such as technology or healthcare funds, hold dozens of stocks within their focus areas. Diversification reduces risk while providing exposure to market trends.

Now let's look at what Dogecoin actually is: a cryptocurrency created in 2013 by copying Litecoin's code and adding a meme-like dog logo, born purely as a satire. It has no development team, no business plan, no revenue model, and no technological innovation. Its supply increases by 5 billion coins annually, making it inflationary by design, mocking Bitcoin's scarcity.

This token has no economic utility. You can't build applications on it, and you can't earn returns by staking it. Its only function is to exist as an internet meme, occasionally hyped up by a celebrity tweet.

What regulatory loopholes make this possible?

The path to marketization reveals how financial innovation actually works: regulatory arbitrage that circumvents the spirit of the law but technically adheres to the letter of the law.

The REX-Osprey Dogecoin ETF (DOJE) was launched under the Investment Company Act of 1940, rather than the Securities Act of 1933, which regulates commodity ETFs like Bitcoin. This choice is crucial. The 1940 Act provides for automatic approval after 75 days unless the U.S. Securities and Exchange Commission (SEC) raises objections, creating a regulatory shortcut. The problem? The 1940 Act was designed to support diversified mutual funds that spread risk across multiple assets, rather than single-asset speculation based on abandoned memes.

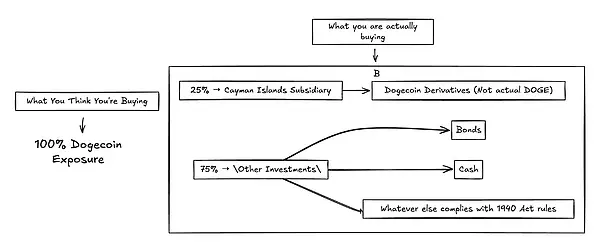

To meet diversification requirements, the DOJE cannot hold Dogecoin directly. Instead, it uses derivatives through its Cayman Islands subsidiary to gain exposure, with a maximum holding limit of 25% of its assets. This creates an absurd situation: a Dogecoin ETF can only have a maximum exposure to Dogecoin of 25%.

This fundamentally changes what investors are actually buying. When an ETF holds assets directly, it accurately tracks their prices. Using derivatives through offshore subsidiaries introduces tracking error, counterparty risk, and complexity, distorting performance. The fund's returns become disconnected from Dogecoin's actual market movements.

This regulatory circumvention creates transparency issues. Retail investors who bought into the Dogecoin ETF expected direct exposure to the memes they saw on social media. But what they actually received was a complex derivative product in which three-quarters of the investment had no correlation with Dogecoin price movements. Their returns were diluted by the remaining 75% of the fund's other assets.

Worse, this structure subverts the original protective intent of the Securities Act of 1940. Congress enacted diversification rules intended to reduce risk by spreading investments across a wide range of assets. Wall Street, however, found a way to exploit those same rules to package high-risk speculation into regulated vehicles with weaker oversight than intended. Rather than protecting investors from risk, the regulatory framework masked new risks with institutional legitimacy.

In contrast, most Bitcoin ETFs, such as ProShares BITO or Grayscale’s spot Bitcoin ETF attempts, typically use the Securities Act of 1933 or other frameworks designed for commodity funds to allow more direct or futures-based Bitcoin exposure without the strict 25% asset cap.

Bitcoin ETFs typically hold futures contracts directly or seek to directly custody Bitcoin (when approved), thereby more closely tracking Bitcoin's underlying price.

The Dogecoin ETF represents a perfect storm of regulatory arbitrage. The ETF invests in virtually nothing it's supposed to track, holding a useless asset while exploiting a 1940s law designed to prevent such speculation. It's financial engineering at its most cynical—exploiting regulatory loopholes to create a speculative product under the guise of investor protection.

Why such an obsession with yield?

Wall Street has abandoned fundamentals and is chasing returns regardless of asset quality.

State Street data shows that institutional portfolios have the highest allocation to stocks since 2008. Investors are pouring money into option-yield ETFs that promise monthly dividends, high-yield junk bonds and crypto-related income products that offer double-digit returns through derivatives.

Capital flows prioritize returns, asking questions later. When interest rates soar, investors aggressively shift to high-yield corporate bonds, abandoning the safer investment-grade sector. Thematic ETFs focused on artificial intelligence, cryptocurrencies, and meme assets are being launched at a record pace, catering to speculative demand rather than long-term value.

Risk appetite indicators continue to flash green. Despite macro market uncertainty, the Volatility Index (VIX) remains low. Following the turbulence in early 2025, defensive sectors briefly attracted inflows, but funds quickly retreated to higher-risk, higher-reward sectors such as industrials, technology, and energy.

Wall Street has essentially decided that in a world of unlimited liquidity and constant innovation, yield trumps all else. If something offers a premium return, investors will always find a reason to buy it, regardless of its fundamentals or sustainability.

Are we creating a bubble?

What happens when the number of investment products exceeds the actual investment target?

We've crossed the Rubicon, with ETFs outnumbering stocks. This is a fundamental change in market structure. We're essentially creating synthetic markets on top of the real market, and each additional layer increases fees, complexity, and potential points of failure.

Matt Levine noted:

As ETFs grow in popularity and technology makes them cheaper to implement, more trades that were once custom and manual will become standardized ETFs. The number of potential trades far exceeds the number of stocks… In the long run, the potential market for ETFs is limited by the (unlimited) number of trades, not the (decreasing) number of stocks.

The memecoin ETF phenomenon has accelerated this trend. Rex-Osprey has filed applications for a Trumpcoin ETF, a Bonk ETF, and traditional ETFs for XRP and Solana. Currently, 92 crypto ETF applications are awaiting approval by the SEC. Each successful launch creates demand for the next product, regardless of its underlying utility.

This is reminiscent of the CDO squared problem of 2008, when Wall Street created derivatives of derivatives until the financial products were completely disconnected from the underlying reality. We are now doing the same thing with mortgages, replacing them with attention and cultural phenomena.

Markets appear more liquid than they really are because multiple products trade around the same underlying asset. But in a crisis, all of these products tend to move together, and "liquidity" evaporates simultaneously.

What does a memecoin ETF mean?

The deeper story is about the evolution of finance into a comprehensive attention-capturing mechanism that can monetize any phenomenon that produces price fluctuations.

The launch of an ETF creates its own momentum through network effects. Driven by anticipated inflows from institutional investors, Dogecoin's price rose 15% in the month leading up to the DOJE's listing. Higher prices attract more attention, which in turn spawns more memes, increasing cultural relevance and providing a rationale for the creation of further financial products. Success breeds imitation.

Traditional finance monetizes productive assets like factories, technology, and cash flow. Modern finance monetizes anything that drives price: narratives, memes, social momentum. ETF packaging transforms cultural speculation into institutional products, extracting fees from the communities that originally created these phenomena.

The broader question is, is this innovation or extraction? Does the financialization of memes create new value, or does it simply extract value from organic cultural movements by increasing institutional costs?

Online culture already generates enormous economic value—advertising revenue, merchandise sales, platform engagement, and the creator economy.

I decided it was time to “soft-restart” my relationship with internet culture.

I've been pondering what will propel these companies to billion-dollar valuations by 2025. Somehow, I've ended up ordering matcha at Mitico Coffee Roasters in Bangalore, just to feel like I'm part of the action. Not because I particularly enjoy the taste of the ground green powder, but because matcha has become a ritual, a symbol of productivity and tranquil luxury that somehow makes you feel more connected to the global aesthetic of wellness.

Internet culture has now devolved into a series of participation fees disguised as lifestyle choices, and the monetization opportunities are everywhere, ranging from the straight-up ridiculous to the truly ingenious.

Consider the buzz of 2025. We witnessed Coldplay's "Kiss Cam" scandal, turning an awkward moment into a corporate resignation scandal that even forced Gwyneth Paltrow to inexplicably become a temporary spokesperson. The internet went wild over whether 100 men could defeat a gorilla (spoiler: experts say they can, but only barely). The Labubu craze turned $30 blind box collectibles into status symbols, with people even rushing to buy them in stores.

Then there's the language barrier I can't quite get past. Gen Z slang is constantly evolving. Last week, someone called my outfit "bussin'," and I honestly didn't know whether to be offended or delighted. Apparently, that's a good thing? My nephew tried to explain that "rizz" describes something glamorous, but then he started talking about "skibidi" this and "Ohio" that, and I realized I was completely lost. I tried to keep up, but honestly, trying to use the words correctly made me feel a little cheugy. This "trying too hard, millennial" vibe wasn't what I was going for.

Then Taylor Swift got engaged to Travis Kelsey, and within minutes, the entire marketing universe shifted. Brands from Walmart to Lego to Starbucks dropped everything to jump in on the conversation.

The key is that this cultural momentum is itself an economic engine. Katy Perry takes an 11-minute space flight, and the internet spends a week debating whether it's "extravagance"—engagement that translates into advertising revenue, brand exposure, and cultural capital, all monetizable in a dozen different ways. When everyone starts calling their friends "pookie" because of a couple on TikTok, suddenly an ecosystem of pookie playlists, pookie ribbons, and pookie merch is born.

Online culture creates immense economic value through the creator economy, merchandise sales, platform engagement, and movements that drive stock prices faster than quarterly earnings reports. If a single Elon tweet can add billions of dollars to Dogecoin’s market capitalization, and if Tesla’s valuation relies more on cultural momentum than fundamentals, then cultural phenomena are legitimate economic forces that deserve the same institutional accolades as other asset classes.

ETF wrappers don’t extract value from these communities—they formalize existing value and make it accessible to previously excluded populations. Retirees in Ohio can now access online culture through their 401(k) plans without having to learn a crypto wallet or navigate a Discord server.

Conversely, the same retiree could lose a significant portion of their retirement savings because of a forgotten internet joke. An annual fee of just 1.5% would eat up $1,500 per year from a $100,000 investment, regardless of whether Dogecoin rises or falls. Because regulatory requirements limit the ETF to 25% exposure to Dogecoin, this retiree may not have received the cultural exposure they thought they were buying. Financial accessibility without financial education can be dangerous. Making speculative assets easier to buy doesn't reduce risk—it simply makes it less obvious to those who may not understand what they're buying.

Financializing memes might actually strengthen these communities, rather than exploit them. When cultural movements are backed by institutional investment, they gain stability and resources.

If internet culture drives price, it becomes an asset class. If social momentum creates volatility, it becomes tradable. ETF wrappers are simply the delivery mechanism for transforming cultural energy into institutional products.