Author: Nancy, PANews

The listing fee has always been the focus of market controversy, especially the huge listing fee is often regarded as an important factor hindering market innovation. Therefore, more and more emerging projects choose DEX (decentralized exchange) as the first position, but at the same time, the risk of Rug has also increased significantly.

Recently, after successfully performing a textbook airdrop, the derivatives DEX Hyperliquid not only achieved impressive performance in many data, but also hit a new high in the spot auction price, further enhancing the platform's market advantage. With such strong data, PANews learned that many projects have already set their sights on listing on Hyperliquid.

The auction price of the listed coin increased significantly after the airdrop, and the spot trading liquidity was concentrated in HYPE

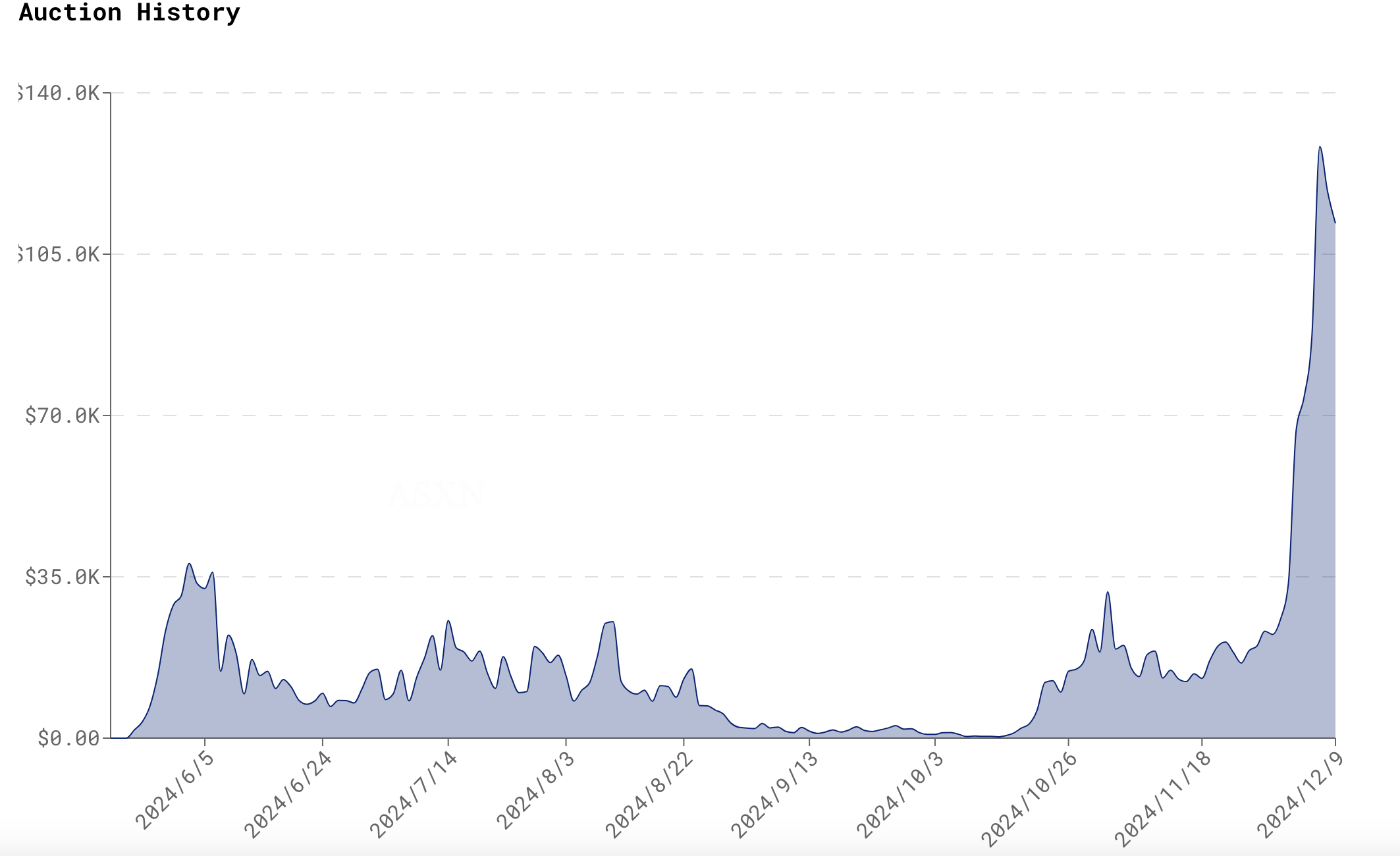

On December 6, a token ticket named "SOLV" set a new record for Hyperliquid's auction at a price of approximately US$128,000, which attracted the attention of many investors and was suspected to be related to Solv Protocol, which announced the upcoming TGE (token generation event).

According to official documents, if a project wants to launch Hyperliquid, it needs to obtain the HIP-1 native token deployment rights. HIP-1 is the native token standard established by the protocol for spot trading and creates an on-chain spot order book, similar to ERC20 on Ethereum. However, in order to obtain the right to issue new tokens, projects usually need to participate in Dutch auctions, which are usually held every 31 hours, which means that a maximum of 282 token codes are allowed to be deployed each year.

This auction fee can also be understood as the Gas fee for deployment, which is currently paid in USDC. During the 31-hour auction, the Gas fee for deployment gradually decreases from the initial price to a minimum of 10,000 USDC. If the previous auction was not completed, the initial price will be 10,000 USDC; otherwise, the initial price will be twice the final Gas price of the previous time. The introduction of this auction mechanism can not only avoid excessive speculation and irrational increases caused by excessively high prices, but also dynamically adjust the listing speed of new tokens according to demand. It is this mechanism that ensures that the number of tokens on the Hyperliquid market will not be too large, and gives priority to projects with excellent quality for listing.

Judging from past auctions, ASXN data shows that as of December 10, Hyperliquid has conducted more than 150 auctions since May this year. From the auction price point of view, Hyperliquid's airdrop has become an important turning point. The auction price before December was basically below $25,000, and even millions of dollars, and most of the token codes participating in the auction were MEME coins, such as PEPE, TRUMP, FUN, LADY and WAGMI, but this month's auction prices have risen sharply, except for SOLV, such as SHEEP's auction price of about $112,000, BUBZ about $118,000, GENES about $87,000, etc. This also reflects that the market demand and interest in Hyperliquid have increased significantly after the popularity of the airdrop.

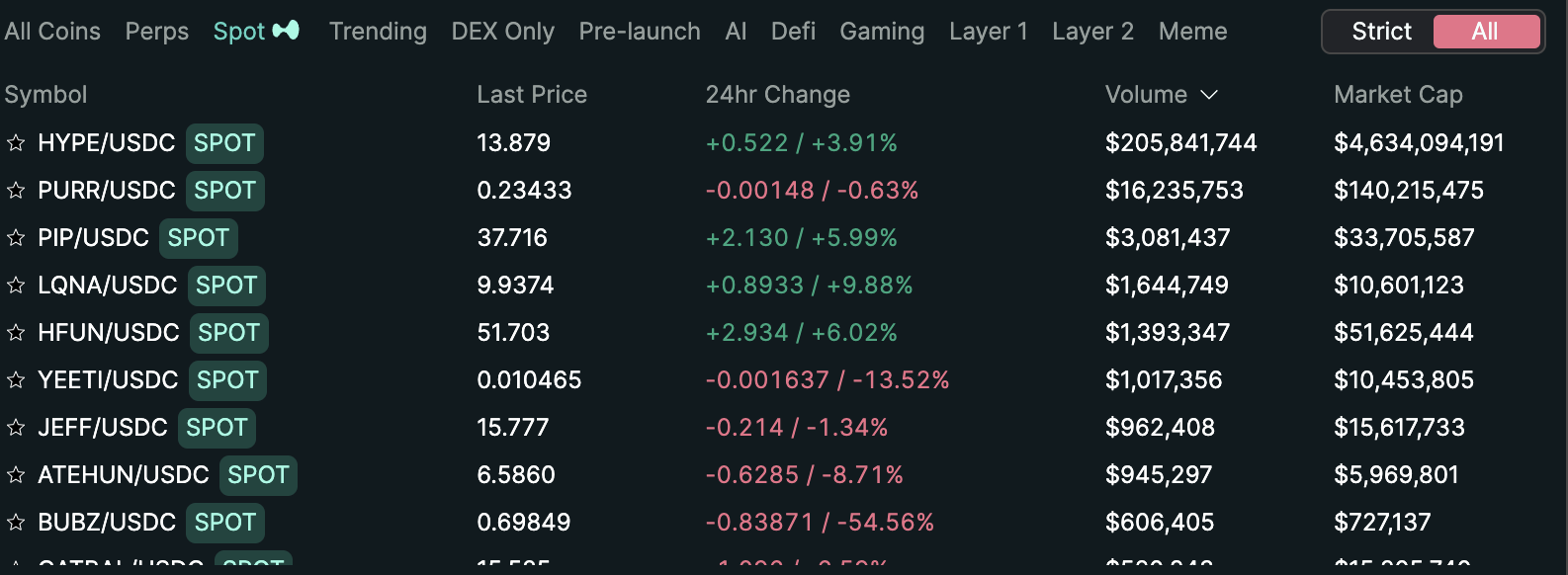

However, judging from the liquidity of hundreds of HIP-1 tokens launched, they are mainly concentrated in a few projects. Hyperliquid transaction data shows that as of December 10, there were hundreds of HIP-1 tokens launched on the platform, with a cumulative trading volume of approximately US$240 million in the past 24 hours, of which Hyperliquid token HYPE accounted for 85.9% of the total trading volume, and its ecological head MEME project PURR accounted for more than 6.7%, and the total liquidity of the remaining projects accounted for only 7.4%. This is related to the fact that Hyperliquid mainly focuses on derivatives trading, and the spot market has gradually taken shape after the rise of MEME.

“Compared to CEX, Hyperliquid currently has very few spot products that can actually be traded. If a large project wins a Hyperliquid spot seat through an auction, it is actually a strong combination. As an on-chain exchange, we are happy to see more high-quality large projects go online or launch through auctions; the USDC funds above can also focus more on the speculation of newly launched assets.” Wu said blockchain analyst @defioasis recently analyzed.

After the airdrop, many data showed impressive performance, and it may become a strong contender for listing?

With its outstanding market performance and innovative coin listing strategies, Hyperliquid may become one of the important competitors for coin listing applications.

On the one hand, the wealth-creating effect of Hyperliquid's airdrop and the successive increases in token prices have become the best marketing tools. As the popularity of the project has surged, Hyperliquid has performed strongly in many data performances.

From the perspective of token price performance, compared with the situation of most projects opening high and closing low after airdrop, the FDV (fully diluted valuation) of Hyperliquid's token HYPE has soared all the way. According to Coingecko data, HYPE's circulating market value once reached 4.96 billion US dollars, and has now fallen slightly, and the current FDV has reached 13.21 billion US dollars, with a maximum of 14.85 billion US dollars.

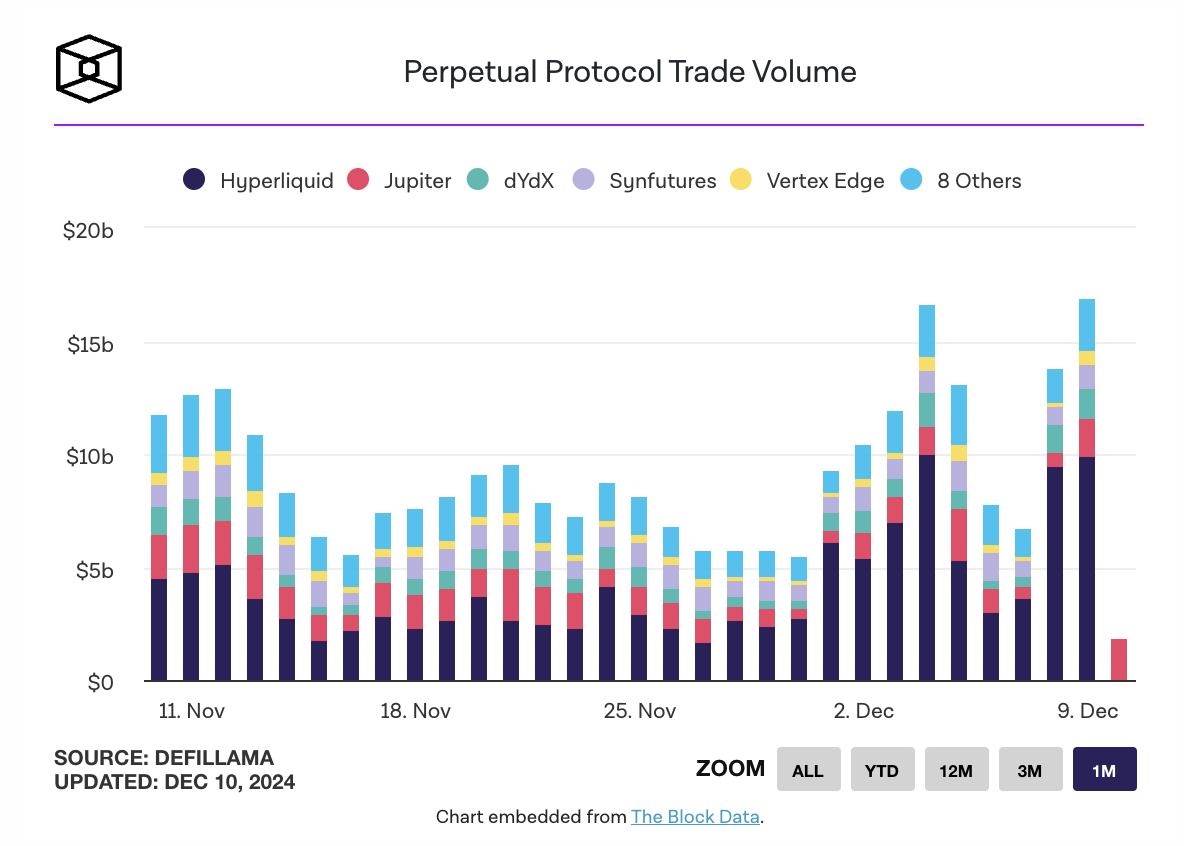

At the same time, Hyperliquid has a strong competitive advantage in the derivatives DEX track. According to data from The Block on December 9, Hyperliquid's trading volume on that day reached US$9.89 billion, accounting for 58.4% of the entire track (about US$16.92 billion).

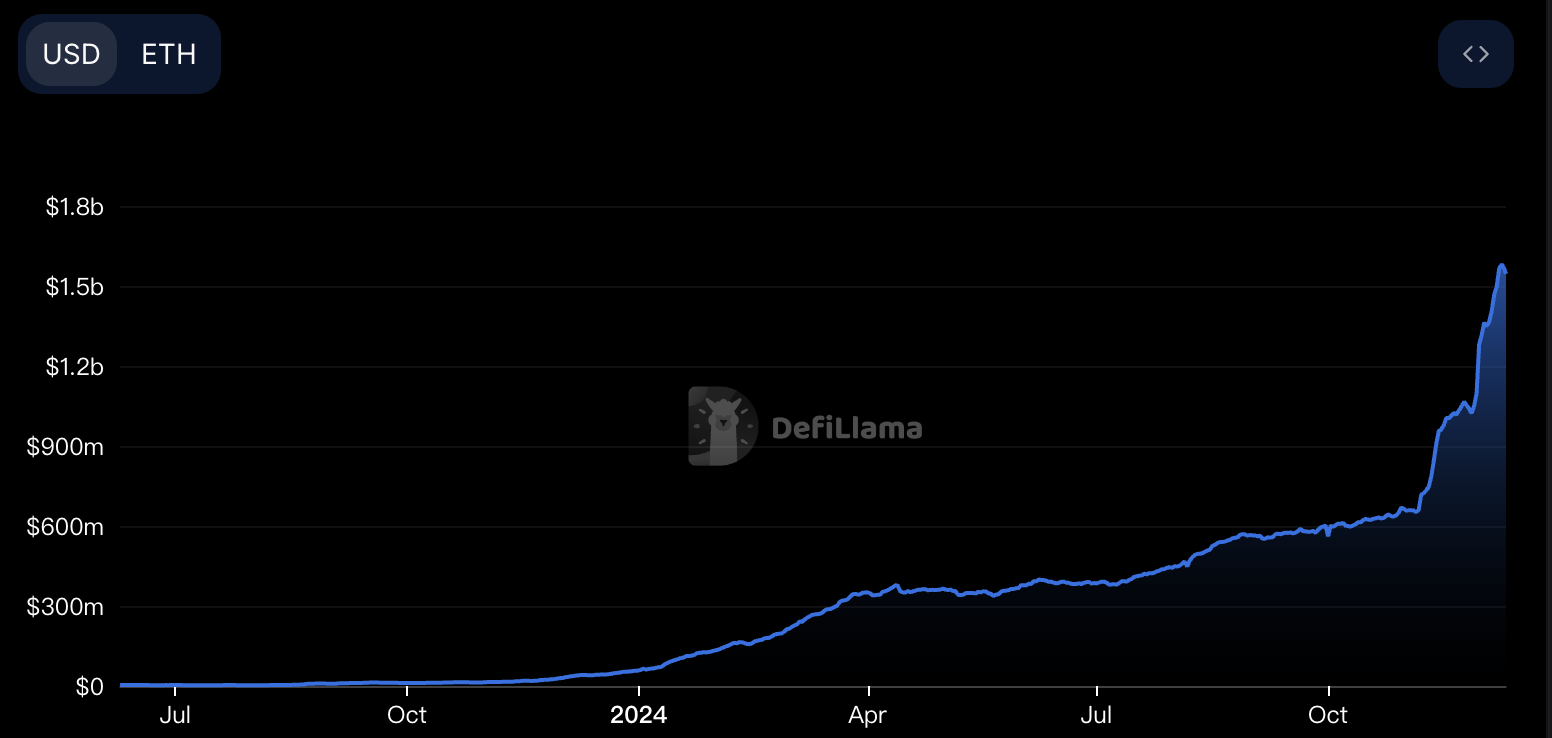

At present, Hyperliquid has accumulated a lot of assets. According to DeFiLlama data, as of December 10, the TVL of Hyperliquid Bridge reached 1.54 billion US dollars. With the huge asset pool of the platform, if Hyperliquid launches more high-quality projects, it may further release trading potential.

In addition, from the perspective of money-making ability, Hyperliquid has demonstrated strong profitability. According to research and analysis by @stevenyuntcap of Yunt Capital, the revenue of the Hyperliquid platform includes instant listing auction fees, HLP market makers' profits and losses, and platform fees. The first two are public information, but the team recently explained the last source of income. Based on this, it can be estimated that Hyperliquid's year-to-date revenue is US$44 million. When HYPE was launched, the team used the Assistance Fund wallet to buy HYPE on the market; assuming that the team does not have multiple USDC AF wallets, the year-to-date profit and loss of USDC AF is US$52 million. Therefore, adding HLP's US$44 million and USDC AF's US$52 million, Hyperliquid's year-to-date revenue is approximately US$96 million, surpassing Lido and becoming the 9th most profitable crypto project in 2024.

The above data also demonstrates Hyperliquid's attractiveness and competitiveness in the market.

On the other hand, Hyperliquid is more transparent and fair in its listing mechanism. As we all know, the controversy over listing fees has a long history, including the recent controversy between Binance and Coinbase over listing fees. The opinions of all parties on listing fees are quite different.

The opposing view is that the rising listing fees have undoubtedly brought a heavy economic burden to the early development of the project, and often have to sacrifice the long-term development potential of the project, which in turn affects the healthy development of the overall ecosystem. Arthur Hayes once disclosed in his article that among the top CEXs, such as Binance, the highest fee is 8% of the total token supply of the project as a listing fee, while most other CEXs charge between 250,000 and 500,000 US dollars, usually paid in stablecoins. He believes that there is nothing wrong with CEX charging listing fees. These platforms have invested a lot of money to accumulate a user base, which needs to be recovered. However, as an advisor and token holder, if the project gives the token to the CEX instead of the user, this will damage the future potential of the project and negatively affect the trading price of the token.

However, the positive side believes that the listing fee is part of the exchange's operation and can be used as an effective tool to screen the quality of projects. By charging a certain fee, the exchange can not only ensure the sustainable operation of the platform, but also ensure that the listed projects have a certain economic strength and market recognition, thereby reducing the influx of low-quality projects and maintaining market order and healthy development.

In this regard, IOSG partner Jocy once published an article and made several suggestions. First, the exchange needs to strengthen information transparency and take severe punishment measures against problematic projects; second, the exchange should isolate departmental interests to avoid conflicts of interest; finally, prudent due diligence must be conducted to ensure a diversified decision-making process and say "no" to any form of project fraud.

In addition to exchanges, project parties should not rely on CEX listings, but rather on user participation and market recognition. For example, Binance founder CZ said not long ago, "We should work to reduce such 'quote attacks' in the industry. Bitcoin has never paid any listing fees. Focus on projects, not exchanges." Arthur Hayes said that the biggest problem in the current token issuance is that the initial price is too high. Therefore, no matter which CEX obtains the first listing rights, it is almost impossible to achieve a successful issuance. At the same time, for those project parties who blindly pursue listing on CEX, selling tokens to the listing trading platform can only be done once, but the positive flywheel effect formed by increasing user participation will continue to bring returns. Crypto researcher 0xLoki also wrote that the iron must be hard to forge, and any exchange will list a good enough project. If you need to accept extremely harsh terms to go on the exchange, you need to first think about the motivation of the project party: Is the project really good enough? What is the real purpose of listing on the exchange? Who will pay for the cost in the end?

Ultimately, the core issue of the controversy over listing fees lies in the transparency and fairness of the fees, as well as the sustainable development potential of the project. Compared with the opacity and high fees faced in the CEX listing process, Hyperliquid's listing auction mechanism can reduce listing costs and enhance market fairness, thereby ensuring that the assets on the platform have higher value and market potential. At the same time, Hyperliquid returns listing fees to the community, a mechanism that also helps to encourage more users to participate in transactions.

In general, in the current market environment, how to balance the listing costs and the long-term development of the project has become a core issue that the industry urgently needs to think about and solve.